How AI's butterfly effect is rippling through every corner of the ASX

Martin Conlon | Schroders

AI scepticism has not been lucrative to date. For the most part, scepticism of any kind hasn’t been lucrative.

Claims of interplanetary data centres (no doubt with some future interplanetary revenues) and an addressable market for artificial intelligence of $26.5 trillion (about 20% of global GDP) raise few eyebrows. A seemingly laughable IPO valuation of US$1.75 trillion for SpaceX (about 100x revenue) is an obvious opportunity for a quick profit.

For those of us attempting to invest at sensible prices that stack the longer-term investment odds in our favour, and focused on earnings growth and profit pools that remain tied to earthly reality, these are slightly uncomfortable conditions. Seemingly certain ways to lose money longer term are proving profitable in the short term.

The ballooning global balance sheet, pumped up by ever-growing private and public sector borrowing, continues to heighten price volatility, often in response to small supply/demand imbalances.

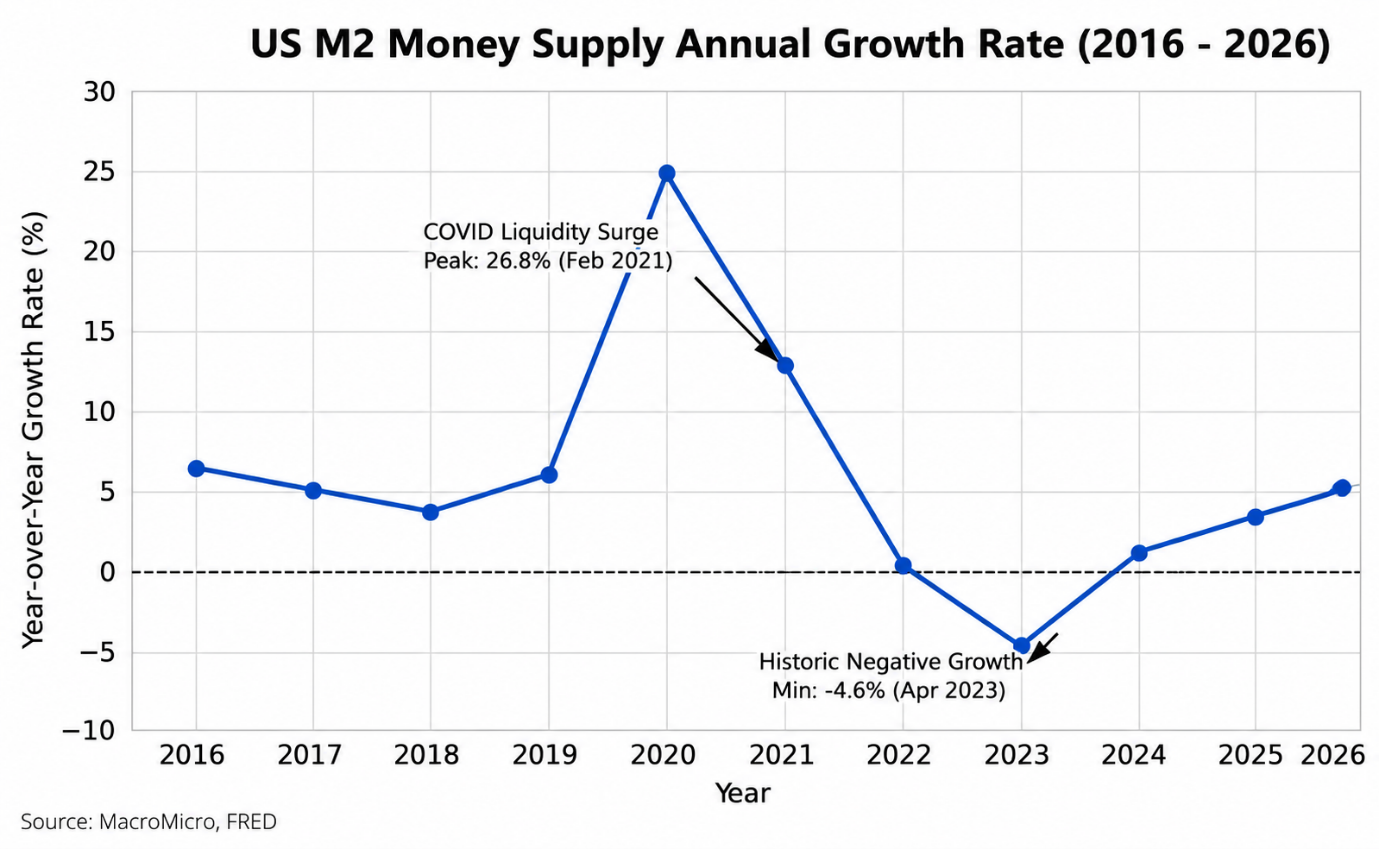

US money supply growth is strong and accelerating, adding fuel to already buoyant markets and asset prices. A more leveraged balance sheet necessarily means more sensitive valuations. Add declining genuine liquidity as institutions shy away from lit markets dominated by high-frequency traders seeking to extract profit from retail order flow and rules-based processes ranging from passive funds to leveraged semiconductor ETFs, and it is tough to argue we’re making progress towards more efficient and fair asset pricing.

SpaceX is perhaps a case in point. The vast pools of money directed towards rules-based investment processes, as asset owners focus more on explicit fee costs than costs to future gross returns, create plenty of incentive to arbitrage these processes and the organisations that set the rules.

