Why should investors stay invested during market volatility?

When an airplane experiences turbulence it can be unnerving if you’re not used to it. Still, the pilot and crew -- after telling you to stay seated and fasten your seat belt as a safety measure – typically stay on course so you can reach your destination.

That’s a lesson for investors. One of the bitter truths of investing is that stocks and bonds don’t always go up. As we have seen in 2022, in fact, sometimes that selloff can be quite dramatic – and painful.

When facing bouts of market volatility, it is important to not focus on the day-to-day swings, but your longer-term investing goals. Of course, no one likes to see their hard-earned savings diminish, so investors often ask “How should I handle market volatility?" And “Should I sell stocks when markets are volatile?" That’s why it can be so hard to accept that often the best course during market selloffs is: Do nothing.

When times are tough, we want to limit our losses. Even when things are going well, we wish we had invested more. We all fear missing out.

But when you’re investing, giving in to fear is often a losing strategy. More often than not, investors with this mindset tend to buy high and sell low as they invest more in a rising market and pull money out in a falling market.

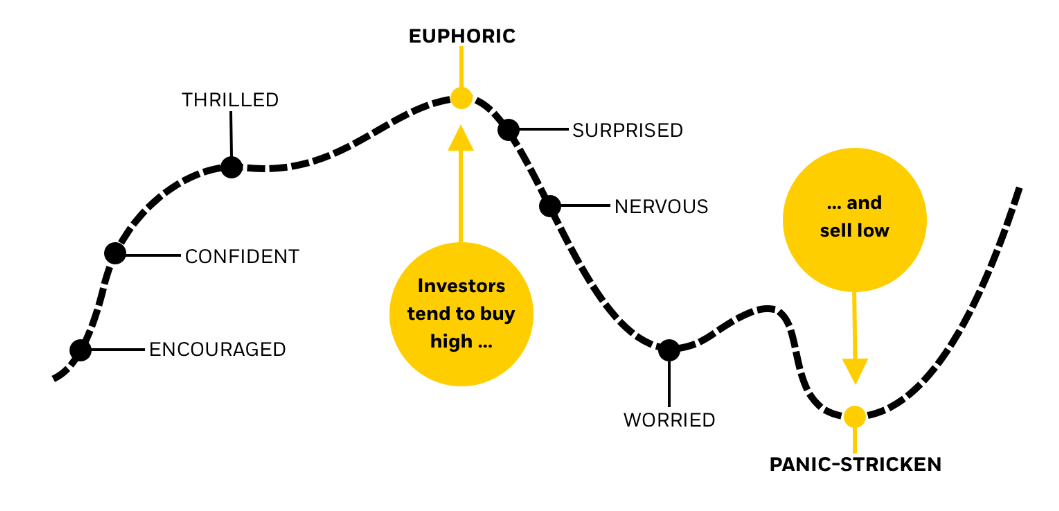

Stay the course: controlling emotions during the ups and downs of the market

For illustrative purposes only.

Source: iShares

This chart illustrates that riding the ups and downs of the market can be an emotional rollercoaster. Investors may be thrilled and confident when markets are soaring, leading them mistakenly to buy high. On the other hand, they can become nervous and panicked when markets fall, causing them to sell low. The key takeaway: focus on your long-term goals.

Having said that, sometimes it may make sense to adjust a portfolio if conditions seem to suggest that you are not going to make it to your goal if markets have changed. For example, you may need extra resilience against inflation in today’s high inflationary environment. Or you may need added diversification by increasing exposures to other asset classes, like international stocks. Changes to a portfolio like these may actually help strengthen it for the long term.

In short, making tweaks around the edges of a portfolio may make sense. But trying to time the market to avoid selloffs is extremely difficult because of the risk of missing the rebound. Instead, focus on your longer-term investing goals.

