Q3 CPI confirms RBA’s fears on housing and services

Taylor Nugent | Markets Research

Key points

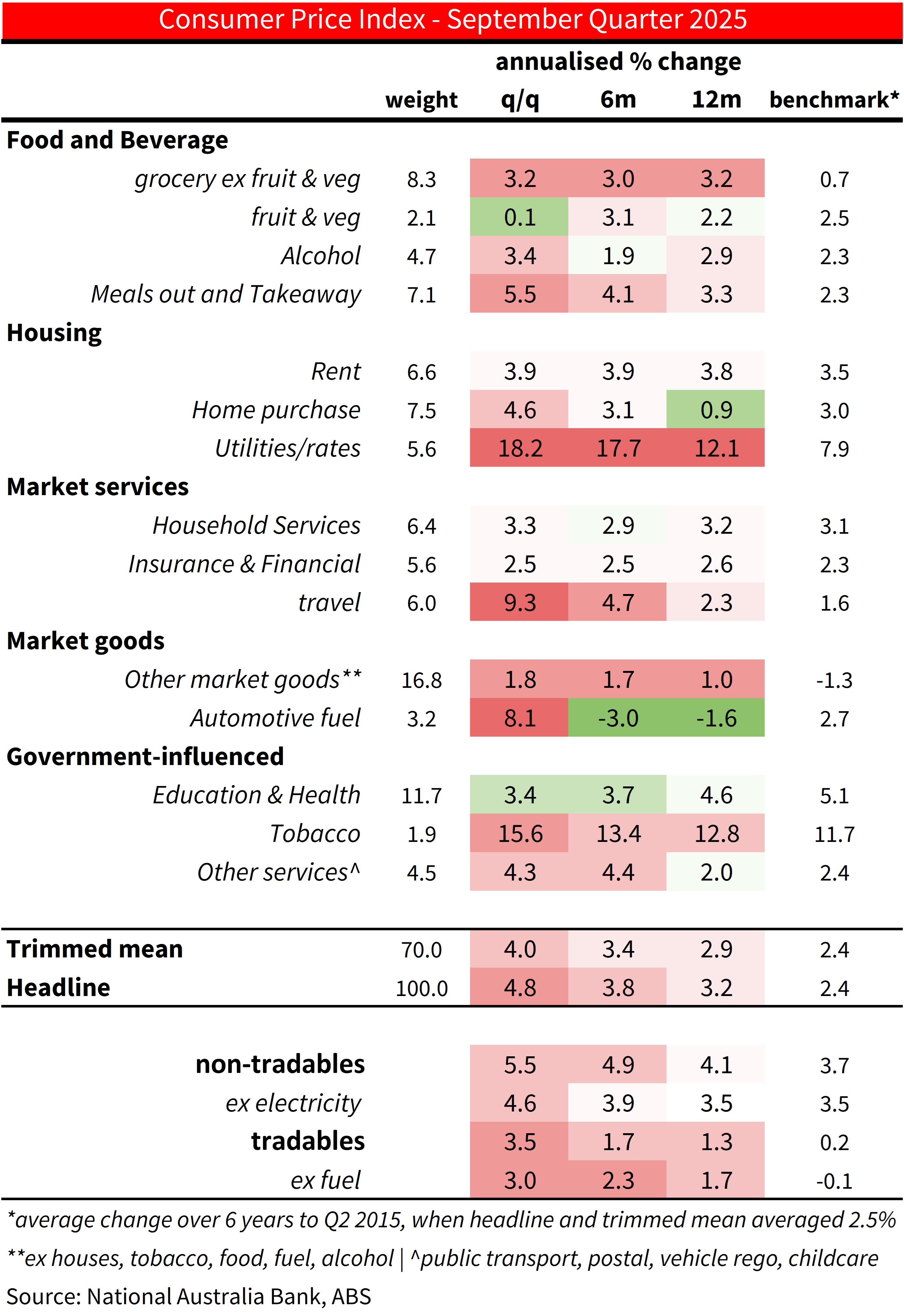

- Trimmed mean was 1.0% qoq and 3.0% yoy (NAB 0.9%, consensus 0.8%)

- Headline was 1.3% qoq (NAB and consensus 1.1%)

- The RBA recently has rightly pointed to housing and services components as a concern

- Market services reaccelerated, in line with the signal from the August indicator

