ASX dividend champions

Mark LaMonica | Morningstar

Conventional wisdom is a byproduct of groupthink that presents solutions good enough for the average person while simultaneously not being right for any individual. You follow it at your peril. Each Monday I will challenge the investing norms that just may be holding you back from living the life you want.

Unconventional wisdom: ASX dividend champions

“If you don’t know where you’re going, you could end up anywhere. If you don’t adjust your sails to the changing wind, you’re going to end up where the wind blows you, not where you want to go. To get anywhere, you have to know where you’re going, what your course is, and you have to stick to the course.”

- Larry Jacobson

One of the biggest challenges we face as investors is trying to adapt generic investing advice to our own circumstances. A reader was recently struggling with this very issue in his pursuit of an income strategy. A topic close to my heart.

The reader was grappling with taking the standard income investing advice in the US and applying it to the Australian market. The US has the deepest capital markets in the world and a lot of investing guidance is US centric.

It is easy for Australians to assume US investors aren’t interested in income investing. Afterall, the yield on the S&P 500 sits just north of 1% and most of the media attention on the US market is about high flying – and low yielding – tech shares.

That isn’t the case. US investors are drawn to income investing for the same reason that makes it an attractive strategy for Australians. That doesn’t mean the markets are the same.

Differences between the US and Australian market

In Australia company management will typically establish a target earning payout rate to support a dividend. For example, CBA has a target of paying out between 70% and 80% of net profits after tax in dividends.

A range gives management some discretion, but investors are comfortable with dividends fluctuating along with the often-cyclical nature of earnings. A dividend that is lower than the previous year is generally shrugged off. What matters is a high earnings payout rate to reflect the advantageous tax environment of franking credits.

Income investors in the US have a different mindset. A dividend cut is seen as a significant red flag and a signal that the company is in trouble. Knowing this mindset means many companies will only cut a dividend as a last resort. This reinforces the investor aversion to dividend cuts.

The earnings payout rate is much lower in the US. This cushion allows companies to handle the cyclicality of earnings without needing to cut the dividend.

If US income investors avoid companies that cut dividends, they conversely seek out those that consistently raise them. That mindset spawned the dividend aristocrats and dividend kings.

There are currently 69 dividend aristocrats who have raised their dividend for 25 consecutive years and 54 dividend kings with 50 consecutive years of dividend increases. Many companies see inclusion on these lists as a point of pride. This further reinforces the stigma of a dividend cut.

Applying US income investing advice to Australia

With this background it is clear why income investing guidance from the US doesn’t work in Australia. Avoiding companies that ever cut their dividend and seeking out those that consistently raise them leaves income investors with few options. The only company in Australia that meets the dividend aristocrat criteria is Soul Patts.

Getting too bogged down in ‘rules’ can obscure the bigger picture. At a bare minimum a successful income investor needs to grow a passive income stream at a higher rate than inflation. You can’t achieve financial freedom if your passive income grows slower than inflation.

If you are retired and can already support yourself off passive income simply matching inflation might be ok. But for most investors trying to improve their standard of living and / or eventually replace a salary the income growth rate needs to exceed inflation.

While consistent growth is preferrable there are ways to deal with fluctuating income. Retirees can rely on a cash cushion to smooth out year-to-year variations while accumulators can patiently focus on the long-term.

Using this success criteria, I’ve set out to find Australian shares that meet the spirit, if not the law, of the standard income investing advice in the US.

These are the Australian dividend champions – they may not have the pure lineage of the aristocrats or kings, but they get the job done in the end.

Finding the ASX dividend champions

Step one: Beating inflation

The first step in my search for the Aussie dividend champions is to compare 2016 dividends to 2025 dividends for each of the 214 ASX listed shares in our coverage universe.

Higher dividends are great. But the goal is to grow passive income at a pace faster than inflation. Since 2016 inflation has cumulatively increased 36%. Using that as a cut-off there are 47 companies that have a 2025 dividend at least 36% higher than 2016.

Step two: Consistently rising dividends

I wanted to account for the variability of year-to-year dividends in Australia but make sure the trajectory was consistently higher. To do this I took the average annual dividend over the past 10 years and compared that to the 2025 dividend.

Again, I used a 36% cut-off for inclusion onto my list. This is a high hurdle rate, but it further reinforces that only shares that have grown dividends at rates comfortably exceeding inflation will be included. There are now 27 names on the list.

