A sustained energy shock would raise the risk of recession

Kieran Davies | Coolabah Capital

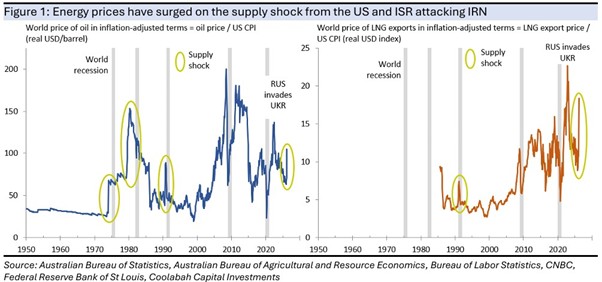

Oil prices remain extraordinarily volatile and are currently about 45% above pre-Iran-war levels as the market tries to estimate how long the Strait of Hormuz might be blocked. LNG prices are up by more because Qatar has halted production, currently about 70% above pre-war levels.

The war has reduced the world supply of oil by about 20%, with the world supply of gas down about 4%. The IEA release of 400m barrels of oil from reserves will cover the shortfall in the supply of oil for about 20 days, assuming full compliance, while some additional oil could be exported via existing pipelines. The US is seeking a more lasting military solution by trying to form a coalition of selected advanced economies and China to escort ships through the Strait of Hormuz.

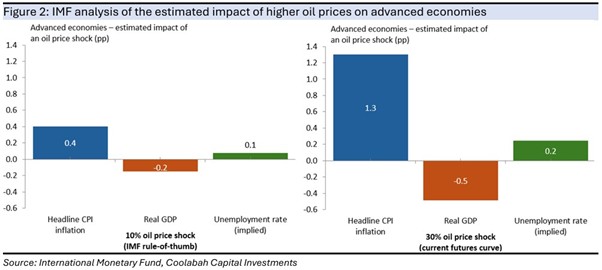

Some central banks might release their modelling this week, but the IMF recently published its estimated impact of an oil price shock for advanced economies. Scaling the IMF analysis, a roughly 30% increase in the price of oil – which is what is currently factored into the futures curve for the rest of this year – would boost headline inflation by about 1¼pp. The risk to headline inflation seems greater this time around because the closure of the Gulf is likely to affect food prices via the reduced supply of fertiliser and goods prices via the lower supply of key industrial chemicals.

In this scenario, GDP would be around ½pp lower on the IMF’s figures. Based on the usual relationship between activity and the labour market, this points to an increase in the unemployment rate of about ¼pp, consistent with a sharp economic slowdown, but not recession.

As for the impact of higher oil prices on core inflation, past central bank analyses regularly show a small, sometimes negligible, effect, although that hinges on inflation expectations remaining anchored to inflation targets. Higher expectations would lead to sustained higher core inflation, which is why central banks are likely to talk tough about the upside risk to inflation posed by the war with Iran.

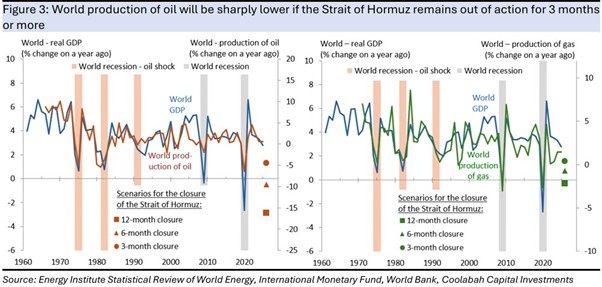

More generally, a sustained reduction in the world supply of energy points to an increased risk of recession. The world economy has become less dependent on oil over time, but growth in world GDP is still highly correlated with growth in the global production of both oil and gas, such that a long blockade of the Gulf would raise the risk of recession.

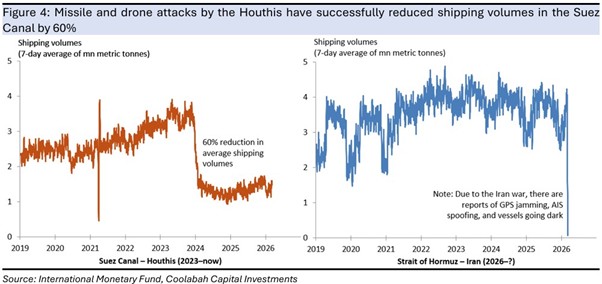

A US-led coalition of warships might change things, but Iran could continue to attack ships, hampering a return to pre-war shipping volumes. In this respect, it is worth noting that the Houthis have successfully reduced shipping volumes through the Suez Canal by about 60% since they first started attacking vessels with drones and missiles in late 2023.

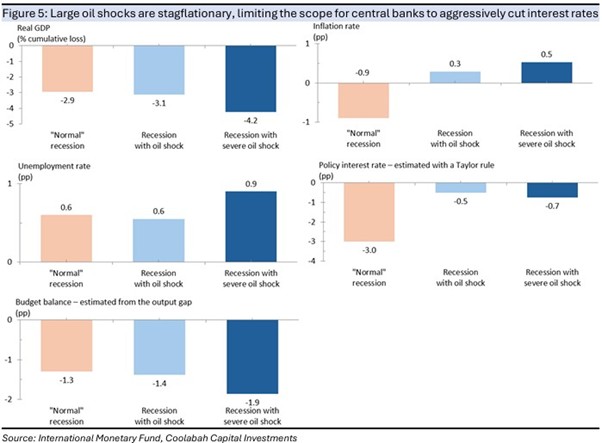

If a recession is realised, an IMF study of business cycles shows that recessions associated with oil shocks are stagflationary, with both higher inflation and higher unemployment. In a “normal” recession, a central bank cuts rates aggressively, usually from a starting point of high interest rates. Stagflation greatly complicates things and a simple policy rule based on the usual increase in inflation and unemployment seen in an oil shock points to little change in interest rates.

Moreover, there is the clear risk that central banks nowadays would seek to avoid the policy mistakes of the 1970s, responding with higher interest rates if inflation expectations drifted higher.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 16 March 2026. This document was originally published in Livewire Markets on 16 March 2026. This information has been prepared by All prices and analysis at 16 March 2026. This document was originally published in Livewire Markets on 16 March 2026. This information has been prepared by Coolabah Capital Ltd ACN 153 555 867. Coolabah Capital Investments (Retail) Pty Limited (CCIR) (ACN 153 555 867) is an authorised representative (#000414337) of Coolabah Capital Institutional Investments Pty Ltd (CCII) (AFSL 482238). Both CCIR and CCII are wholly owned subsidiaries of Coolabah Capital Investments Pty Ltd.The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.