28 June Markets at a glance

Leah Gibbons | nabtrade

Around the grounds

- ASX higher; on track for an over 2% HY gain

- Gold on track to shed 1.4% in H1

- Miners set to log worst HY performance since late 2015

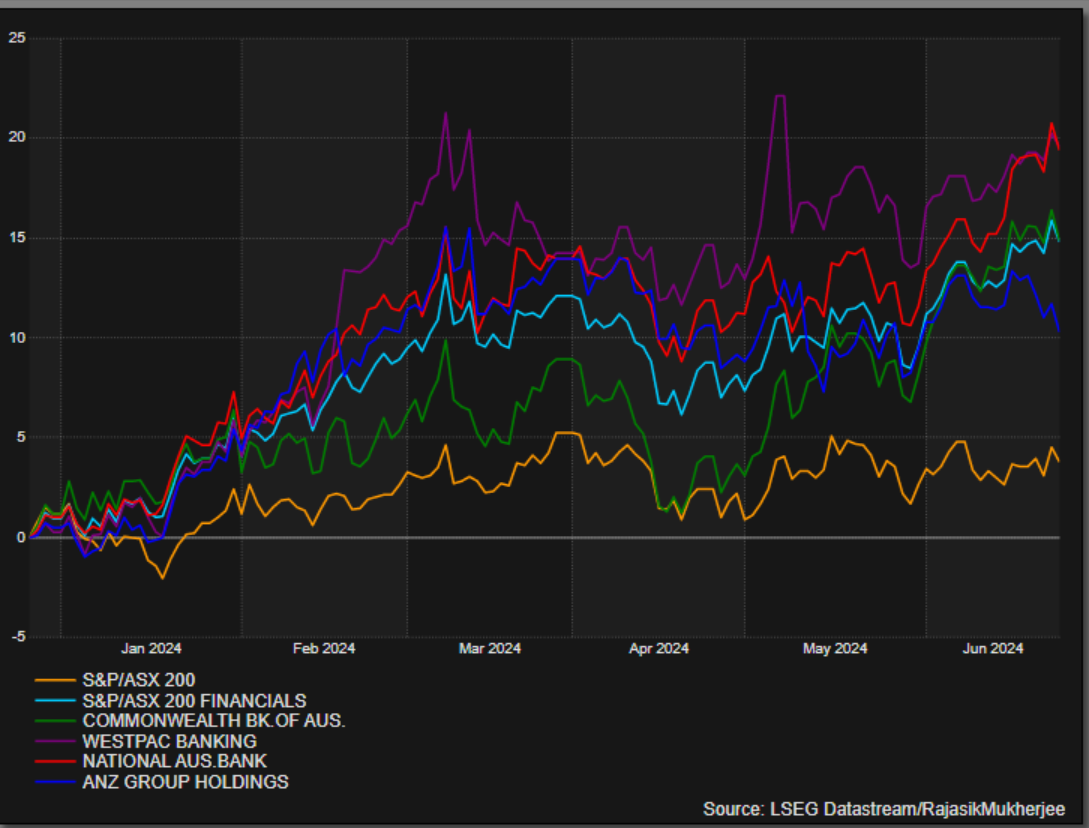

- Banks to log best HY since mid-2021

- Energy stocks set for worst half since CY20

- Investor caution ahead of PCE tonight

The S&P/ASX200 is trading higher on the last trading day of the tax year and the end of the first half, setting up the benchmark for modest gains in the period as sluggish economic growth and high inflation weigh on performance.

The index is on track to gain 2.2% for the first six months of 2024, in line with gains a year earlier but lower than a near 5.5% jump in the second half of 2023.

Breaking down the first half of the year

Gold stocks are on track to fall 1.4% in the first half, amid broader economic worries which has taken the steam out of bullion prices.

It’s a sharp turnaround from the over 11% spike seen in H1 and H2 of 2023 as slow growth, high inflation and a possible interest rate hike on the horizon from the Reserve Bank of Australia (RBA) are the key drivers in the reversal.

Australian listed miners have also taken a dive, set to lose over 13% in the period, logging the worst half-year performance since the second half of 2015 as the price of iron ore fluctuates, down some 16% so far this year on the tails of weaker demand.

Giants BHP Group (BHP) and Rio Tinto (RIO) are expected to shed 14.4% and 10.4% respectively in the first half.

Healthcare is expected to end the half up over 4%, energy stocks are set for their worst half since CY20 on oil price weakness, while sticky inflation has capped gains for the Australian staple consumer firms.

On the flip-side financials have surged 13% in H1 2024, compared to a 2.2% fall a year earlier. The aussie sub-index is on track to log its best HY since June 30 2021, thanks to high interest rates and the door for a hike left wide open after May’s CPI print rose to a six-month high.

In the news

Sticking with the banks, the Federal Government has given the go-ahead of ANZ Group’s (ANZ) AU$4.9 billion buyout of Suncorp’s (SUN) banking business, after nearly two years of scrutiny by regulators and treasury. Suncorp shares have soared to a 17-year high after the approval.

Australian listed shares of Lake Resources (LKE) have tanked after the lithium developer swung the axe on jobs and is eying up an asset sale as low prices of the electric vehicle battery metal scupper efforts to find customers.

It’s the latest blow to the industry after the more than 80% drop in prices for the metal in the past year, fuelled in part by Chinese oversupply and concerns the EV industry isn’t growing as fast as previously expected.

And Insurance Australia Group (IAG) shares are amongst the top of the benchmark as it inks a deal with US-listed Berkshire Hathaway to buy reinsurance protection to migrate natural perils volatility for the next five years. On the outlook, the general insurer has confirmed it is poised to reach its FY24 reported profit with margins around the upper end of its outlook ranges.

Going global

Around the region Asian stocks are headed for a fifth straight month of gains, bolstered by the possibility of rate cuts in the US. Caution though remains ahead of a risk packed session tonight followed by a subdued week.

On the data docket all eyes are on May’s US Core PCE data, the Fed’s preferred measure of inflation, released tonight, which could offer further clarity on the path of policy. Fed futures are currently pricing in a 64% chance of a first rate cut by the US central bank in September, up from 50% a month ago, according to the CME FedWatch Tool.

MSCI's broadest index of Asia-Pacific shares outside Japan is marginally higher in the trading session, and on track to gain over 3% for the month.

Tokyo’s Nikkei 225 has reversed some of yesterday’s losses to eye a monthly gain of 3%, helped by a weak yen and a rally in tech stocks, while US futures have come online a tick higher.

In currencies, the yen continues to trudge at 38-year lows against the greenback, with markets remaining on alert for any intervention from Japanese authorities to prop up the currency. The euro meantime is higher, though headed for a 1.3% monthly loss as political turmoil in the block continues to weigh on sentiment, with France’s snap election due to kick off this weekend.

All prices and analysis at 28 June 2024. The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.