Step three: The future

The future is the only thing that matters for investors. I looked at our analyst estimates for dividends over the next two years for each of the 27 remaining dividend champion candidates.

I allowed for estimates of lower dividends but had a cut-off if the drop was more than 10% from 2025 levels. There are now 23 names on the list.

Step four: Not paying a dividend

There is a difference between dividend variability and not paying a dividend at all. In any country eliminating a dividend for a year is not a great sign.

Since I’m trying to maintain high standards for my dividend champions list I’ve removed three companies from the list that eliminated an annual dividend at some point over the last decade. After removing Santos, Qantas and Origin, 20 companies remain.

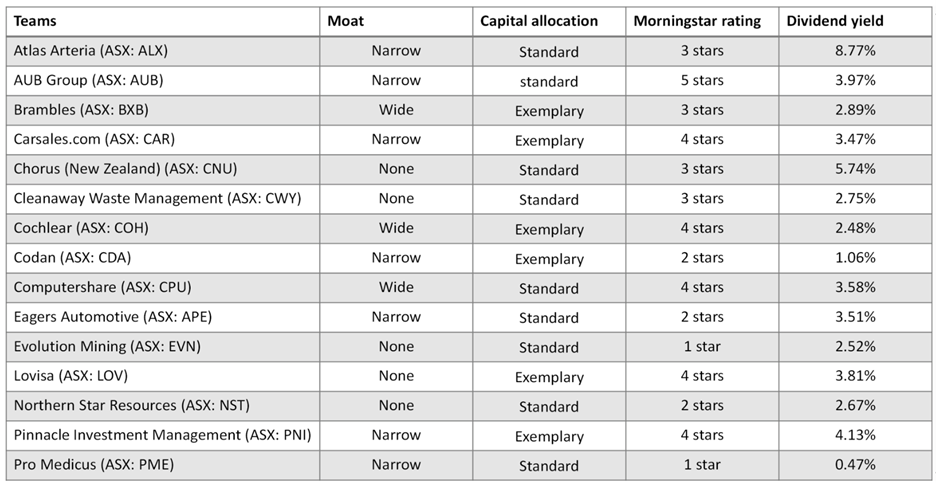

Behold the dividend champions:

Source: Morningstar

Source: Morningstar

Insights from the dividend champions

I put the ASX 200 through the same set of criteria I used to select the dividend champions. As a proxy I used the SPDR S&P/ASX 200 ETF (ASX: STW). This isn’t a perfect comparison as ETF distributions include capital gains but they are minor for market capitalisation weighted indexes.

The ASX 200 failed to meet my standards on multiple levels. The 2025 distribution is only 17% higher than the 2016 distribution which trails inflation by about 20%. The 2025 distribution is only 3% higher than the average annual distribution over the decade. That is 33% below the standard I set for the dividend champions.

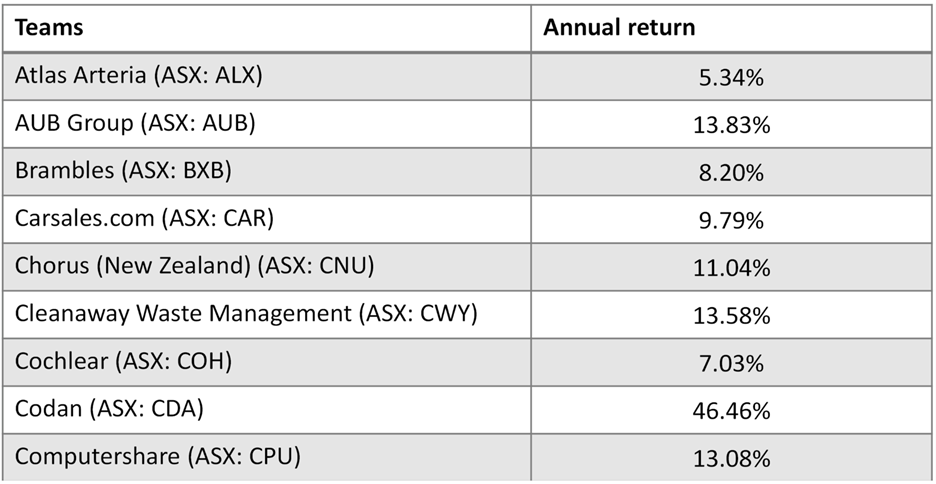

From an income growth perspective, the 20 dividend champions have significantly exceeded the overall index. They also significantly outperformed the index with an average annual return of 17.93% for the last 10 years compared to 9.81% for the ASX 200. The following chart shows the return for each member of the dividend champions.

