What to Watch - Week of 9 June

Tapas Strickland & Taylor Nugent | Markets Research

Past Week

- Australian GDP was a soggy 0.2% q/q, weighed by a fall in public demand.

- The data confirmed consumer momentum into 2025 has also been weaker than the RBA earlier expected

- Offshore, the ECB cut as expected but President Lagarde said they were ‘getting to the end of a policy cycle’

- US data flow has been a little softer, but will be overshadowed by Payrolls

- The AUD outperformed against a weaker US dollar, up 1.3% to 0.6501

Week ahead

- Australia has a quiet start with a Monday Public Holiday across all states except for QLD and WA. The NAB Business Survey and the WBC Consumer Sentiment (Tuesday) highlights in what is also a quiet week for data

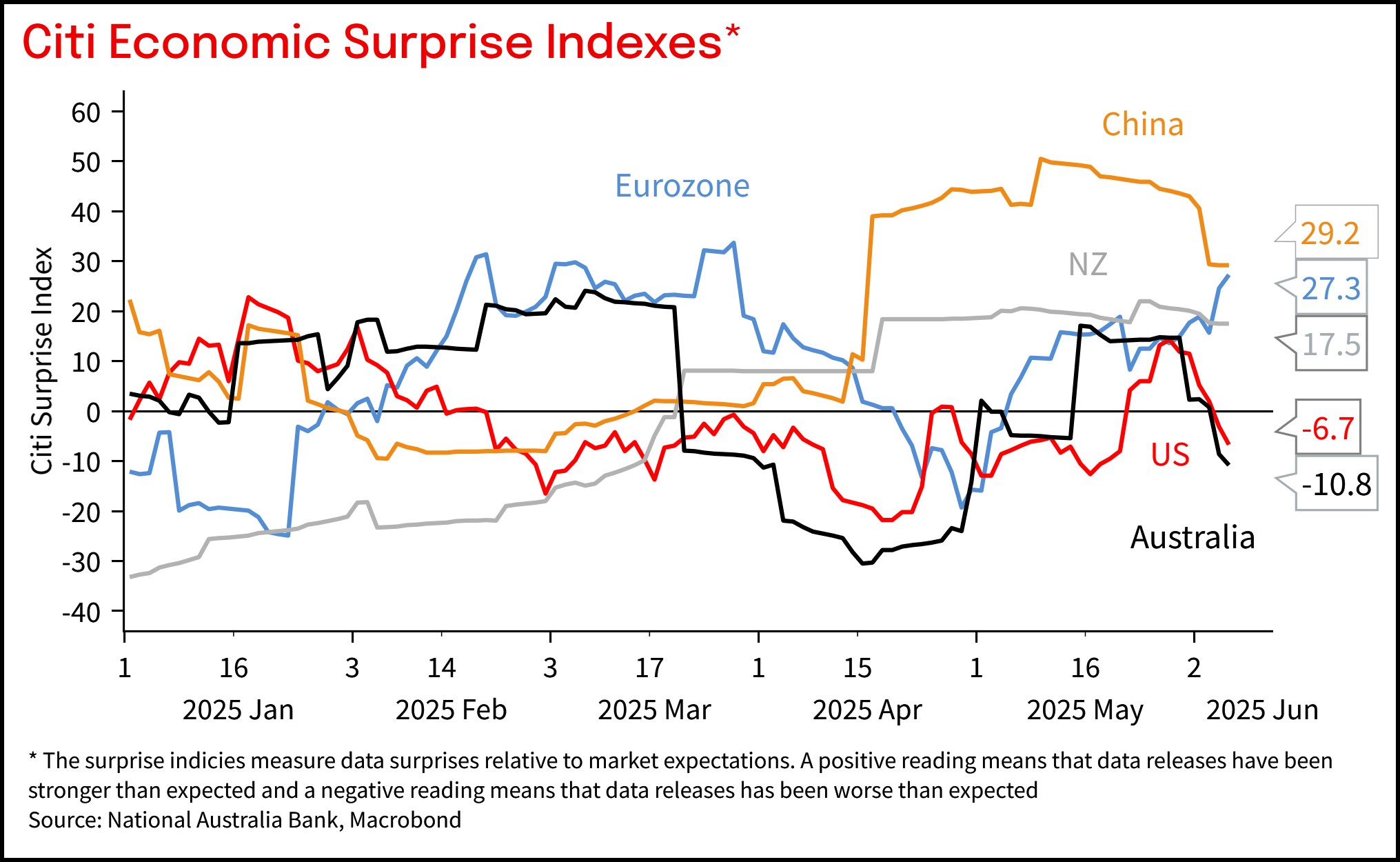

- Across the globe it is a relatively quiet week as well with most focus still on tariff/trade developments given the US’ self-imposed 9 July deadline is nearing. Note US and Australian data has disappointed over the past week

- In the US the CPI (Wednesday) and PPI (Thursday) will be closely watched for tariff impacts. Jobless Claims (Thursday) also worth a look after last week’s rise. Auctions too: $39bn of 10yr and $22yrbn of 30yr

- Across the pond in the Eurozone, it is quiet with no top-tier data apart from the ECB Wage Tracker (Wednesday)

- The UK has some important data flow, including Earnings/Unemployment (Tuesday), Monthly GDP (Thursday) and the Chancellor’s Spending Review (Wednesday)

- In China, the Trade Balance, CPI and PPI (all Monday) will be watched closely for trade impacts

- Japan has little in the way of top-tier data

- There is also little of note on the NZ calendar apart from the pre-GDP partial of Manufacturing Activity (Monday) and the BNZ PMI (Friday)

View the full report here

Chart 1: Data is disappointing expectations in Australia and the US

This document has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, NAB recommends that you consider whether the advice is appropriate for your circumstances. NAB recommends that you obtain and consider the relevant Product Disclosure Statement or other disclosure document, before making any decision about a product including whether to acquire or to continue to hold it. Please Click Here to view our disclaimer and terms of use. Please Click Here to view our NAB Financial Services Guide.

All prices and analysis at 6 June 2025. This information has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.