Summer Lovin – Happened so fast!

Henry Jennings | Marcus Today

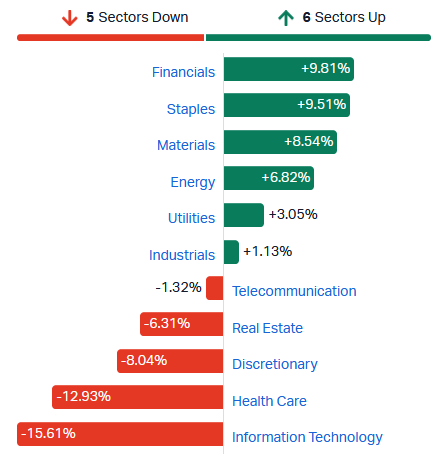

The market has rallied to record highs, primarily propelled by the resource sector and the banks, both of which have enjoyed a staggering run.

Average price move post results +3.2% - Out of the 274 results - 47 moved up over 10% - 39 moved down more than 10% - 51 dropped over 5% - 90 rose over 5%.

But it hasn’t all been oranges and sunshine. There have been some high-profile casualties. CSL and COH. TPW and ZIP have also had battalions of issues. So too has AMP. And market darling PME.

The tech sector has come under immense pressure, following the US software meltdown we have seen and the question marks over the SaaS business models. However, there are now signs of life. The results from WiseTech (WTC), along with the announced job cuts of around 2,000 roles over the coming years, sent a strong message to the market, and the tech sector is starting to rebound.

Source: Marcus Today

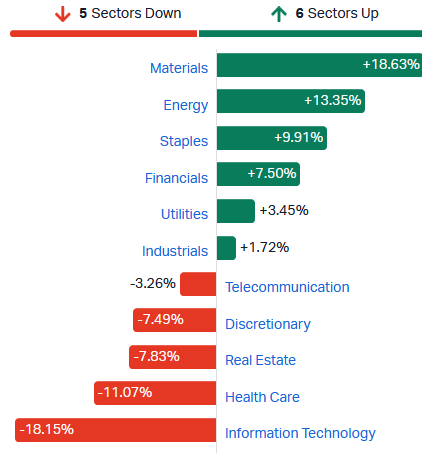

And year to date tells a similar story.

Source: Marcus Today

Many readers will know that I have long been a bull on the commodity sector — whether it be gold, copper, critical metals, rare earths or uranium. To me, commodities still represent good value. We have seen price rises across the board, and while some commodities are off their ‘spike’ highs, miners, explorers and producers don’t need spike prices — we simply need a higher-for-longer commodity price complex.

Part of this rush into commodities is the growing belief that countries must hold strategic stockpiles and develop supply chains that are not easily disrupted by the two major superpowers.

Gold has been the obvious port in a storm, as central banks continue to buy gold as a hedge and a diversification away from the US dollar and the de-dollarisation trend we are seeing. There is little doubt in my mind that the US dollar will continue to drift lower this year. That is part of Project 2025, or even the so-called Mar-a-Lago Accord, which has a lower dollar as one of its centrepiece policies to improve export competitiveness.

There is also no doubt that the US President wants lower interest rates, and Kevin Warsh is seen as the man to deliver that. It is hard to believe the Fed is even contemplating rate cuts, given where the US economy currently sits. GDP is still growing strongly, and all that recession talk from several years ago — soft landings, hard landings — well, all we’ve really had is a vertical take-off.

Here in Australia, given the index composition of our market, the defensive qualities of the banks — which generate $30bn-plus in cash profits every year — combined with the dominance of BHP as the world’s largest miner, now earning over 52% of its profits from copper, make it understandable why our market is sitting at record highs. With copper prices continuing to trend higher, the picture remains supportive.

The reporting season has shown a fairly robust corporate outlook overall. Those who disappointed have been punished — and punished quickly. That said, some of the punishment meted out by the algos and aggressive hedge funds has been reversed the following day after more careful analysis of the results and underlying forward drivers.

The real standouts have been the resource stocks, with BHP in particular up over 8% this month on the back of very strong numbers and, more importantly, its ability to find extra cash ‘down the back of the sofa’ to further bolster its balance sheet. That extra cash came from silver streaming royalties, following a deal with Canada’s Wheaton for US$4.3 billion — a royalty stream the market had previously ascribed little to no value to. By comparison, Rio Tinto (RIO) is still trying to simplify its structure after its aborted attempt to merge with Glencore.

With a solid banking backdrop, a strong resource sector, and a technology space that is now showing green shoots and pushing higher, we could see the market kick on in March as we head into Easter and the May Budget. There are risks — as the market goes ex-dividend following results, we could see some drift lower — and of course we remain subject to the volatility and vagaries of the US market. Still, it feels as though the market wants to continue pushing higher.

Many sectors have performed well, but just as many have not participated in this rally. Despite an environment where rates are expected to rise again after monthly inflation came in at 3.8%, the market has largely shrugged this off. That’s certainly positive for the Aussie dollar, good for bank margins through net interest margin (NIM) expansion, and there is still no real sign of bad debts emerging.

If the technology sector were to rebound toward broker valuation targets, we could see the market push toward 9,500 before the Easter break. That may be a stretch, but we know bank results will be solid, dividends will be robust — if not higher — and with strategic moves underway in commodities to build resilient stockpiles and supply chains, it appears the likes of BHP and RIO will continue to grind higher.

Gold miners are also enjoying these conditions, with recent results showing substantial cash piles building. As I’ve said before, it’s not about gold spiking to $5,500 or higher — it’s about gold staying at elevated levels. Every day gold sits around $5,000 is another day miners are banking extraordinary margins.

Looking beyond gold, BHP’s outlook on copper points to a looming supply deficit. As one of the world’s largest copper producers, BHP is exceptionally well-positioned to capitalise. Again, copper prices don’t need to go crazy — they just need to stay higher for longer. And don’t forget iron ore, which has been languishing. If that were to lift back toward $105–$110 a tonne, we could see another leg higher in the resource sector — also supportive for the local economy heading into the May Budget.

All up, it remains a very bullish market scenario. We’ve shrugged off the killing season. Volatility has been high, no doubt, but those who stuck to their investment thesis and backed quality stocks have been rewarded.

Last August’s results were lacklustre, followed by a very weak September as stocks went ex-dividend and pressure mounted. This February feels like the opposite. The mood is far more optimistic than it was last reporting season. Summer Loving! Happened so fast!

That said, it’s still not an easy market. It remains a stock-picker’s market, and you need to be positioned in the right themes. Those themes have been banks and commodities, not technology and IT. Are we about to see that sector turn, with money rotating out of banks and back into tech?

We shall wait and see. Tell me more! Tell me more!

A free trial of the Marcus Today newsletter for nabtrade clients is available here.

All prices and analysis at 26 February 2026. This information has been prepared by Marcus Today Pty Limited. Marcus Today Pty Ltd ABN 57 110 971 689 is a Corporate Authorised Representative (no. 310093) of AdviceNet Pty Ltd ABN 35 122 720 512 (AFSL 308200). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.