Creating highly imbalanced supply/demand situations (where a free float of less than US$100bn sets the price for more than US$2 trillion in paper market value) has been bread and butter for investment bankers for years.

Nevertheless, the scale has never been this large, and the proportionately large fees extracted by venture capital firms and investment banks based on these paper market values are not paid in the same paper.

The unhealthy power in the hands of index constructors, the ability for these rules to be perverted and gamed, together with the already high cost being extracted for simple mathematical calculations, is increasingly distorting markets.

As Mr Buffett has noted, “what the wise man does in the beginning, the fool does in the end”.

Grappling with and dimensioning the implications of AI, not to mention determining which areas are bubbles and which may be real, remains one of our more significant challenges at present.

While direct exposures may be centred in the US, the butterfly effect is evident everywhere. Apparently small distortions are having very large impacts, both on the economy and asset prices. Data centres, power, water, commodity prices, unemployment fears, capital expenditure booms, cyber security threats; little is left untouched.

The massive capital expenditures that are growing the balance sheets of tech giants without depressing earnings are simultaneously appearing as revenues and earnings in the beneficiaries, creating the illusion of an earnings boom.

It is also altering the cashflow dynamics of US markets as the walls of cashflow that used to be directed to buybacks morph into capital raisings and debt issuance.

Perhaps most importantly, these massive cashflows are hitting the real economy, creating large imbalances in areas where the real economy cannot keep pace with the grand ambitions of tech oligarchs accustomed to ‘scalability’ and growth rates that do not exist in the physical world.

Whether this capex boom delivers economic value, productivity gains, both or neither seems likely to be important, as will the distortions it creates along the way.

