Mid-year outlook for 2024: Opportunity knocks

Henry McVey | KKR

Despite intensifying political uncertainty, heightened geopolitical tensions, and volatile commodity prices, we continue to see compelling investment opportunities across the global macro landscape. Accelerating AI demand for electricity, reorientation of global supply chains, improving labor productivity, and retirement security all represent important macro themes behind which to invest.

We also remain really encouraged by the technical backdrop, as net issuance of Equities and Credit remains well below trend. However, it is definitely not business as usual in the world of macro and asset allocation, as our Regime Change thesis requires a different approach to portfolio management.

To build upon this view, we have done more analysis to underscore the value of adding more non-traditional assets to one’s portfolio. Indeed, unlike in the past, today’s volatility in portfolios is being driven by stock-bond correlation, not by single asset volatility. Importantly, most of today’s CIOs have not invested in this type of environment.

In terms of areas to lean in, we think that the current vintage will be a strong one for Private Equity, especially opportunities linked to value creation by operational improvement and/or corporate carve-outs.

Meanwhile, we continue to pound the table on many parts of Real Assets, including Real Estate Credit, Infrastructure, and Asset-Based Finance.

Finally, we see a lot of potential in Opportunistic Credit and Capital Solutions.

On the risk side, we believe higher rates – especially if productivity should tail off – are a more challenging scenario than lower rates and slower earnings. We are also keeping an eye on employment trends.

Our bottom line: Opportunity Knocks, as we still think the current economic cycle has further to run, a backdrop that should accrue to the benefit of long-term investors, especially ones who have dry powder to lean into the inevitable periodic dislocations that are likely to occur during a Regime Change.

"A pessimist complains about the noise when opportunity knocks." (Oscar Wilde - Irish poet and playwright)

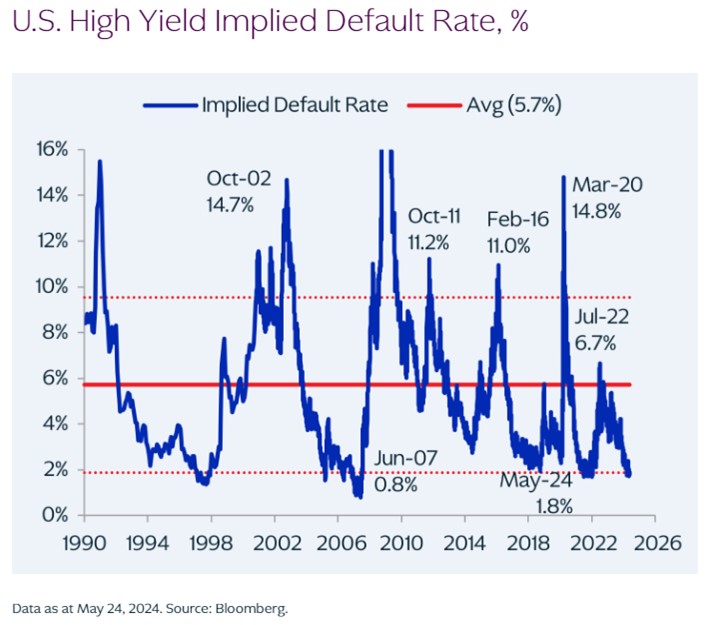

We are often asked, especially heading into the second half of 2024, if we still believe that the glass is half full for global allocators when it comes to deployment opportunities, particularly in an environment of heightened complexity, ‘sticky’ inflation, and higher for longer interest rates. (See Glass Half Full Outlook for 2024). With an uncertain presidential election around the corner in the United States, and many other important elections taking place across the world, there is certainly a lot to consider. On the more cautious side, equity markets are now nicely higher, and credit spreads are now sharply tighter since late December 2023 when we laid out our thesis that investors might regret looking at the glass as half empty. In fact, our KKR proprietary market-implied default model suggests HY spreads are pricing in about a two percent default rate today, compared with about three percent at the beginning of the year and a historical average of 5.7%.

