Q2 CPI Preview – Trimmed mean at 1.0% a test of RBA strategy

Taylor Nugent | Markets Research

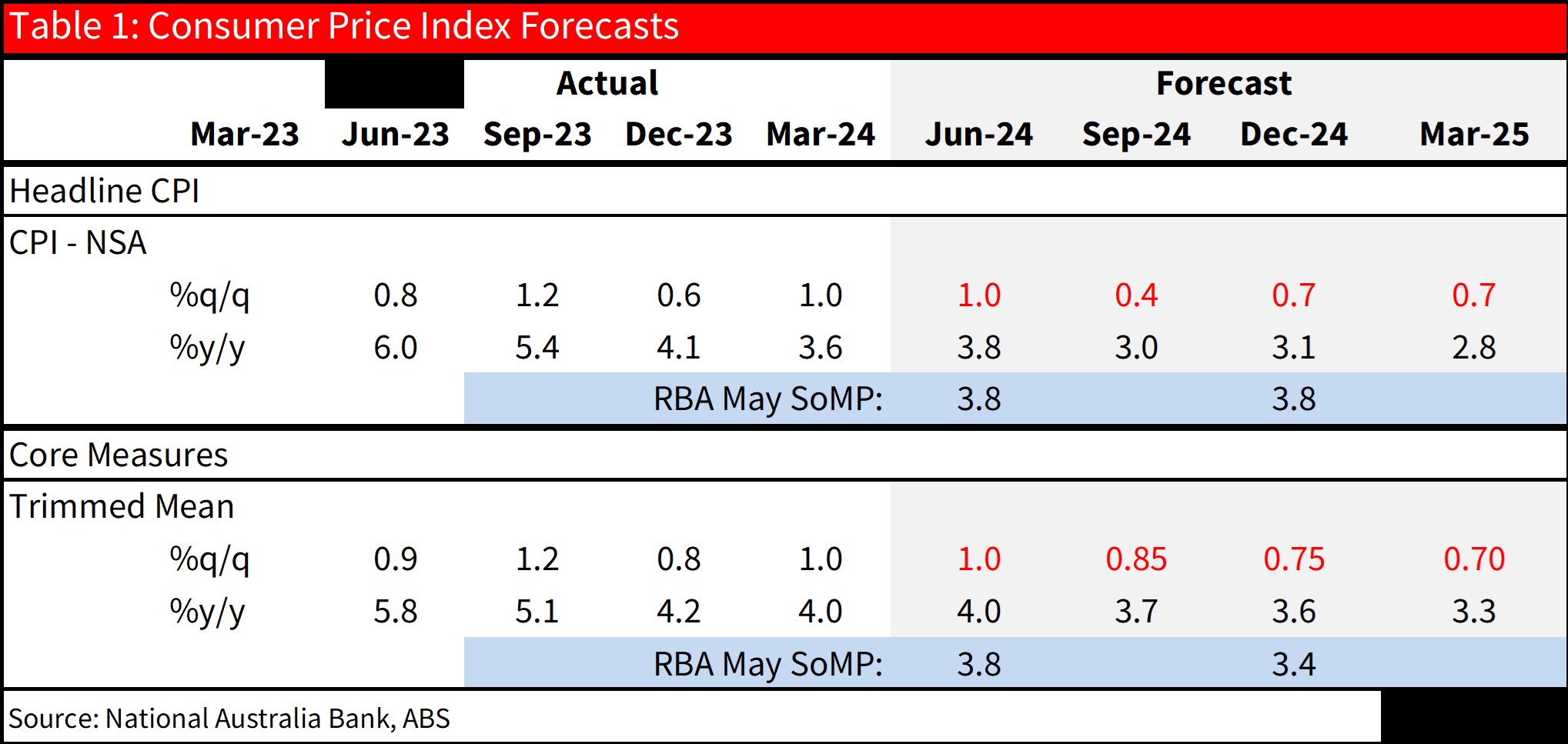

We expect Q2 trimmed mean of 1.0% q/q and 4.0% y/y. That’s two tenths above the RBA’s May SoMP forecast of 0.8% and a tenth above our 0.9% preliminary expectation ahead of the May CPI indicator.