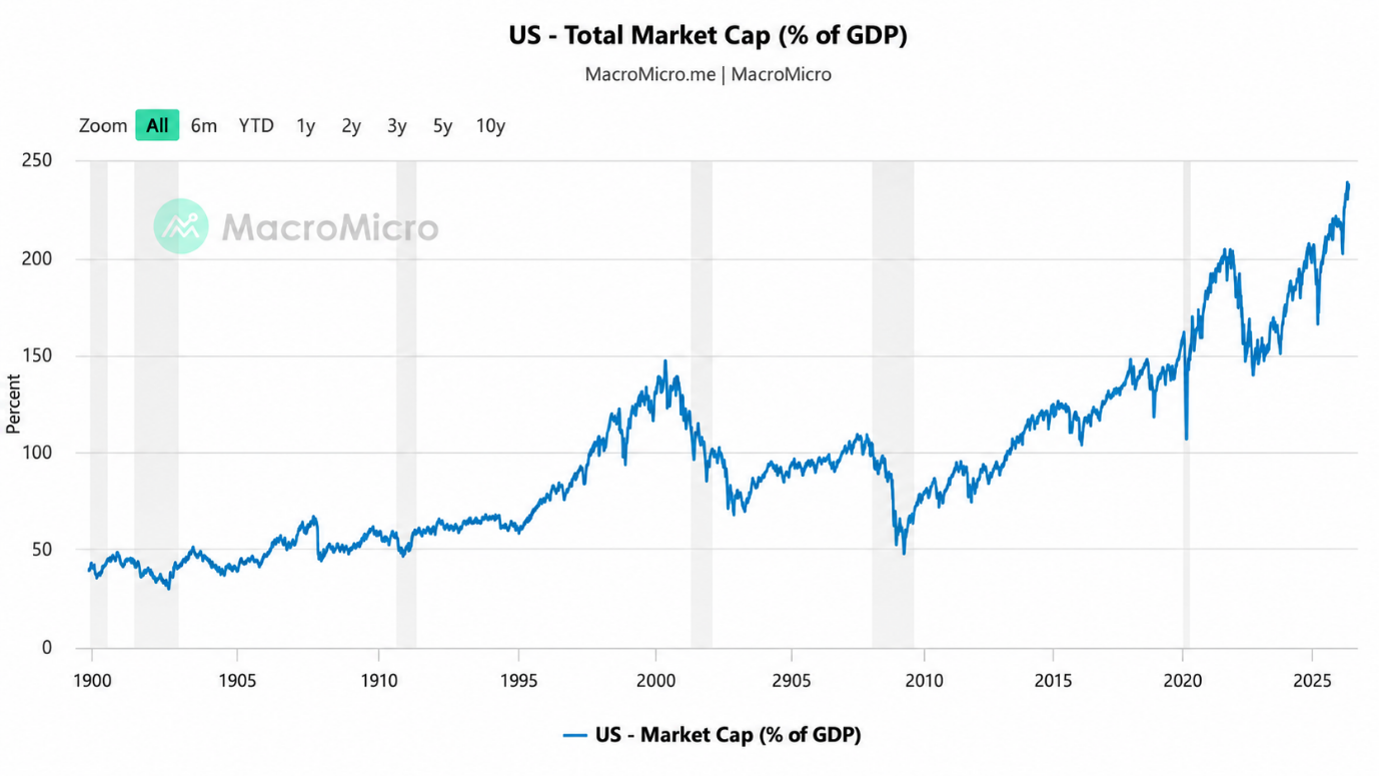

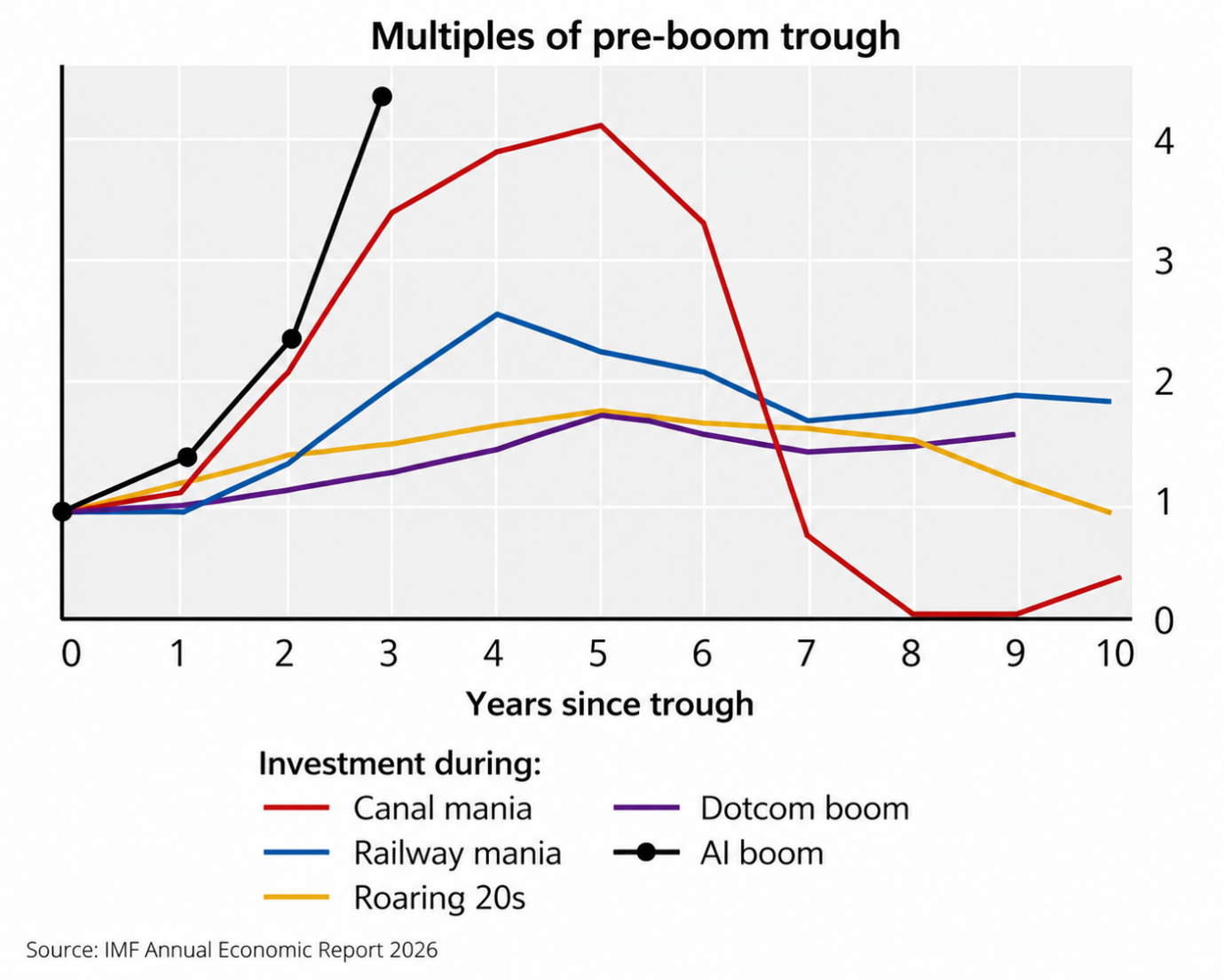

The enormous scale that spending has reached relative to both GDP and previous booms leaves us sceptical these levels can be anywhere near sustainable in the longer run and highly concerned that revenue potential can meet expectations. Valuations are not pricing this questionable sustainability.

Joe Walker, in one of his always excellent podcasts, was covering some of this territory in his discussion with Productivity Commissioner Danielle Wood. A couple of the more interesting points they discussed in determining the prospects for economic value accretion were around the absence of network economics relative to history for the technology behemoths and the likelihood of economic rents being extracted in ancillary areas such as data centres or the application layer.

While historic network economics are providing the cashflows to fund massive data centre, processor and memory investments, LLMs have not yet been able to ‘lock in’ customers, competitive advantage has been fleeting as performance differentials are quickly closed, and price competition looks likely to remain a feature as Chinese companies are both viable and much lower-cost competitors (sound familiar).

The potentially narrow markets for the most expensive frontier models and the ability to use much cheaper (but still highly effective) models for the vast bulk of tasks raise the potential for the industry to have vastly different economics to today’s tech leaders.

Observing the financial statements of Nvidia or Micron, obvious beneficiaries of the capex boom, margins everywhere are egregious. Akin to the resource boom, tech providers are locking in exorbitantly elevated capital costs in developing relatively commoditised infrastructure.