Source: Morningstar

Source: Morningstar

How you should use the dividend champions

The dividend champions list was created by backtesting a desired outcome using historic data. It shouldn’t be a surprise that the companies that met my criteria outperformed from a dividend growth and return standpoint.

Investors should be wary of backtesting. Historic data can provide perspective but backtesting also encourages look-ahead bias where we assume investors in the past had information that wasn’t available at the time. Backtesting is often used to construct convenient narratives about the past that might not apply in the future.

That doesn’t mean the dividend champions, dividend aristocrats or dividend kings are useless. Here are some ways to use the list.

Jumping off point for more research

One use is as a jumping off point for further research. Given the number of investment options available it is always helpful to create a more manageable starting point to dig into.

If you are an income investor and using the dividend champions list for further research, I would suggest the following:

- Try and determine why each of these companies was successful in the past. Think about the macro factors that facilitated their success, things the company did well and the competitive environment they operated within.

- Determine the likelihood of the factors leading to their success persisting. Threats include changing economic conditions, an evolving regulatory environment, new technology and the responses of competitors.

Investors tend to focus too much on short-term catalysts for different shares. Assessing the long-term factors for dividend growth is far more useful for income investors. If the company is successful, the share price will take care of itself.

The type of companies that made the list – and those that didn’t

First a warning - correlation is not causation. I wouldn’t change your investment strategy because 30% of the company names on the list start with the letter C. But if there is a reasonable explanation to why certain types of companies do well it might provide a valuable insight.

Prevalence of moats

The first thing that jumps out to me is that 70% of the companies have a narrow or wide moat which denotes our analyst’s view that they have a sustainable competitive advantage. Given 35% of the overall population of shares we cover in Australia have a moat I think this insight is valuable.

To grow dividends a company needs to grow cash flows. Competition often means lowering prices or investing more in creating better goods and services. A sustainable competitive advantage limits the impacts of competition which frees up more cash to pay dividends.

Need for strong capital allocation

Paying a dividend is both a management choice and a byproduct of having funds available to return to shareholders. You can’t pay dividends if management makes poor capital allocation decisions by investing unwisely in the business, making foolhardy acquisitions or taking on too much debt.

These collective capital allocation decisions are assessed with our analyst’s capital allocation rating. 40% of the dividend champions receive our highest capital allocation rating of exemplary. This compares to 17% of the overall coverage universe.

Who didn’t make the list

None of the big 4 banks made the list. NAB and Westpac had lower dividends in 2025 than 2016 and ANZ’s dividend was marginally higher. CBA’s 2025 dividend exceeded the 36% threshold over 2016 but the average dividend in the decade didn’t meet the threshold when compared to 2025.

The growth prospects for banks is limited in a relatively stable competitive environment dominated by the largest players. It isn’t surprising they failed to grow dividends at a rate higher than inflation.

The largest miners also didn’t make the list. BHP, Fortescue and Rio grew their dividends at a high rate when comparing 2025 to 2016. But given wide fluctuations in annual dividends none of them exceeded the 36% threshold for the current dividend compared to average dividends over the decade.

This is also not surprising as miners are price takers and at the whim of commodity prices which are inherently cycle. Mining is also a capital-intensive business where replacing reserve depletion and bringing new production online is a costly endeavor.

Final thoughts

It is an interesting mix of companies that made this list. There are some companies that most income investors wouldn’t consider like Pro Medicus with a 0.47% yield or Codan with a 1.06% yield. There are also companies with high yields like Atlas Arteria with concerning prospects given the upcoming loss of a major toll concession.

More than anything this exercise illustrates that you can’t even begin to create an investment strategy or select investments without understanding what you are trying to accomplish.

Income investing is too often simplified into finding the shares with the highest yields. Pursuing an income strategy is framed as a trade-off which forsakes capital growth. These are both misnomers.

Whatever you are trying to accomplish start by breaking down what success looks like. That doesn’t guarantee you will accomplish your goal but it sure beats the alternative – mindlessly flailing about trying to reach an outcome you haven’t bothered to define.

Access this research and more at Morningstar. For a free four-week trial, click here.

All prices and analysis at 20 March 2026. This information has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892.). Morningstar’s full research reports are the source of any Morningstar Ratings. The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.