The politics of oil: why Australia is paying the price

Jason Teh | Vertium Asset Management

The 2026 Hormuz crisis is not solely a story of physical supply disruption. It is a story of deliberate policy choices by major powers, beginning with a US financial manoeuvre in Venezuela that stripped China of its energy insurance policy, followed by Washington's strikes on Iran that closed the Strait, compounded by Beijing's defensive response, and briefly extended by Washington's own contemplation of an export ban. The pattern is not accidental: the powers that control oil supply ring-fence it for domestic use when it suits them, leaving the economies at the end of the supply chain to absorb the consequences.

America First in Caracas

For many years, China kept Venezuela's oil industry on life support through large loans repaid not in cash but in oil. Venezuelan crude reached China through two parallel channels: structured equity and debt-repayment flows managed by state oil companies, and discounted spot barrels purchased by independent teapot refiners through the shadow fleet. Venezuela sat outside the Hormuz chokepoint and Washington had taken notice. The Trump administration's National Security Strategy explicitly sought to deny non-hemispheric competitors access to Western Hemisphere resources, and Venezuela was the most direct expression of Chinese energy influence in the Americas.

Following the removal of President Maduro in January 2026, US authorities reopened Venezuelan oil to US entities while making it difficult for Chinese participation. In an instant, Beijing lost the supply, the debt repayment stream, and its political foothold. It was a deliberate dismantling of a strategic investment built over two decades, executed at the moment China's energy security was about to be tested by war in the Gulf.

America First in Tehran

The strikes on Iran on February 28 were months in the planning. Nuclear negotiations in February had been progressing but Washington concluded that diplomacy had been exhausted and a nuclear-armed Iran posed an unacceptable threat. The operation targeted Iran's nuclear facilities, ballistic missile infrastructure, and senior leadership, killing Supreme Leader Ali Khamenei in the opening strikes.

The stated objectives were nuclear containment, regime change, and elimination of Iranian proxies. Energy consequences were not a feature. Iran's response to the attacks closed the Strait of Hormuz. The burden fell most heavily on others — on Asia, on Europe, and on every import-dependent economy that had no seat at the table when the decision was made. The United States, a major oil producer with domestic supply insulated from Hormuz, was far better placed to absorb what followed.

China First, Then Seoul

When US and Israeli strikes on Iran triggered the effective closure of the Strait of Hormuz, China faced a compounded energy security shock. With just over half of its seaborne crude imports transiting the Strait, Gulf supplies were suddenly inaccessible, and the Venezuelan cushion had already been stripped away.

Beijing's response was clear from the second week of the crisis. On March 11, a blanket suspension of gasoline, diesel, and jet fuel exports took effect. The following day, Sinopec's request to access 95 million barrels of national commercial reserves was denied. On March 23, China's National Development and Reform Commission intervened in domestic fuel pricing, absorbing roughly half the formula-derived increase to shield consumers from the surge in global crude prices. South Korea followed within 48 hours of China’s first measure. On March 13, the Ministry of Trade, Industry and Energy introduced mandatory export caps on refined oil products alongside domestic wholesale price ceilings.

China and South Korea are the two largest exporters of refined products in the Asia-Pacific region, together supplying 2.5 mbpd to international markets in 2025. China, holding an estimated 90–120 days of strategic reserves, chose to suspend 1.2 mbpd of exports rather than deploy its reserves. China's withdrawal compounded the 5 mbpd of refined products already trapped inside the Strait, removing a combined 6 mbpd from international buyers simultaneously. South Korea, exporting approximately 1.3 mbpd in 2025, faced an immediate dilemma. Buyers scrambling to replace Chinese volumes would likely have driven demand well above the 1.3 mbpd pace South Korea had been running. In response, South Korea, holding nearly twice China's reserves at 208 days, capped refined product exports at 2025 monthly levels, preserving its crude stocks against a demand pull it had not created and could not control. Both had buffers but chose not to deploy them, leaving importers downstream to fend for themselves.