The geographically diversified nature of this infrastructure also complicates the large-scale M&A that has historically been important in stymying competition.

Importantly, and positively, if it transpires that LLMs and data centres are relatively commoditised, any productivity benefits that AI delivers are likely to be more disseminated and far less US-centric.

While the economics of primary investment in AI will be vital in determining the prospects for US equity market earnings and the very large market values attached to them, it is the tentacles of AI that will be most important domestically.

While the likes of Firmus and Megaport are positioned to benefit from speculative fervour from investors more focused on the vibe than the numbers, these are not overly large companies, meaning the more material impact on Australian investors is via secondary areas such as commodity prices.

Standing back and observing the increments to market capitalisation since AI became a market feature, resource companies have been big winners. BHP, Rio Tinto and Sandfire Resources are all up more than 50% in the past year; the resource majors are also among the country’s biggest companies, meaning the dollar-value impact on investor portfolios and index performance is large.

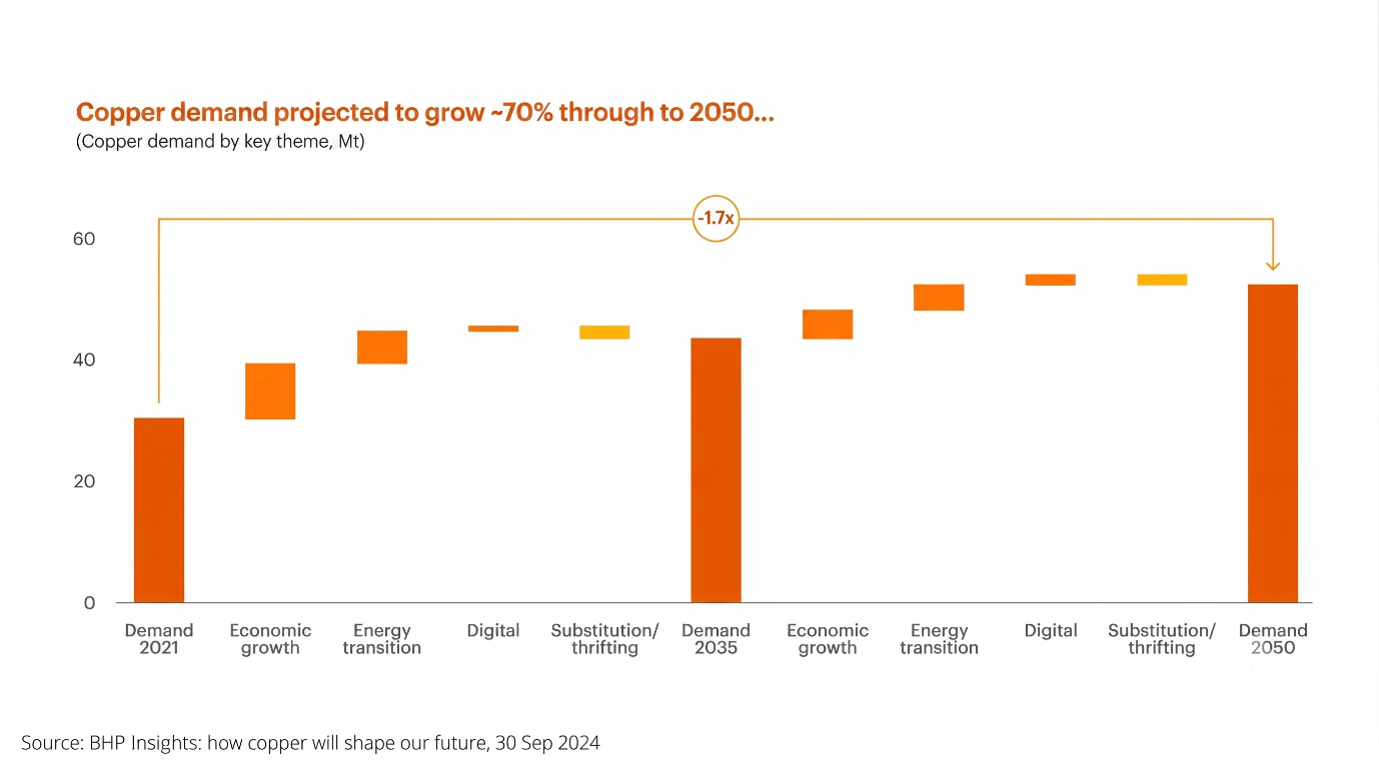

While also influenced by the themes of inflation protection and excessive government borrowing, heightening the influence of financial markets and traders in setting commodity prices as flows wash into relatively small and illiquid markets, copper prices have been the epicentre of investor attention.

Searching for second- and third-derivative exposures to AI supply/demand imbalances and expectations of an ongoing electrification boom, copper has been the commodity of choice.

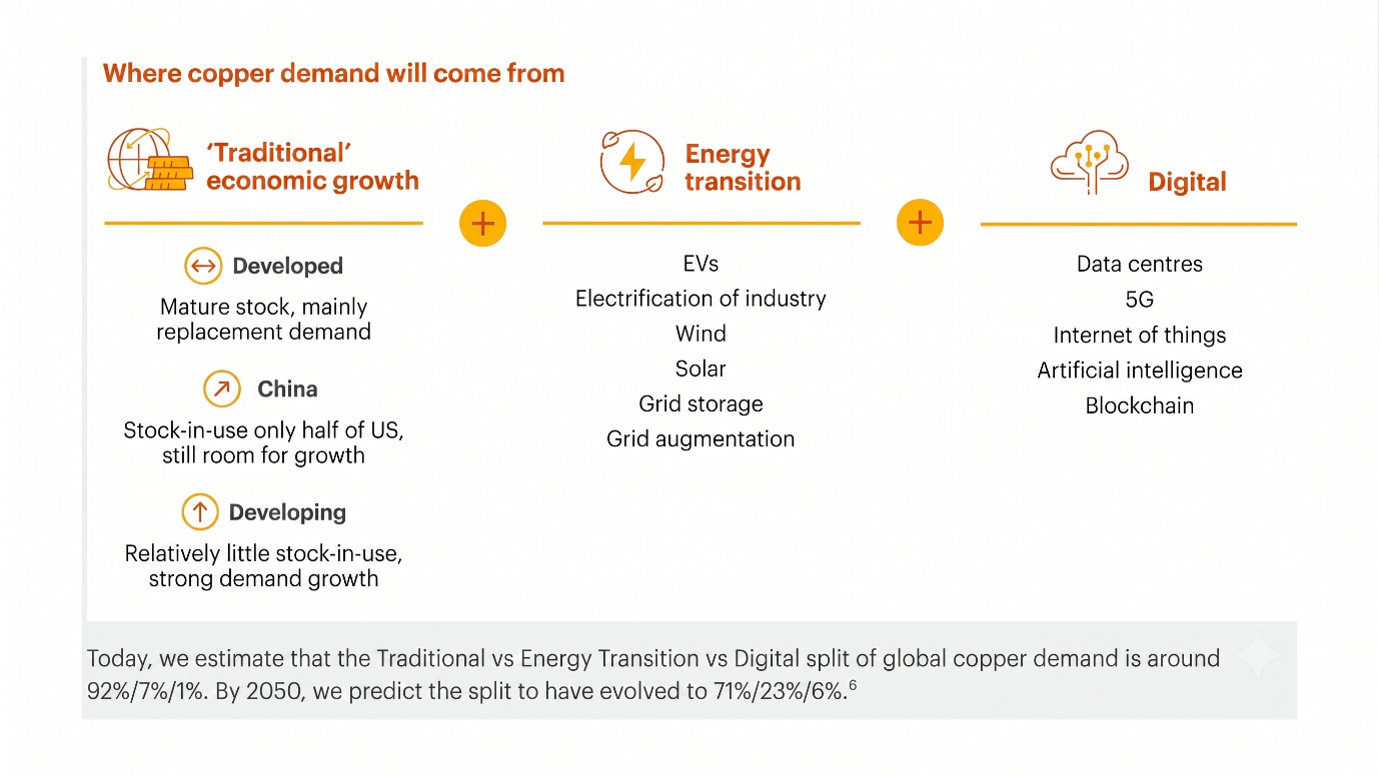

Tight mine supply has combined with strong demand forecasts to deliver optimistic commodity price forecasts despite relatively immaterial contributions to current demand.