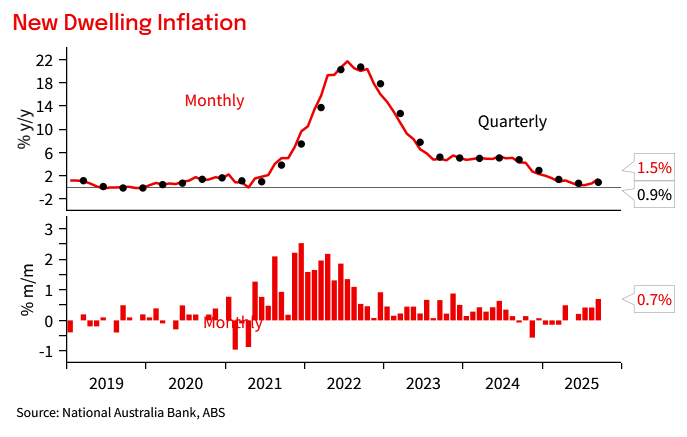

- New dwelling costs were stronger again in September

- NAB continues to expect an extended pause from the RBA, pencilling in a May cut

- GDP and employment data ahead of the December meeting would have to particularly weak to put a cut back in play this year

Assessment

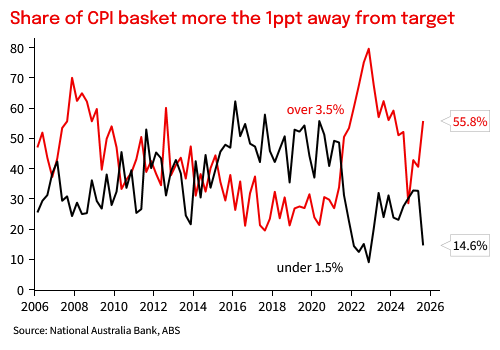

The Q3 CPI data confirmed our read from the partial indicators that inflation was materially above the RBA’s August expectation. Stronger inflation in the quarter was broad based. The share of the CPI increasing more than 1ppt above the 2.5% midpoint rose from 41% to 56%, the share running more the 1ppt below fell from 33% to 15%. That said, volatile travel and the unwind of electricity subsidies were an additional large support to (especially headline) inflation in the quarter. Travel prices contributed 14bp to the seasonally adjusted headline outcome and added utilities 20bp.

NAB continues to expect that the RBA will be on an extended pause, pencilling in a cut in May 2026 as it seeks to gain more understanding of both labour market and inflation dynamics. The RBA has expressed consistent uncertainty around the output gap (with that uncertainty largely related to the supply side), today's data will add to the sense that this is an economy that can't grow much beyond 2% without generating inflationary pressures, particularly in the context of a labour market that shows some residual tightness as a starting point.

After the November meeting and SoMP forecast update on 4 November, employment on 12 November and GDP on 3 December are the key data releases ahead of the December meeting. They would have to particularly weak to put a cut back in play this year.

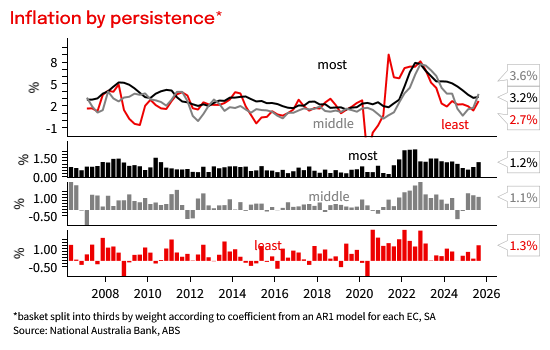

It was a combination of a reacceleration across components, including services, that tend to be more persistent, and large price rises in less persistent components that are volatile quarter to quarter that conspired to deliver today’s very elevated inflation outcome (chart 5). As a result, we do not expect that underlying inflation will continue to annualise at 4% looking over the next few quarters. Even so year-ended trimmed mean inflation will be at or above the top of the RBA’s target range over the next few quarters, and our preliminary Q4 expectation of 0.8% qoq for trimmed mean is still a materially different picture than the RBA’s August characterisation that inflation was annualising near the mid-point of the target.

Detail

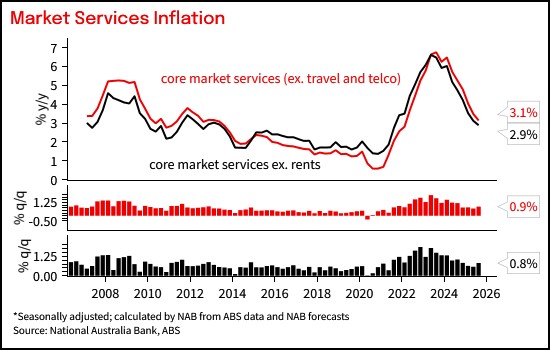

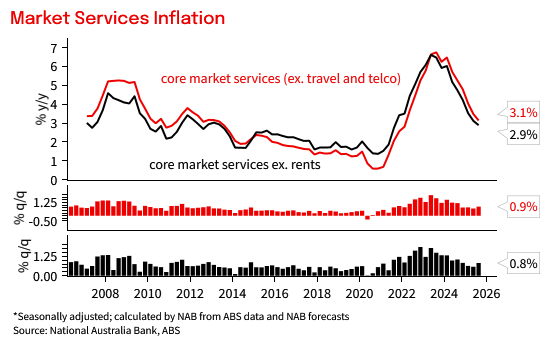

Market services inflation excluding travel and rents, an indicator of domestic inflation pressures that had gradually moderated to a benign 0.6% qoq, was up 0.8% qoq, its highest in a year. Confirming the signal out of the partials in the August CPI Indicator