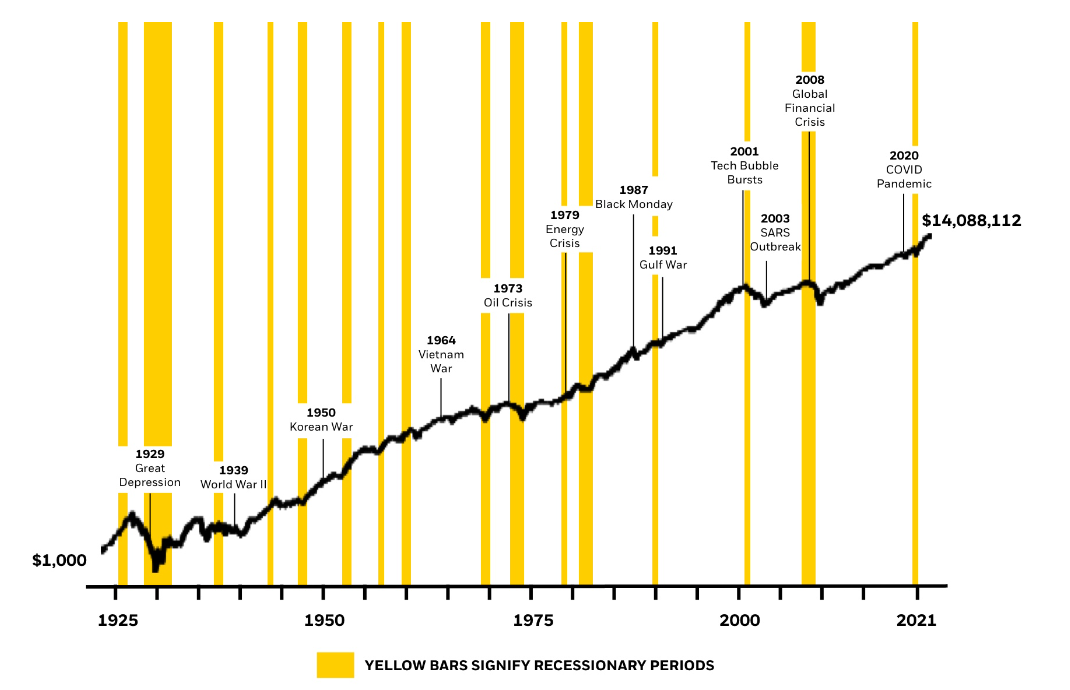

Growth of $1k in the S&P 500 since 1926 (1/1/26-12/31/21)

Source: Morningstar, National Bureau of Economic Research, and BlackRock, as of 12/31/21. Past performance does not guarantee or indicate future results. It is not possible to invest in an index. U.S. stocks are represented by the S&P 500 Index from 3/4/57 to 12/31/21 and the IA SBBI U.S. Lrg Stock TR USD Index from 1/1/26 to 3/4/57, unmanaged indexes that are generally considered representative of the U.S. stock market during each given time period. Index performance is for illustrative purposes only. It is not possible to invest directly in an index. Assumes reinvestment of dividends and capital gains and that an investor stayed fully invested over the full period.

This chart illustrates the long-term performance of the S&P 500 Index going back to the 1920s. Even though the market, as measured by that index, has endured painful selloffs and down periods, such as the Great Depression or the 2008 Global Financial Crisis, over the long term the index has climbed. An investment of $1000 in 1926 would have grown to $14,088,112 by the end of 2021.

Read more iShares insights here.

This information has been provided by iShares, a publication of Blackrock Investment Management (Australia) Limited (ABN 13 006 165 975, AFSL 230 523), for WealthHub Securities Ltd ABN 83 089 718 249 AFSL No. 230704 (WealthHub Securities, we), a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 (NAB). Whilst all reasonable care has been taken by WealthHub Securities in reviewing this material, this content does not represent the view or opinions of WealthHub Securities. Any statements as to past performance do not represent future performance. Any advice contained in the Information has been prepared by WealthHub Securities without taking into account your objectives, financial situation or needs. Before acting on any such advice, we recommend that you consider whether it is appropriate for your circumstances.