Data centres are 1–2% of current copper demand and energy transition is around 7% on BHP estimates. Their data centre forecasts see six-fold growth in copper demand and around 9% of total global electricity consumption by 2050.

While plausible, these demand forecasts often ignore the displacement of demand from lower-value sources and the demand destruction that accompanies higher prices.

Though the positive conditions for long-term copper demand are undeniable, translating these into a sustainable copper price is more tenuous. The current US$13k/tonne copper price more than underwrites strong returns on nearly every new copper project and exceptional returns on existing ones.

Given earnings multiples for BHP and Rio Tinto are now in the high teens based on these copper prices and still very strong iron ore prices, our logic says future investment returns will be moderate if these prices prove sustainable and significantly worse should copper prices prove to be artificially elevated; a not immaterial probability.

Given $300bn of market capitalisation for BHP and another $270bn in CBA at significantly more elevated multiples, the 20%+ benchmark weight which passive investors hold seems likely to tie one arm behind your back in the fight for future returns.

Also on the commodity front, recent months have provided us with some interesting lessons on the value of inventory and stockpiles.

Our expectations that destruction of production infrastructure, interrupted supply chains and drawing down of inventories/strategic reserves in oil and gas would prove supportive for oil prices have proven misplaced, at least in the short term. What did we miss?

Firstly, strategic petroleum reserves proved incredibly effective in ensuring economic resilience and facilitating price control. The ‘just-in-time’ inventory systems that companies love might be wonderful for capital efficiency, but they are rotten for resilience and sustainability. We feel this may have some important implications for the value of logistics assets in a less co-operative geopolitical landscape.

Secondly, operating in a market in which the cost to consumers is material and visible is tough. Governments wanting to get re-elected are working hard against you, and are happy to use plenty of taxpayer money in the fight. Our thinking in weighing the outlook for theoretical free market prices versus real-world outcomes in areas such as electricity prices suggests we should skew towards a more conservative outcome.

The perhaps savage reaction to the announcement of a few material bad debts by Judo can be viewed from a few different angles.

At a company level, as the doors close on the decades of aggressive mortgage lending that have pumped property prices into the stratosphere, major banks are rushing into the business lending sphere for growth.

For a small bank with a funding cost and scale disadvantage, this isn’t great news. Finding new loans is already a competitive business. When major banks can profitably undercut your pricing, particularly on better-quality loans, life becomes tougher again, and the pressures of trying to deliver the growth needed to achieve scale with a loan book deteriorating in quality is a management challenge, to say the least.

At the broader bad debt level, determining whether the Judo experience is the canary in the coal mine for deteriorating loan quality is much tougher again. We have long debated the best way to price bad debt risk. It is akin to the turkey-before-Christmas risk; most days and years are just great, then things end very badly! Most risk and capital adequacy models have done a very bad job of dimensioning this risk. It is not an even probability through time.

Perversely, after a system is cleansed through hard times (Ireland, Spain, Greece), it lays the platform for stronger growth, asset price recovery and benign bad debt conditions.

At the time of greatest pessimism, future risks are well below average. Long periods of benign conditions sow the risks for the future. Lending standards erode and asset price/speculative lending takes the place of lending solidly covered by cashflows, and risk moves to well above average.

