Monthly market views: AI disruption and dollar hedging

Chris Iggo | BNP Paribas Asset Management

Big technology companies are expected to invest up to $650 billion on computing capacity and datacentres during 2026.

The tech bond boom

Free cash flow generation has remained strong, but tech companies are increasingly using their solid credit ratings to tap the bond market to raise money. The Technology and Electronics segment represented 6.48% of the ICE BofA US Corporate Bond index as of the end of January – and that is set to grow. For bond investors, this is interesting.

The growth in technology firms’ issuance adds further potential for diversification, and – in some cases – also provides much-needed duration to the bond market, offering a stable source of coupon income. Leverage across the sector is low at around 0.3 times earnings, compared to the S&P 500 average of 1.6 times, and revenue is growing strongly.

For some investors, owning high-growth technology company bonds might be an attractive complement to increasingly volatile shares. However, as in the equity market, there may be performance differences between hardware and software issuers, with the latter’s future revenue streams likely to be more challenged by AI.

Another source of volatility

The outbreak of conflict in the Middle East is likely to be a source of volatility for financial markets. The early response has seen an increase in oil prices, a slightly stronger dollar, lower equity markets and wider credit spreads.

The extent to which these market moves are sustained depends on how the conflict unfolds. If the intention of the US and Israel is to achieve regime change in Iran, then there are numerous uncertainties over how long this might take, and what the repercussions in terms of regional stability might be. If this is the case, the market and macro implications will be greater. We will monitor the situation closely to see how it potentially impacts our core investment views.

The AI narrative evolves

While the primary source of market volatility has moved from geopolitics back to AI, this time it comes with a twist. Instead of fears of an AI bubble, attention has turned to the potential damage to business models and employment.

The significant capital expenditure increases announced by several AI developers exacerbated worries about the outlook for corporate profits. The disruptive part of ‘creative destruction’ will likely impact some industries profoundly, but there will in turn be new opportunities that follow.

Even as the Nasdaq 100 index is still below its end-of-January peak at time of writing, most other markets have continued to rise. Of particular note is the 5% gain for emerging market technology stocks thanks to the larger weight of tech hardware, which will underpin the further buildout of datacentres.

The lesson for investors is not only the need for diversification (one doesn’t know where the next disruption will come from or who will benefit), but also the benefits of active management. Given the high dispersion of returns across stocks, the ability to overweight winners and avoid losers will be a critical driver of outperformance.

Dollar hedging: Cheaper for now

Hedging US dollar exposure in European portfolios has become cheaper – falling to 170 basis points recently, after peaking at 240bp last summer. The cost is expected to fall further to 115bp in 12 months’ time before stabilising at around 95bp over the medium term.

This projection is based on market expectations around the European Central Bank and US Federal Reserve’s interest rate trajectories. The ECB is expected to pause its rate cutting cycle for the rest of 2026, but there is a high level of uncertainty surrounding the Fed’s next steps – while the market is pricing in almost 55bp of cuts by December 2026, the Fed’s monetary policy committee removed the warning of ‘downward risks to employment’ from its January statement.

The US economy is forecast to expand by 2.4% in 2026, according to the consensus, while inflation is predicted to remain stubbornly above the Fed’s 2% target – meaning market-based expectations for rate cuts are by no means cast in stone. In this scenario, hedging US dollar exposure might be slightly more expensive going forward.

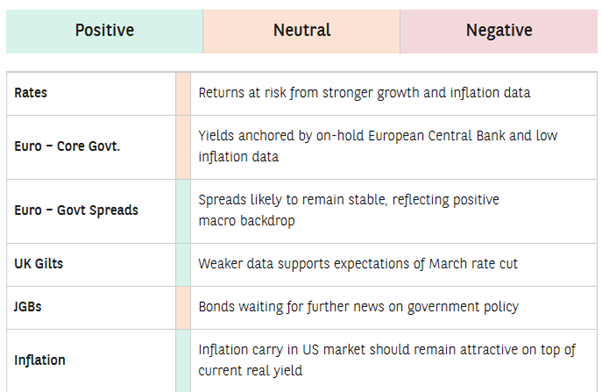

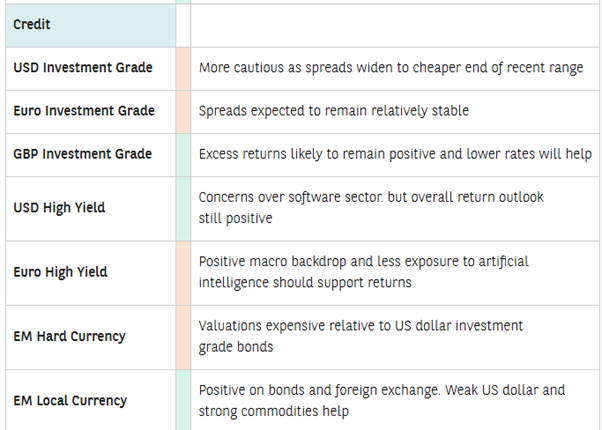

Asset class views

Opinions draw on investment team views and are not intended as asset allocation advice.

BNP Paribas Asset Management has identified several themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Automation & Digitalisation, Consumer Trends & Longevity, the Energy Transition as well as Biodiversity & Natural Capital; source: BNP Paribas Asset Management.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 12 March 2026. This document was originally published in Livewire Markets on 17 February 2026. This information has been prepared by BNP PARIBAS ASSET MANAGEMENT Australia Limited ABN 78 008 576 449, AFSL 223418). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.