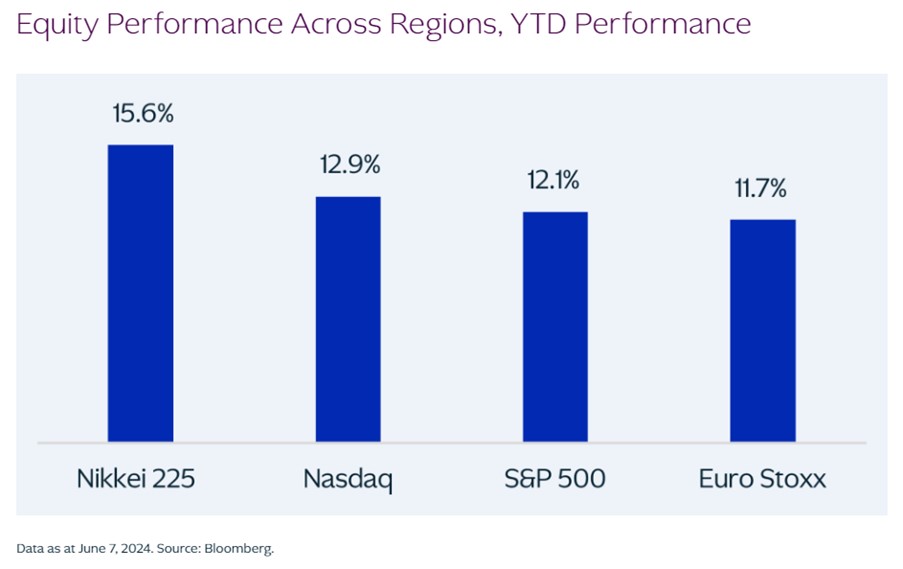

EXHIBIT 1: Equity Markets Have Withstood Substantial Volatility to Enjoy Glass Half Full Returns and Then Some in the 1H24

EXHIBIT 2: …While Investors Have Also Gotten More Optimistic About the Outlook for Credit, High Yield in Particular

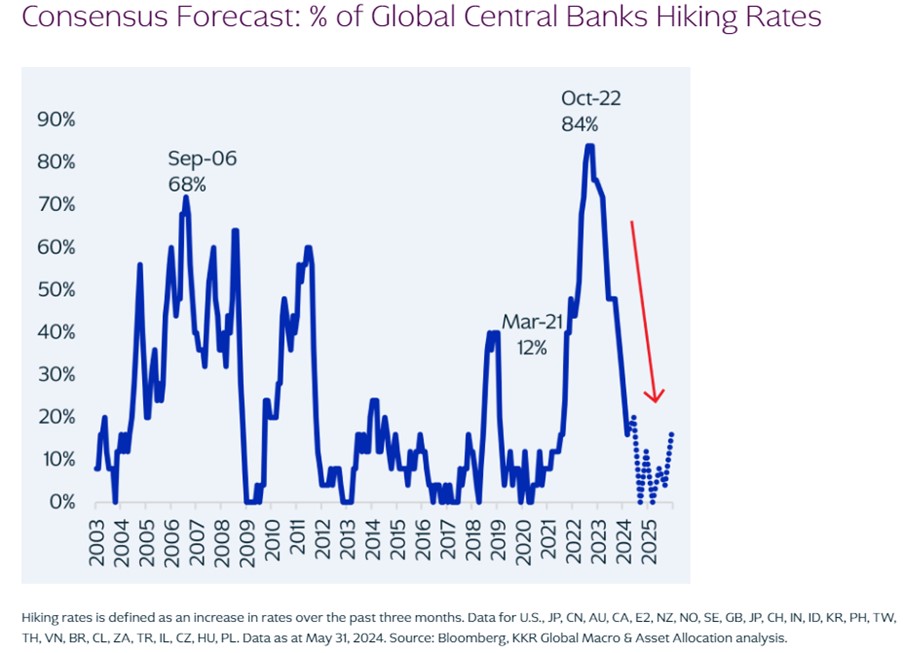

EXHIBIT 3: Risk Assets Have Responded Favorably to the Idea That There Will Be Fewer Tightenings and More Easings

