Finding value in the Aussie mining sector

Tyger Fitzpatrick | Morningstar

Gold and iron ore have been the main drivers of this rally. Iron ore prices are up 11% from last quarter, mainly driven by optimism over Chinese stimulus and steel capacity cuts. The gold price has surged to an eye watering $4,100 USD per ounce, largely driven by ETF inflows, strong central bank buying and a weaker US dollar. These recent developments raise a key question for investors. Where should I look for value in the mining sector?

I will breakdown the key sectors that are materially undervalued according to our analysts and discuss three Aussie mining stocks that are trading at a discount to their fair value.

Is the mining sector overvalued?

The mining sector’s unweighted average price to fair value (P/FV) estimate has risen from 1.01 to 1.27 over the past quarter. At face value, this metric would suggest the mining sector is moving into materially overvalued territory. However, this is not the full picture.

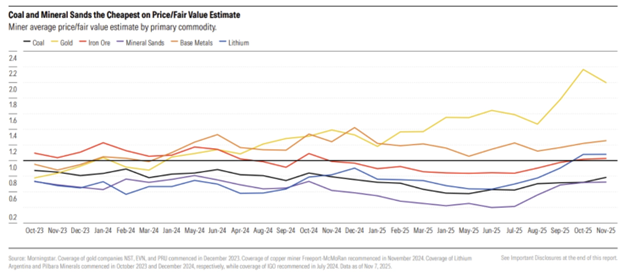

The primary driver of this valuation increase has been the inflow of investment in gold mining stocks. Gold mining companies are trading at an eye watering 2 times fair value while the second highest group being base metals (copper, aluminium etc.) sitting at 1.2 times.

In contrast, coal and mineral sands are currently the cheapest on P/FV basis with an average of 0.8. ASX listed New Hope and Whitehaven are noted as substantially undervalued due to continued downward pressure on thermal coal prices. Iluka, a dominant player in mineral sands, is also priced at a 21% discount to our analyst’s fair value estimate.

Lower lithium prices have pushed global leading producers such as Albemarle and SQM into undervalued territory. However, the unweighted lithium miners average P/FV sits at 1.1 suggesting an uneven spread of value across the Lithium space. Iron ore miners, led by BHP and Rio Tinto look fairly priced on a P/FV multiple while outliers such as Mineral Resources are priced at a 27% discount to Fair Value.

Mineral Resources (ASX:MIN)

- Fair Value Estimate: $68 (27% discount at 20 November)

- Rating: ★★★★

- Moat: None

Our analysts identified Mineral Resources as one of the cheapest iron ore producers in their coverage. Mineral Resources generates revenue in three core segments. Iron ore, lithium and mining services. Our analysts believe MIN is undervalued to due fears surrounding its balance sheet and cyclically low lithium prices.

There are two key earnings drivers for Min Res looking forward into 2026. One being the ramp up of the Onslow iron ore mine. The second is the general recovery in lithium prices to the marginal cost of production (20,000 USD per metric tonne). These two tailwinds are expected to drive a deleveraging of MIN’s balance sheet going forward.

New Hope (ASX.NHC)

- Fair Value Estimate: $5.50 (27% discount at 20 November)

- Rating: ★★★★

- Moat: None

Weak thermal coal prices have pushed downward pressure on New Hope’s share price, with our analysts concluding the company is materially undervalued. Our analysts expect strong demand for high quality thermal coal from regions such as Southeast Asia over the next decade.

New Hope also has a 23% stake in the Malabar-Maxwell mine in NSW, which gives the company some diversification into metallurgical coal. In terms of pricing, new thermal coal supply is constrained by regulatory and ESG factors. With tight supply, we expect to see longer term upside in the commodity price. It is worth noting New Hope has a higher uncertainty rating which derives from ESG pressures and regulatory uncertainties. New Hope’s dividend policy is to pay 25% of EBITDA which our analysts see as appropriate given the cyclical nature of coal prices. The company has a very strong balance sheet with net cash of $330 million. The current yield is 6.1% which is 100% franked.

Deterra Royalties (ASX:DRR)

- Fair Value Estimate: $4.40 (14% discount at 20 November)

- Rating: ★★★★

- Moat: Wide

Deterra Royalties manage a portfolio of royalties in the resource sector. Our analysts liken Deterra’s business model to a toll road with leverage to the iron ore price. The primary asset is the MAC royalty agreement with BHP which represents 90% of earnings. This royalty agreement is based on revenue earned rather than profits. This acts as a hedge from inflation costs and margin compression. In fact, our analysts see the royalty asset benefiting from inflation due to higher commodity prices.

The beauty of the business model is it has no operating or capital costs. BHP’s expansion in iron ore production requires no additional capital from Deterra. The key risk is the above-mentioned leverage to the iron ore price. The recent acquisition of Trident was a move to diversify the company’s earnings into other commodities such as Lithium and Gold. However, our analysts expect the MAC royalty to be the main driver of revenue for the foreseeable future. Deterra has a yield of 5.7% fully franked which is supported by a minimum payout ratio of 75% of earnings.

Wrap up

Overall, despite the recent run on commodity prices – there remains pockets of value in this space. Producers of mineral sands and coal remain significantly undervalued while gold producers are priced well above their fair value. Each of the three opportunities outlined in the article are all trading significantly below their fair value estimates, proving pockets of value remain in the ASX mining sector.

Access this research and more at Morningstar. For a free four-week trial, click here.

All prices and analysis at 24 November 2025. This information has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892.). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.