China and South Korea are not alone in turning inward. Thailand also imposed a full export ban, but from a position of genuine scarcity. With reserves of only 38 days against a 60-day target, Bangkok was protecting itself from collapse, not ring-fencing comfortable buffers. At 0.07 mbpd, a fraction of China's or South Korea's, Thailand's ban removes little from the regional market. Each country reached a similar decision but had different motivations: China suspending most exports despite comfortable reserves; South Korea capping exports to defend its reserves against the demand surge China's ban created; and Thailand banning exports entirely out of necessity rather than choice.

America First Again?

Around March 19, speculation emerged that the Trump administration was contemplating the same playbook — restricting crude and product exports. The Brent-WTI spread blew out to $10 per barrel before the White House denied it. The logic was superficially identical, but the economics were not. The US exports ultra-light sweet crude of a grade its Gulf Coast refineries, configured for heavy sour crude, cannot absorb. Trapping those barrels domestically would not have relieved feedstock constraints but would have caused light crude inventories to swell. Gulf Coast refiners were already capturing extraordinary margins on the heavy sour grades they were running, including the Venezuelan crude redirected by Washington's January policy, and had no economic incentive to switch.

The export ban was never imposed, but its contemplation highlighted a recurring theme. Three separate decisions: Venezuela, Iran, the export ban. Each made in America's interest. None considered the cost to others.

The World Pays the Price

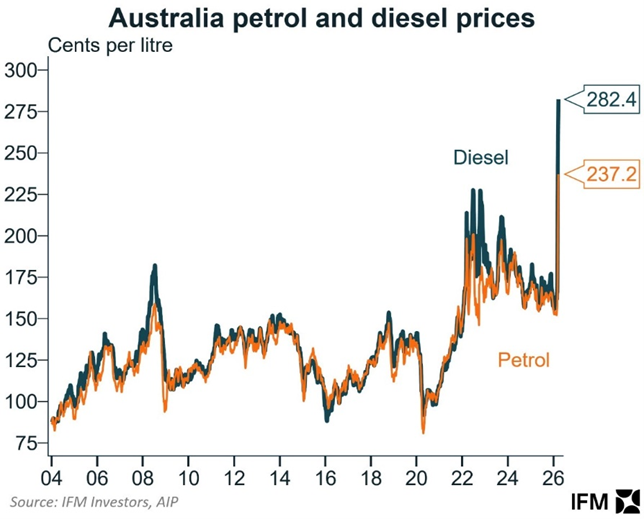

Refining margins surged as the Strait closed, reflecting a physical feedstock shortage rather than risk premium. Brent crude surged from $70 per barrel before the conflict to above $100. Singapore complex margins jumped to $30 per barrel, the highest in nearly four years, with jet fuel and diesel cracks leading the rally. Australian retail petrol prices followed within days, reaching record levels as the supply chain disruption worked its way downstream to the pump.

The supply shock operates through two distinct mechanisms: export controls, which remove volume from international markets, and refinery run cuts, which remove volume from global supply entirely. Refinery run cuts affect everyone equally, domestic consumers and international buyers alike. Less crude being processed means less product exists. Unlike export controls, run cuts cannot be reversed by a policy decision. They require feedstock to return before refineries restore runs.

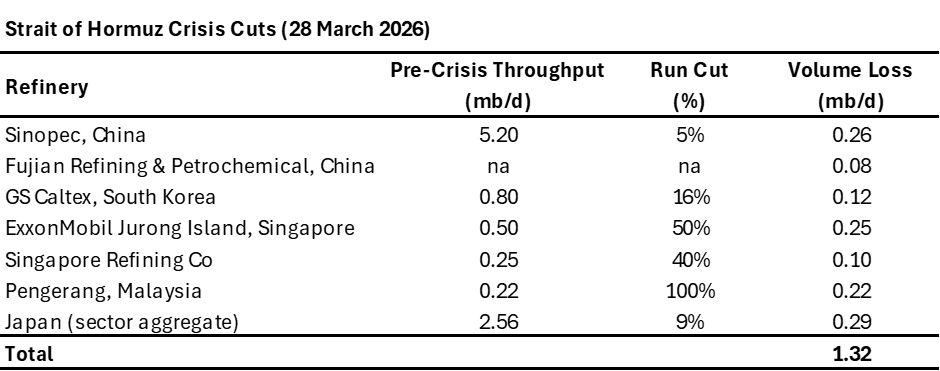

In contrast to China and South Korea, Japan chose cooperation over restriction and still fell short. Tokyo imposed no export restrictions and deployed its largest ever strategic reserve release to keep refiners running. The reserve release helped but Japanese refineries remain below their pre-war utilisation rate of 82.7%, with current utilisation of 73.3% implying a shortfall of 0.3 mbpd. Together with confirmed cuts across China, South Korea, Singapore, and Malaysia, cumulative run cuts across the region now stand at approximately 1.3 mbpd and the worst is still ahead.