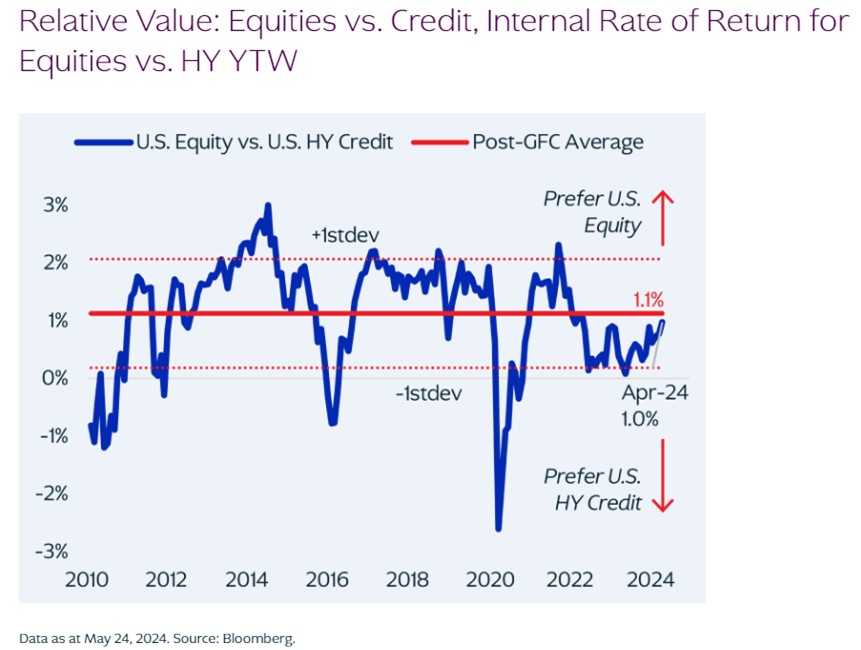

EXHIBIT 4: Overall, Our Models Still Favor Credit, But Now Only at the Margin

However, perhaps more important for long-term investors, there are a lot of political and social crosscurrents that are increasingly bleeding their way into markets. Not surprisingly, the introduction of social media into our political process has created more discord. This type of disruption is like other post-industrial revolutions where technological change ushered in periods of social and political unrest. As our colleague Ken Mehlman explains, just as the invention of the printing press around 1440 introduced years of political, religious, social, and scientific disruption, the combination of the Internet and social media is a ‘Gutenberg 2’ moment that has produced and portends similar disturbances.

At the same time, complicated issues around immigration and inequality are also driving tense debates across the Western world that increasingly seem to push the left and right further apart. See Section IV, question #3 for a full discussion, but the upcoming U.S. presidential election only increases our conviction that policy from either a Trump or a Biden administration is likely to maintain an inflationary bent (which further heightens discord), given the threat of tariffs and the need for security spending, contributing to an increasing ‘normalization’ of wider than usual deficits. Finally, great power rivalries around the globe have intensified notably in recent quarters. As such, investors should expect more barriers to trade and capital flows in the coming years under almost all scenarios. Key to our collective thinking is that the intensifying focus on ‘homeland economics’ is a post-COVID, post-Ukraine global phenomenon that is likely to continue almost regardless of electoral outcomes in most countries.

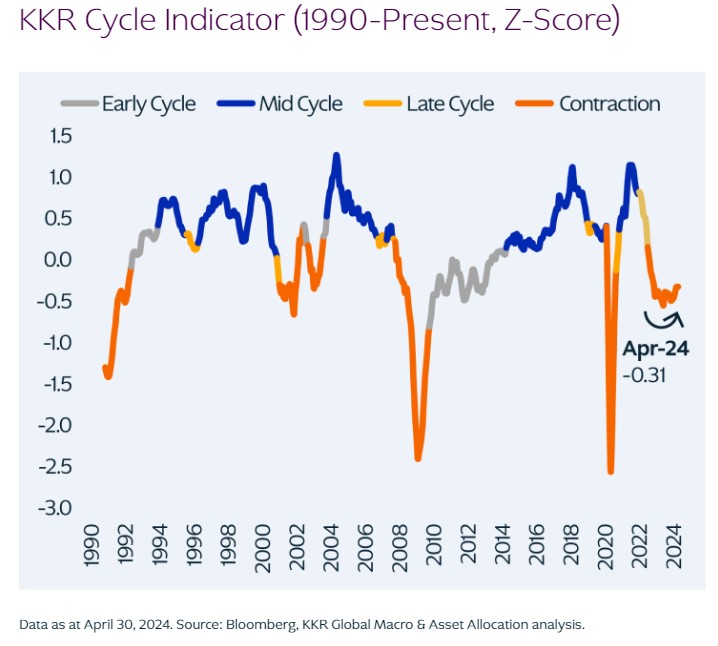

EXHIBIT 5: After Two Years of Being in Late Cycle and Contraction, Our Proprietary KKR Cycle Indicator Is About to Move Into Its Early Cycle Phase