Across housing components, new dwelling inflation rose 0.7% mom in September. 0.4% mom outcomes in July and August had the RBA nervous, so a further acceleration will add to those worries. Rents, rose 0.2% mom in September after a sustained run of 0.3% mom, but was due to the semi-annual indexation of rent assistance, and do not reflect underlying deceleration. More timely advertised rents and ongoing undersupply of housing, suggest rent inflation will run above overall inflation and wages growth over the next couple of years.

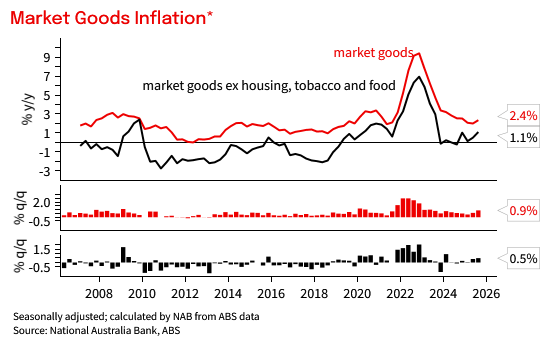

Goods prices excluding new dwelling costs and food and tobacco, rose 0.5% qoq on a seasonally adjusted basis. That was a little less benign than we had pencilled in, largely due to a 0.7% qoq rise in car prices, which tend to be volatile quarter to quarter.

Grocery inflation, ex fresh fruit and vegetables, continued to annualise around 3.0%, similar to its pace over the past year. Coffee, beef, and dairy products were notable supports for food inflation in Q3.

Chart 1: Headline and Trimmed Mean Inflation

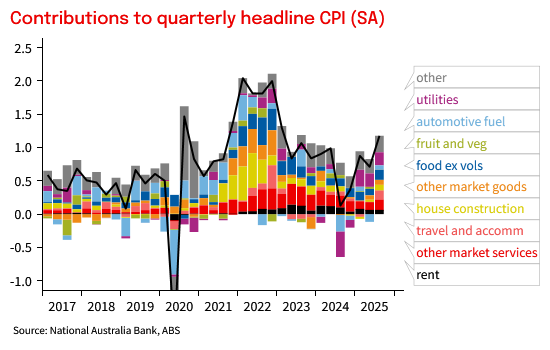

Chart 2: Contributions to CPI inflation

Table 1: CPI heat map. Shows 3-, 6- and 12m annualised outcomes. Shading reflects how far inflation is above or below a benchmark of the 6 years to 2015 when inflation averaged around the mid-point of the target

Chart 3: Market services inflation

Chart 4: Market goods inflation

Chart 5: Inflation by 'persistence'

Chart 6: Share of basket running 1ppt higher or lower than target midpoint

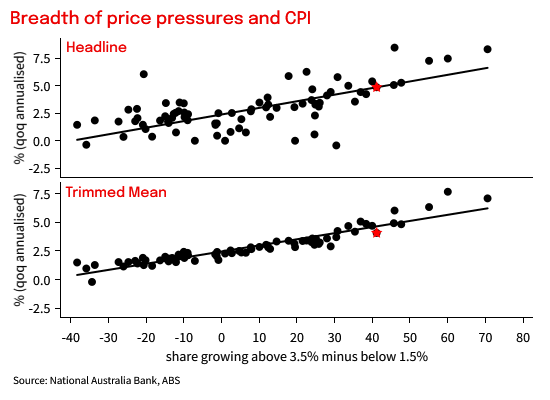

Chart 7: Breadth of inflation compared to headline and underlying outcomes

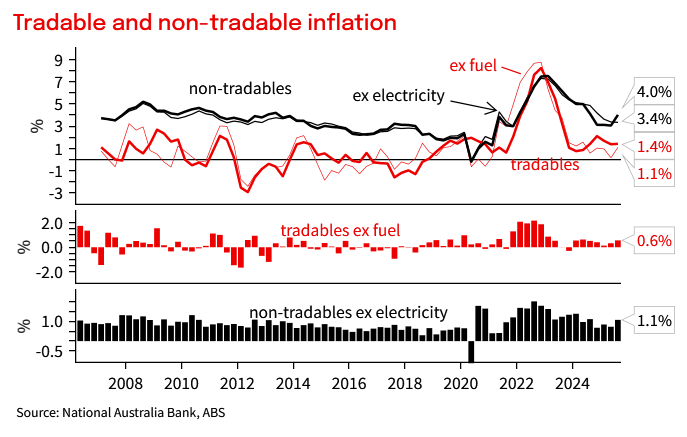

Chart 8: Tradable and non-tradable inflation.

