What to Watch - Week of 30 September 2024

Tapas Strickland | Markets Research

Past week

- A big week in Australia, with the AUD lifting on the back of Chinese stimulus announcements (AUD +1.1% to 0.6881). The iron ore price is also up a smart 11% on the week, as are equities (CSI 300 +14.8% on the week)

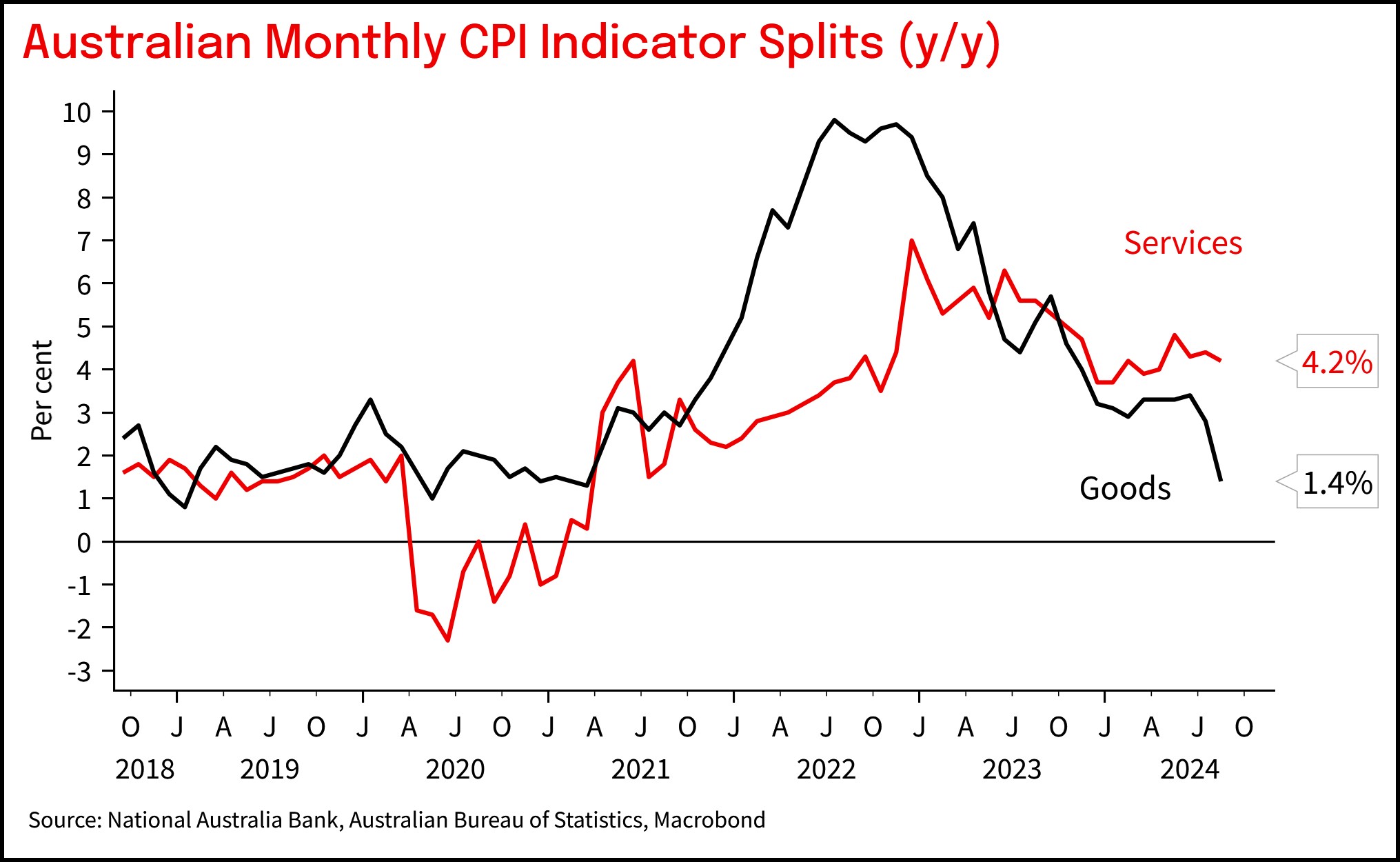

- The RBA met and kept rates on hold, though Governor Bullock did note the board did not discuss the case to hike rates. However, the Monthly CPI Indicator continued to show elevated services inflation.

Week ahead

- In Australia, all focus on the extent to which households have started to spend the extra cash flow generated from recent tax cuts and government subsidies. Retail Sales (Tuesday) and Deposit data (Monday) will be watched closely. A lot of other data out too, including Building Approvals and the Goods Trade Balance.

- Offshore there are three key data points. US Payrolls (Friday), Eurozone CPI (Tuesday), and China PMIs (Monday) ahead of China’s Golden Week Public Holidays that extend through to 7 October.