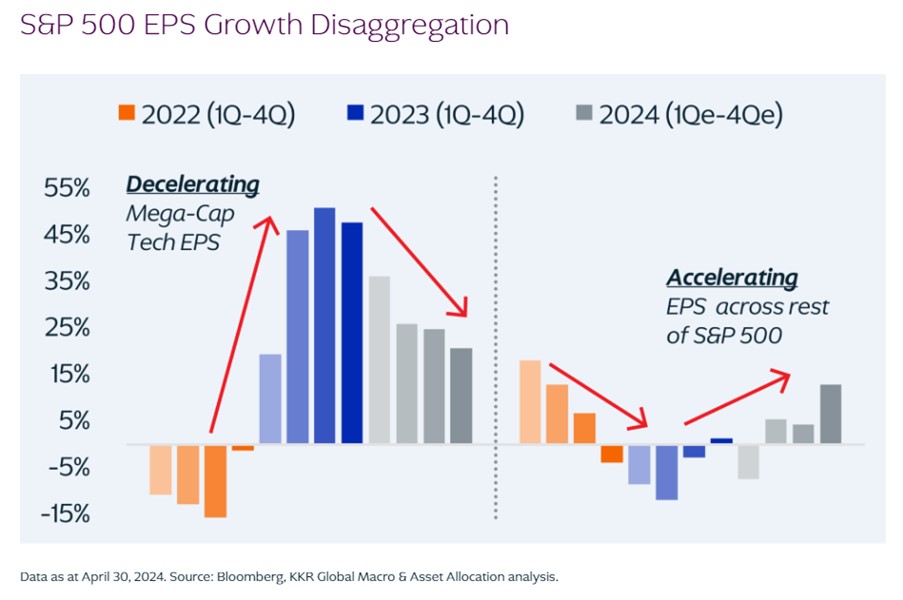

EXHIBIT 6: We Think Earnings Growth Is Set to Broaden Beyond Mega Cap Technology and Become More Balanced in Coming Quarters, Driven by Positive Operating Leverage and Margin Growth in Other Sectors

