What to Watch - Week of 4 August 2025

Tapas Strickland | Markets Research

Past Week

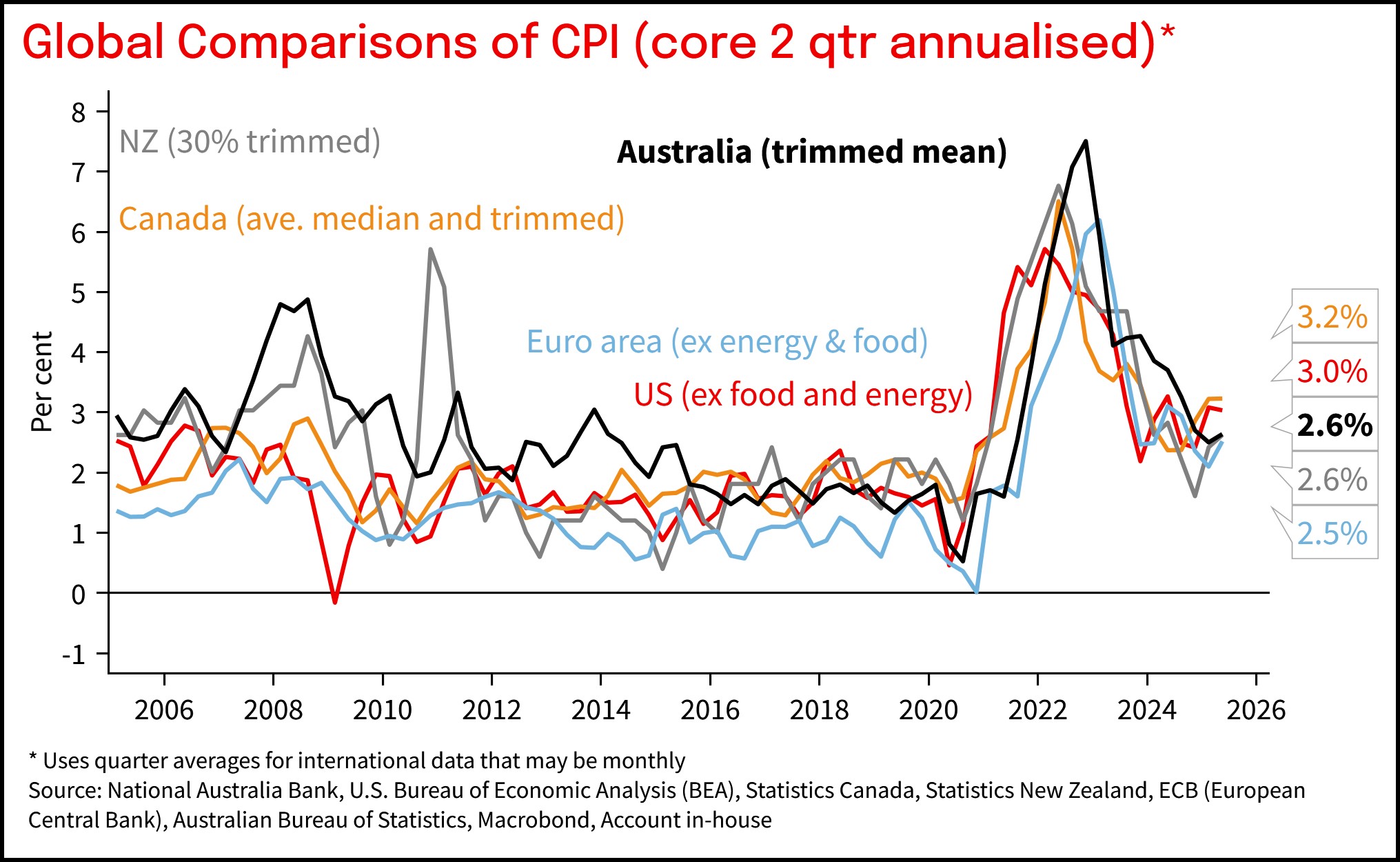

- Australian Q2 CPI gave a green light to an RBA August interest rate cut, though the details suggested some caution should remain

- Also in good news, there was a sharp turn positive in the data flow with Retail Sales, Building Approvals and Credit all beating expectations

- Offshore the US data flow remained strong, Fed Chair Powell sounded less dovish or mildly hawkish, while President Trump finalised tariffs: Australia is confirmed at 10% and New Zealand at 15%

Week ahead

- Australia has a quiet week ahead of the RBA Meeting the following week (11-12 August). The only top-tier piece is the Monthly Household Spending Indicator (Tuesday) which should rise 0.9% m/m (consensus 0.8%)

- Plenty of second-tier data, including the Goods Trade Balance (Thursday). Note it is also a NSW Bank Holiday on Monday, meaning thinner than usual markets on Monday.

- Offshore it is fairly quiet with the Northern Hemisphere Summer Holiday season in full flight. Major items include:

- fallout from US President Trump’s finalisation of tariff rates

- the BoE meets (Thursday) where a 25bp cut is widely expected

- earnings continue, including AMD and Disney

- US has the ISM Services (Tuesday) and Productivity (Thursday). There is a smattering of Fed speakers, but we expect the schedule to fill out further given there are clear divergences on the FOMC.

- Europe is a desert data wise

- In China the S&P Global Services PMI (Tuesday; formally Caixin PMI) where another soft outcome is likely. The Trade Balance (Thursday) is also likely to garner attention.

- Across the ditch, in NZ, are Unemployment/Employment (Wednesday) and Inflation Expectations (Friday)

Read the full report here

Chart 1: Australian core inflation close to the 2-3% mid-point

This document has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, NAB recommends that you consider whether the advice is appropriate for your circumstances. NAB recommends that you obtain and consider the relevant Product Disclosure Statement or other disclosure document, before making any decision about a product including whether to acquire or to continue to hold it. Please Click Here to view our disclaimer and terms of use. Please Click Here to view our NAB Financial Services Guide.

All prices and analysis at 1 August 2025. This information has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.