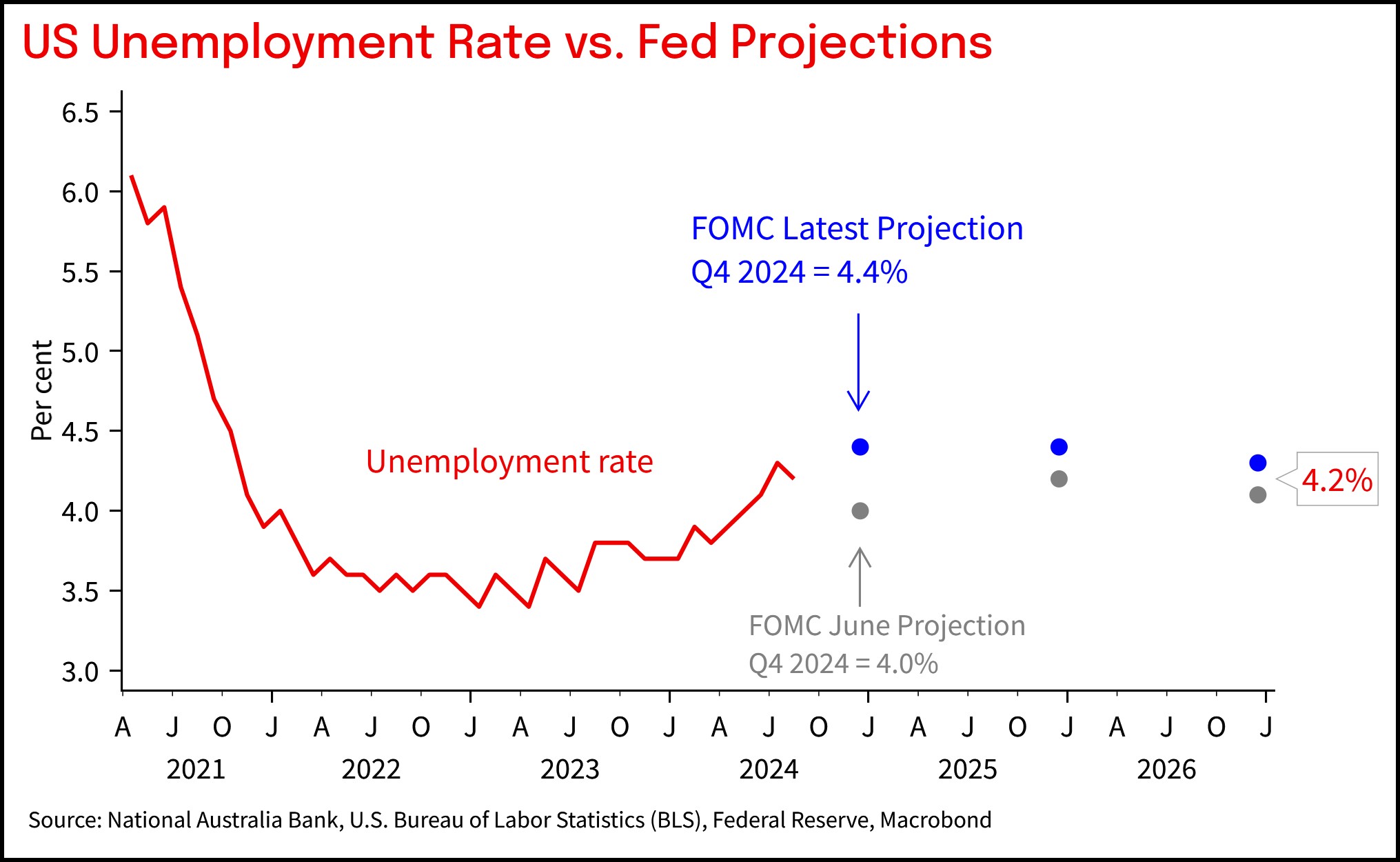

- Consensus for US Payrolls (Friday) sits at 140k jobs and for the unemployment rate to be unchanged at 4.2%. However, there is little between 4.2% and the FOMC’s September Projection of the unemployment rate averaging 4.4% in Q4. Any lift would likely lift the probability of a follow up 50bp cut in November (currently 49% priced for a 50bp move).

- There are also other relevant US labour market indicators out in the week, including JOLTS (Tuesday), ADP Employment (Wednesday), and the employment sub-indexes of the Manufacturing and Services ISMs (Tuesday and Thursday). Overall, Services ISM is expected to remain expansionary.

- In the EZ CPI will dominate and where to date services inflation appears sticky, as it is in the UK and in Australia. There is little data of note in the UK, though BoE’s Chief Economist Pill is speaking on Tuesday. In Japan the Tankan is out as is the BoJ Minutes, though more focus on the policies of the new PM and whether they intend on going to fresh elections.