Sources: Sinopec — FY2025 results briefing, 23 Mar 2026; GS Caltex — Seoul Economic Daily, 25 Mar 2026; FREP, ExxonMobil Jurong Island, Singapore Refining Co, Pengerang — Reuters, Mar 2026 (industry sources and Kpler); Japan — PAJ weekly data.

Sources: Sinopec — FY2025 results briefing, 23 Mar 2026; GS Caltex — Seoul Economic Daily, 25 Mar 2026; FREP, ExxonMobil Jurong Island, Singapore Refining Co, Pengerang — Reuters, Mar 2026 (industry sources and Kpler); Japan — PAJ weekly data.

The more consequential pressure builds in April. Chinese teapot refiners, independent operators representing 25% of China's refining capacity, have no state backstop and no remaining feedstock options. Their model was built around discounted sanctioned crude from Venezuela, Iran, and Russia. Venezuelan crude has been redirected, Iranian crude is trapped, and Russian grades, now partially unsanctioned under US waivers, are being competed away to India. All three sources have effectively closed. Their only remaining buffer was about 10 weeks of on-site inventory as of early March, now significantly depleted, burning through at 2.8 mbpd. When exhausted in late April, teapots face a binary decision. There is no stable operating point between minimum economic throughput and full shutdown. If feedstock cannot be secured, the full 2.8 mbpd disappears, more than double the 1.3 mbpd of confirmed run cuts that have already helped send regional margins to their highest levels in years. They are the most exposed refining sector in Asia with the least policy protection and the shortest timeline to a cliff.

What This Means for Australia

Australia is almost entirely dependent on imported refined product. Ampol's Lytton and Viva Energy's Geelong refineries cover less than 20% of national demand and have been directed to dedicate their entire output to domestic supply, but they cannot close the gap. The remaining 80% arrives by ship from South Korea, Singapore, and Malaysia, whose collective crude intake is 59% Strait-dependent. South Korea and China supply approximately half of Australia's fuel imports directly and have both ring-fenced domestic supply. Contracts should proceed but top-up cargoes beyond contracted volumes are limited, and emergency cargoes have already been chartered from the US Gulf Coast at significantly higher cost. Australia's reserves of 29 days of petrol and 25 days of diesel are depleting with no obvious replenishment path. Even if the Strait reopened tomorrow, Kuwait Petroleum Corporation's CEO warned it will take three to four months to restore shut-in Gulf fields before the recovery chain can begin.

Australia did not cause this crisis, but it is paying for it, and it was not prepared for it. Washington redirected Venezuelan crude and struck Iran, closing the Strait. The energy cost fell elsewhere. Beijing ring-fenced its reserves and banned exports despite holding comfortable buffers. Seoul, sitting on far greater reserves, protected its own. Each decision served a domestic purpose and none was made with any reference to the countries at the end of the supply chain. Australia, with 29 days of petrol, had no such choice. Meanwhile Australia, the only IEA member in persistent breach of the 90-day reserve requirement, has offered only soft guidance with no mandatory demand reduction measures — well short of the conservation policies other IEA members have already implemented. The vulnerability was known and the warnings were ignored. It sleepwalked into a crisis it had been warned about for over a decade.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 29 March 2026. This document was originally published in Livewire Markets on 29 March 2026. This information has been prepared by Vertium Asset Management Pty Ltd (ABN 25 615 639 659), a Corporate Authorised Representative (Corporate Authorised Representative Number 001258758) of Clime Asset Management Pty Ltd (ABN 72 098 420 770), AFSL 221146. The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.