Private Credit headwinds move onshore

Phil Strano | Yarra Capital Management

It’s a significant understatement to suggest it’s been a big couple of months in markets, with the conflict in Iran continuing to dominate headlines and drive volatility. For Australian private credit investors, however, large exposures to real estate lending could mean the worst is yet to come.

Before the conflict’s commencement, the financial market’s main worry was the rise of AI tools and the potential implications for software companies, with substantial declines in their equity valuations being a painful experience for many investors. In being large lenders to the software space, US private credit funds have also been caught up in the turbulence, with fears of spiking defaults and lower returns impacting investor confidence.

Outflows from US private credit funds reached a crescendo last week, with famed lender Blue Owl (NYSE: OWL) announcing investor redemption requests for 1Q26 totalled $US5.4bn from two of its funds with significant software exposure. Investors in OWL’s Credit Income and Technology Income funds asked for an incredible 22% and 41% of their capital to be returned. For both funds, redemptions are now effectively gated, limited to 5% per quarter in accordance with the funds’ Business Development Company (BDC) structures, resulting a frustrated queue of investors wanting liquidity.

OWL’s share price is now down two-thirds from its peak in early 2025. By contrast, OWL’s Credit Income Fund $A bonds, which are effectively secured against the fund’s underlying assets, are less impacted and continue to hold their value (refer Chart 1). These bonds are protected by a significant equity cushion, with fund leverage at just ~0.7x, redemptions gated and a BDC mandated leverage covenant limit in place of 2x.

Chart 1. Blue Owl’s debt investors are faring much better than its shareholders

Source: YCM, Bloomberg, Apr 2026.

While we don’t have the software concentrations, Australian private credit is significantly more exposed to the riskier side of real estate lending, especially higher yielding commercial and residential development. In many ways, private credit’s exponential growth since the GFC was a meeting of minds, with local investors understanding Australian real estate and its resilience through multiple cycles; comfortable loan-to-value completion ratios have acted as a powerful magnet for yield hungry investors.

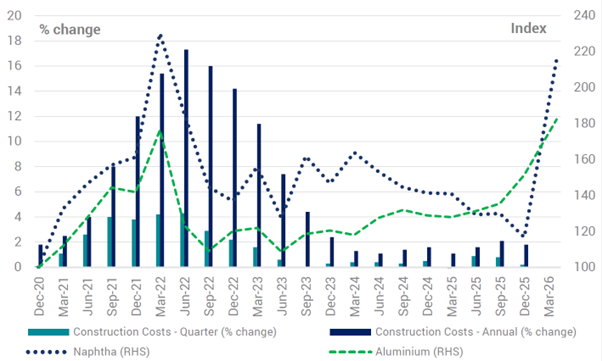

This brings us back to the current Iran conflict and the impact of inevitable cost escalations and higher interest rates on construction sites across Australia. Already weakened through the 2022/23 period of higher interest rates and cost escalations, property development/construction is enduring another round of higher costs (refer Chart 2) and constrained demand. For instance, since the commencement of hostilities, naphtha and aluminium prices – key components in plastic and metal building products – have increased by 85% and 20% respectively. Moreover, in being highly correlated (i.e. increased costs impact all developments similarly), a diversity of development exposures might offer only limited protection from credit losses given the systemic risk profile.

Chart 2. The outlook for construction costs appears grim

Source: YCM, Bloomberg, Apr 2026.

This confluence of events, if sustained, is likely to fuel similar redemption pressures in Australia, with more pure play private credit funds likely to close their liquidity gates in the months ahead. While actual losses will most likely be lower than feared, being unable to meet redemption requests for funds that have been marketed with a ‘promise’ of ungated monthly or quarterly liquidity will be damaging to the private credit landscape.

Private credit’s current travails illustrate the benefits of truly diversified higher yielding portfolios. Our Higher Income Fund blends appropriate risk for commensurate returns across a wider opportunity set of multi-sector Australian credit, providing genuine liquidity and price transparency at mark to market levels.

With yields approaching 7%, our Higher Income Fund is designed to meet investor needs for strong and defensive monthly income from a liquid portfolio which caps private credit investments at 20% (currently ~11%) and has no direct exposure to commercial or residential real estate development lending.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 20 April 2026. This document was originally published in Livewire Markets on 20 April 2026. This information has been prepared by Yarra Funds Management Limited (ABN 63 005 885 567, AFSL 230 251). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.