- Finally in NZ is the QSBO (Tuesday) and Employment Indicators (Friday)

View the full report here

Chart 1 - Past Week: Australian services inflation remains elevated

Chart 2 - Week ahead: US Payrolls under focus, not much gap between the unemployment rate and the FOMC projection

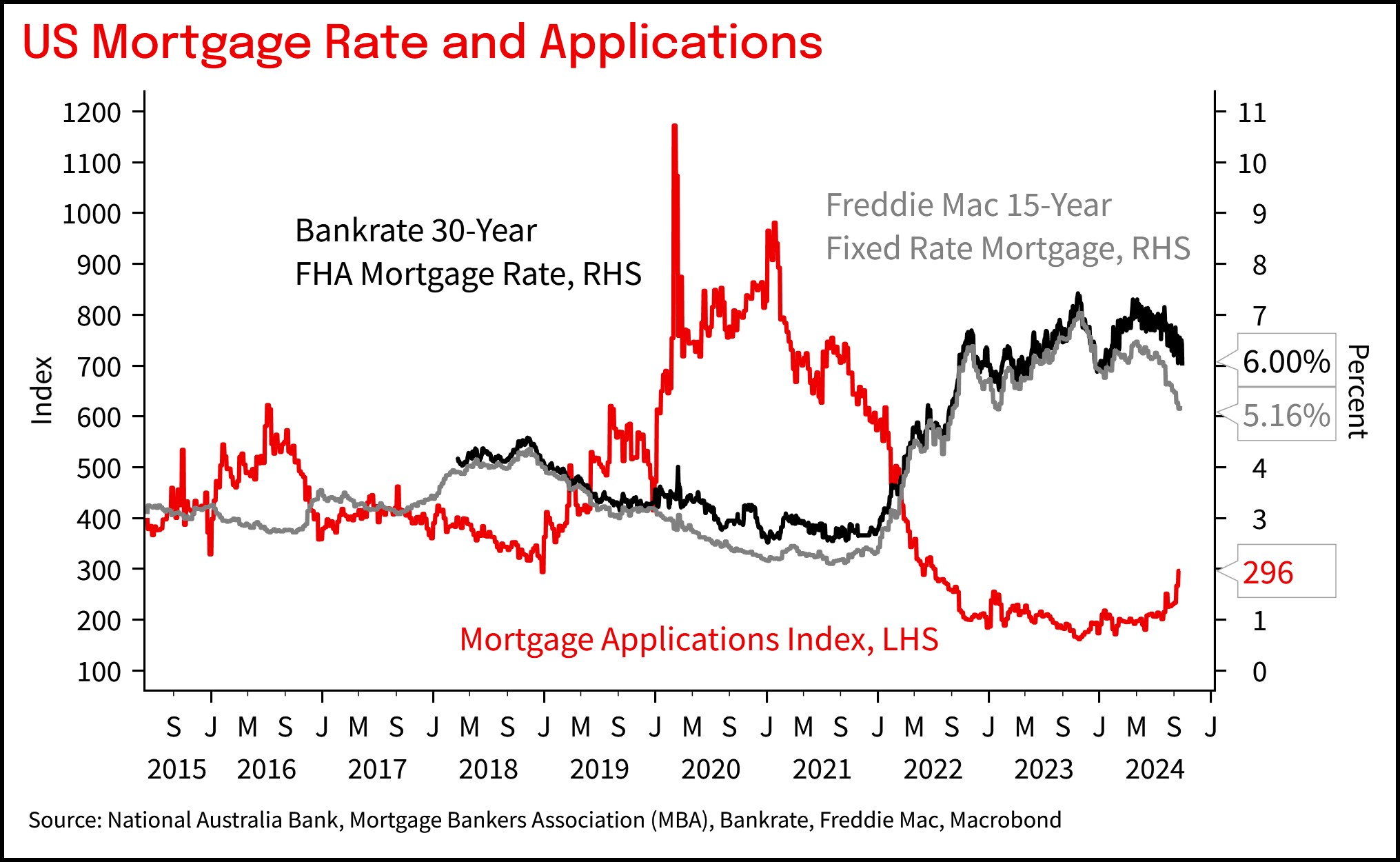

Chart 3 - Week ahead: How will the US housing market react to lower mortgage rates? |

This document has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, NAB recommends that you consider whether the advice is appropriate for your circumstances. NAB recommends that you obtain and consider the relevant Product Disclosure Statement or other disclosure document, before making any decision about a product including whether to acquire or to continue to hold it. Please Click Here to view our disclaimer and terms of use. Please Click Here to view our NAB Financial Services Guide.

All prices and analysis at 27 September 2024. This information has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.