We also pencil in a headline outcome of 1.0% q/q nsa (1.1% sa). That would see headline lift to 3.8% y/y. A surge in international travel prices is the key driver.

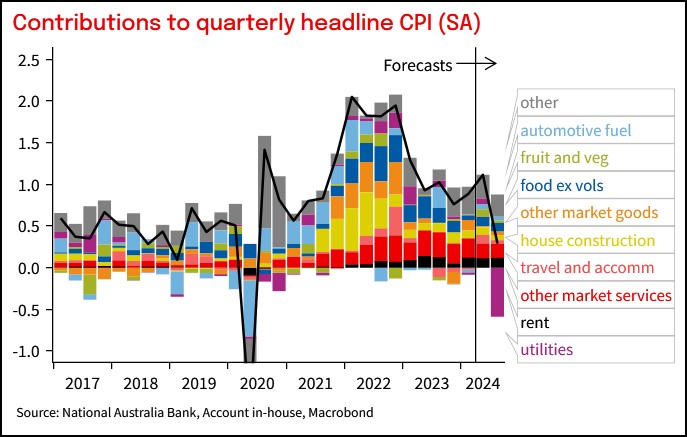

Relative to last quarter, durable goods are more benign but still running ahead of the trend declines prior to the pandemic. A reacceleration in grocery inflation is a key support for the trimmed mean. Housing components remains persistently strong, but elsewhere market services show some improvement.

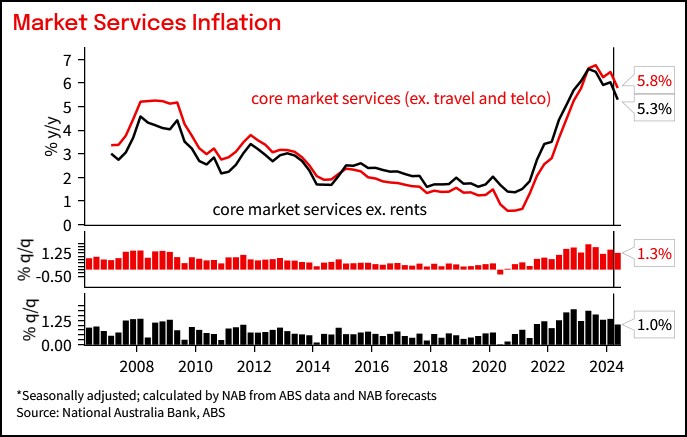

The aggregates matter, but this isn’t a simple ‘sticky service prices’ story. A silver lining is that the strength we expect to be confirmed in Q2 CPI is despite progress in still too high market services and non-tradable inflation.

Uncertainty remains despite the information in the Monthly indicators. New cars, much of health, and financial services have had no coverage so far. Over the past 2 years, trimmed mean has printed on average a tenth away from our forecast and two tenths away from the Bloomberg median, and with little directional bias. With the RBA’s strategy having left risks thoroughly unbalanced, Q2 CPI is particularly important.

NAB’s central view is that the RBA will remain on hold – some cooling in market services inflation, wages growth likely passed its peak, and soft activity growth should be enough to keep the low bar of a return to target in 2026 in sight. The consequence is they won’t be able to cut for a long time. We pencil in May 2025.

Still, further tightening as soon as August is a real possibility should the RBA reassess and conclude rates are insufficiently restrictive. At numerous points through this tightening cycle the RBA has slowed or paused hikes earlier than has been warranted by the data backdrop, opting to tolerate upside risks and higher for longer inflation in pursuit of maintaining labour market gains. Their confidence in that approach is frayed.

View the full report here

This document has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, NAB recommends that you consider whether the advice is appropriate for your circumstances. NAB recommends that you obtain and consider the relevant Product Disclosure Statement or other disclosure document, before making any decision about a product including whether to acquire or to continue to hold it. Please Click Here to view our disclaimer and terms of use. Please Click Here to view our NAB Financial Services Guide.

All prices and analysis at 4 July 2024. This information has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.