Chart 9: New Dwellings inflation was hot in September

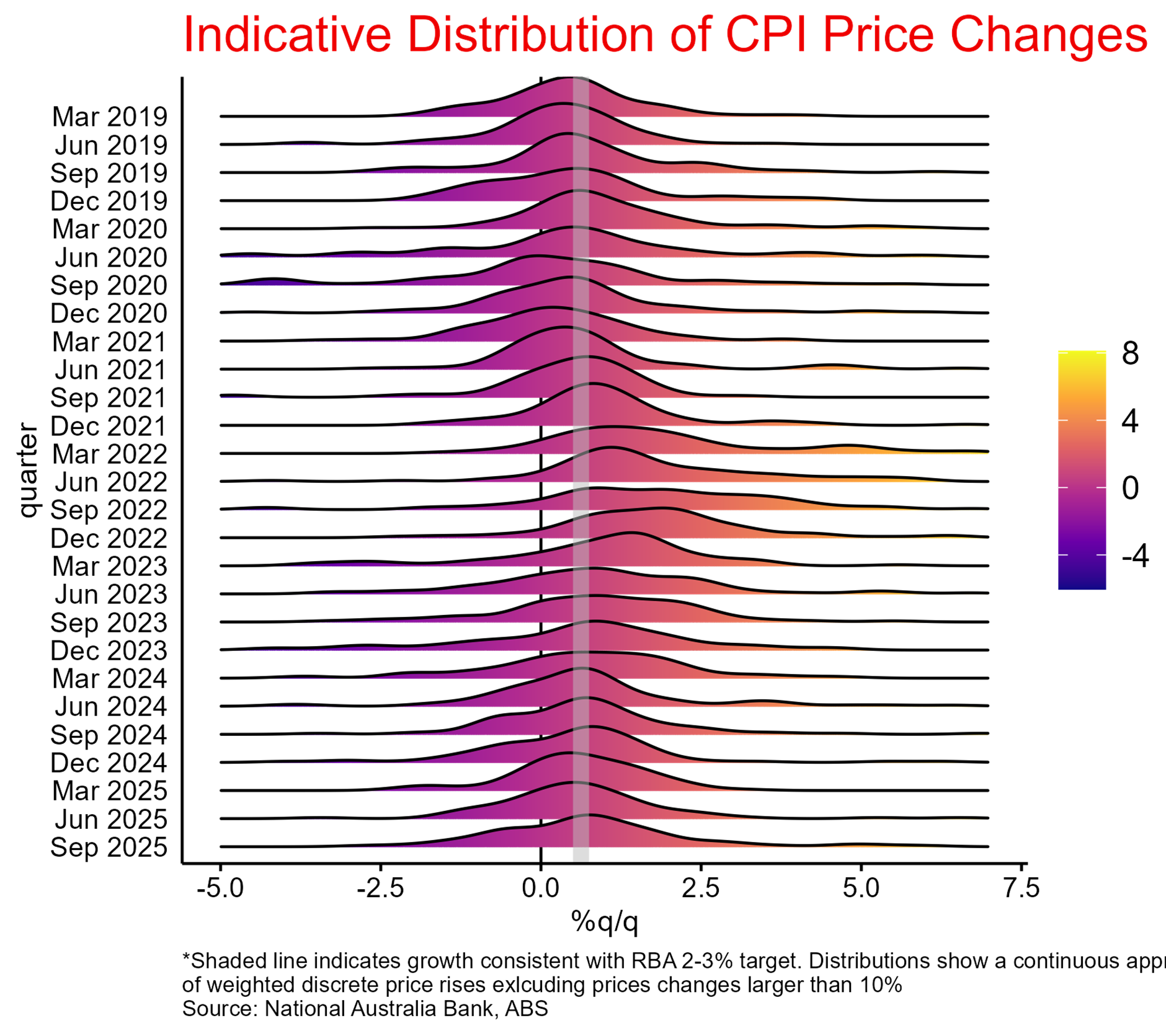

Chart 10: Distribution of price increases

This document has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, NAB recommends that you consider whether the advice is appropriate for your circumstances. NAB recommends that you obtain and consider the relevant Product Disclosure Statement or other disclosure document, before making any decision about a product including whether to acquire or to continue to hold it. Please Click Here to view our disclaimer and terms of use. Please Click Here to view our NAB Financial Services Guide.

All prices and analysis at 29 October 2025. This information has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.