In Minsky’s cycle (hedge finance, speculative finance and Ponzi finance), Ponzi finance is the phase in which borrowers realise that cashflows can’t even cover interest costs. Negative gearing, by definition, is a taxpayer-funded subsidy for those where borrowing costs aren’t covered by cashflows. These ludicrous incentives have actively encouraged speculation and poor lending, reinforcing our perception that Australian banks house above-average forward-looking risks, despite risk models claiming everything is hunky-dory.

In a traditional bank bad debt cycle, bad debts first erode earnings, then regulatory capital. Capital erosion forces equity raising and shareholders are forced to determine whether the erosion is near its conclusion and worthy of injecting more capital, or whether they are injecting capital as a donation to debt holders.

As for many free markets, things have morphed. Whether through direct government intervention, aggressive interest rate reduction or monetisation, the size and risk inherent in asset price destabilisation mean a raft of intervention in any bad debt cycle. This socialises and redistributes losses that should rightfully be worn by bank shareholders and debt holders.

China and Japan have adopted variants of this model. The cost of this model is much lower growth as none of the bad debts are cleansed. This makes pricing banks more difficult again.

Socialising losses prevents the earnings and capital erosion but costs vast economic growth potential as the rest of the economy is forced to pay the bill. It is probably a much better outcome for bank shareholders as the turkey risk is removed.

Above the bank bad debt level and its reliance on asset pricing, the impact of asset price stabilisation or decline on the broader economy becomes more complex again. Even with the assumption of socialised bad debt experience, asset price growth eventually hits a wall, as it did in China and Japan.

Whether this stabilisation and/or decline is upon us is difficult to determine. Despite ‘property price crash’ headlines, nothing more than an extremely benign flattening has occurred to date.

The ‘butterfly effect’ of decades of speculative activity and the extent to which rising asset prices permeate a raft of listed businesses are impossible to model; however, our suspicion is they run deep. 22,000 mortgage brokers (a mortgage broker for every 1,000 adults), a population besotted by home improvement, insurance pricing propelled by rising values, property development of all kinds where viability depends on rising prices; the linkages are endless.

We are actively seeking portfolio exposure to businesses able to deliver profits without asset price rises as fuel. As capital has chased AI exposure and derivatives of it, numerous good-quality businesses have been left behind.

The broad geographic exposure and economic diversity offered in apparently homogeneous sectors leave us very comfortable holding a range of positions in sectors such as healthcare. Ramsay Healthcare, Cochlear, CSL, ResMed and Sonic Healthcare have almost nothing in common other than the GICS sector code.

While the days of systematic investment dominance mean they may often share trading patterns, we believe their lack of economic correlation is vastly more important than their market correlation. We expect this economic diversity may prove highly sought should the butterfly effect from AI change direction.

In other sectors that have seen significant reversion, such as technology, we struggle to see opportunity, as valuation rests on the belief in high levels of earnings growth followed by long-term sustainability, given multiples remain well above market averages.

Market outlook

Vibrant money supply growth, particularly in the US, leaves equity market conditions buoyant, leverage building and most cautious investors unwilling to stand against effervescent valuations. Flows are dominating fundamentals. The absence of financial discipline at a government level in most major economies and the mounting pressures on central bankers to accommodate rather than control this lack of discipline has been a feature for some time.

To the credit of Michelle Bullock, the importance of controlling inflation and standing against political pressure remains well understood domestically.

Nevertheless, in a world in which capital flows readily across borders, the US remains the main game and discipline more questionable.

Very fully priced banks and commodity stocks which are, in the main, no longer cheap leave the domestic equity market in a relatively challenging position. Though selective attractively priced opportunities remain, undervaluation remains the exception rather than the norm.

In complex systems such as equity markets, the chaos theory from which the butterfly effect emanates suggests investors should always be prepared for conditions to change abruptly, often induced by seemingly innocuous factors. We remain focused on business fundamentals and protecting capital rather than relying on cheap money propping up speculative excess.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 15 July 2026. This document was originally published in Livewire Markets on 15 July 2026. This information has been prepared by Schroder Investment Management Australia Limited (ABN 22 000 443 274, AFSL 226473).. The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.