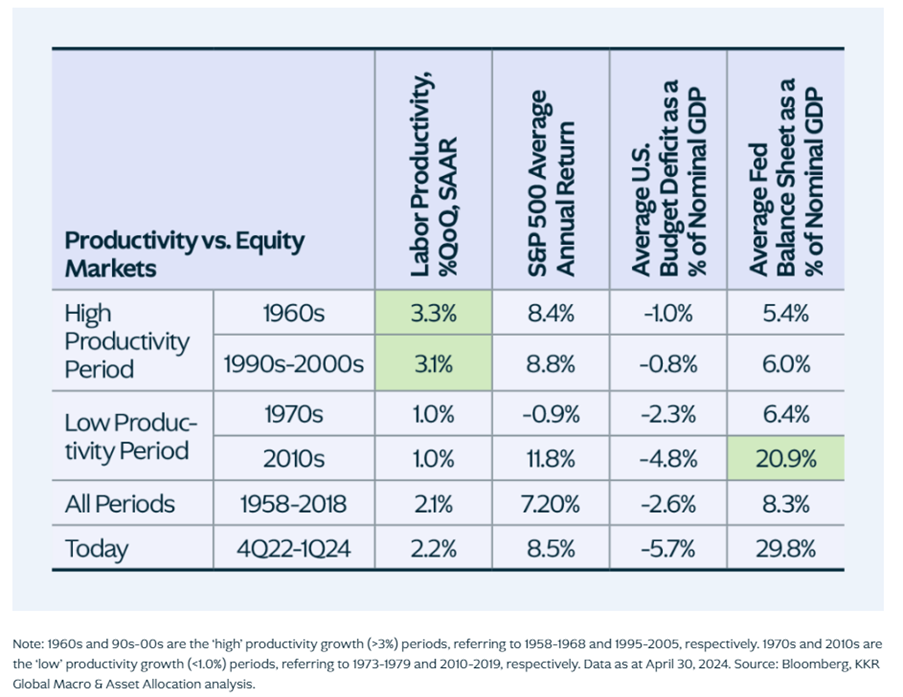

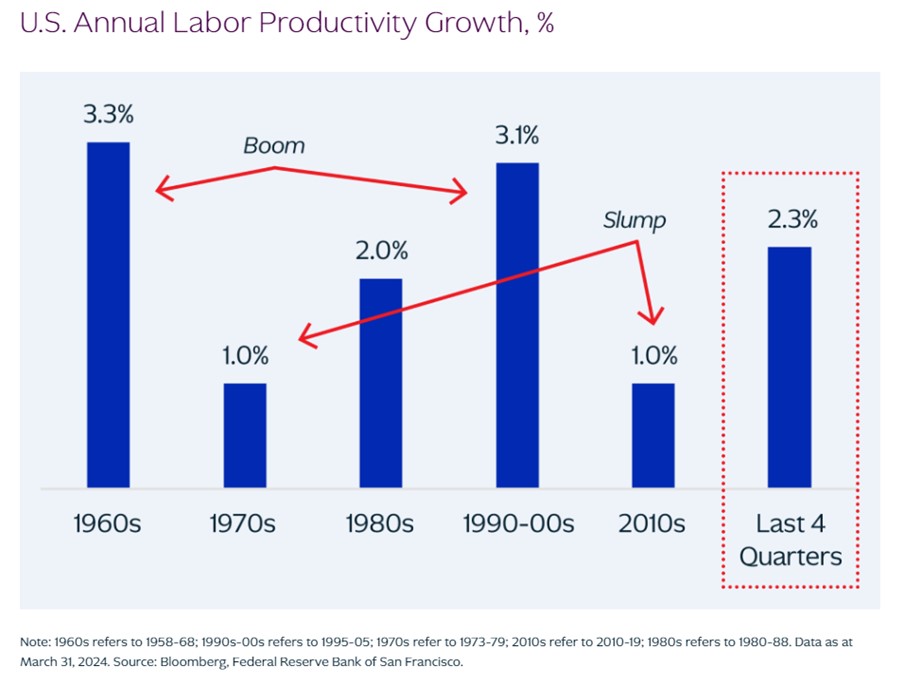

EXHIBIT 7: Long Periods of Equity Outperformance Have Been Driven by Productivity and/or Central Bank Intervention…

EXHIBIT 8: ...As We Look Forward, Our Thesis Is That Productivity Is Again Set to Reaccelerate, Which Would Be Quite Positive for Capital Markets

On the positive side of the ledger, growth and earnings – as our models have been suggesting for some time – are all performing better than the consensus expected in a higher nominal GDP growth environment. True, the U.S. consumer is not driving massive demand growth the way he or she was post-COVID, but unemployment has stayed low (Exhibit 10), inventories are in check, and housing activity is stabilizing. Also, we have seen a massive capex cycle being led by the Technology sector (Exhibit 9). Our view is that, similar to the Internet boom in the 1990s (and the corresponding period of solid economic growth leading up to 2000), the AI boom will drive a sustained period of higher capex before it is actually reflected in corporate profitability results. Implicit in what we are saying, though, is that the recent ongoing surge in productivity has actually occurred before AI benefits have been realized at scale, further underscoring our view that the corporate sector could enjoy a longer-tailed profitability renaissance. Importantly, though, unlike the dot-com bubble 20+ years ago, the companies financing this spending this cycle have bullet proof balance sheets, lower costs of capital, and a more consolidated market.

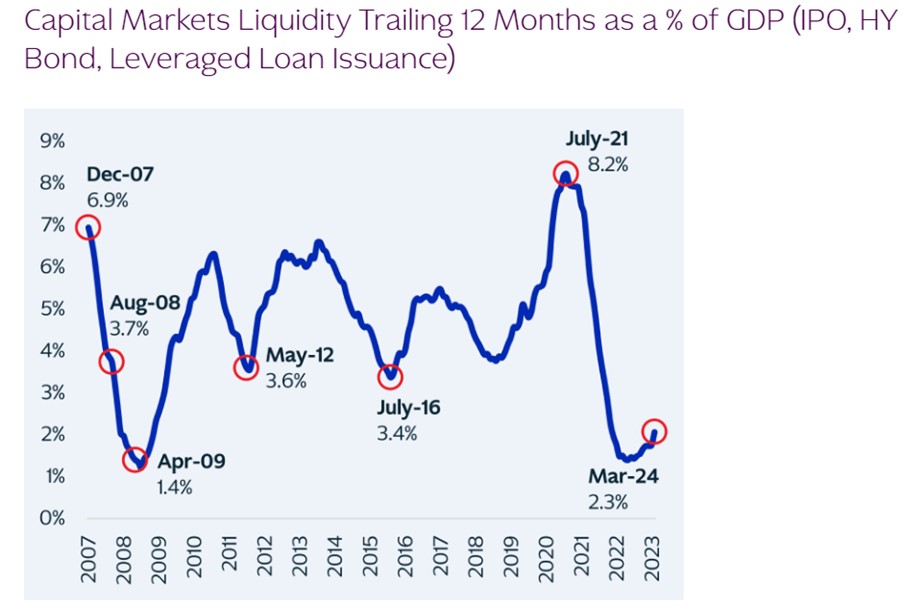

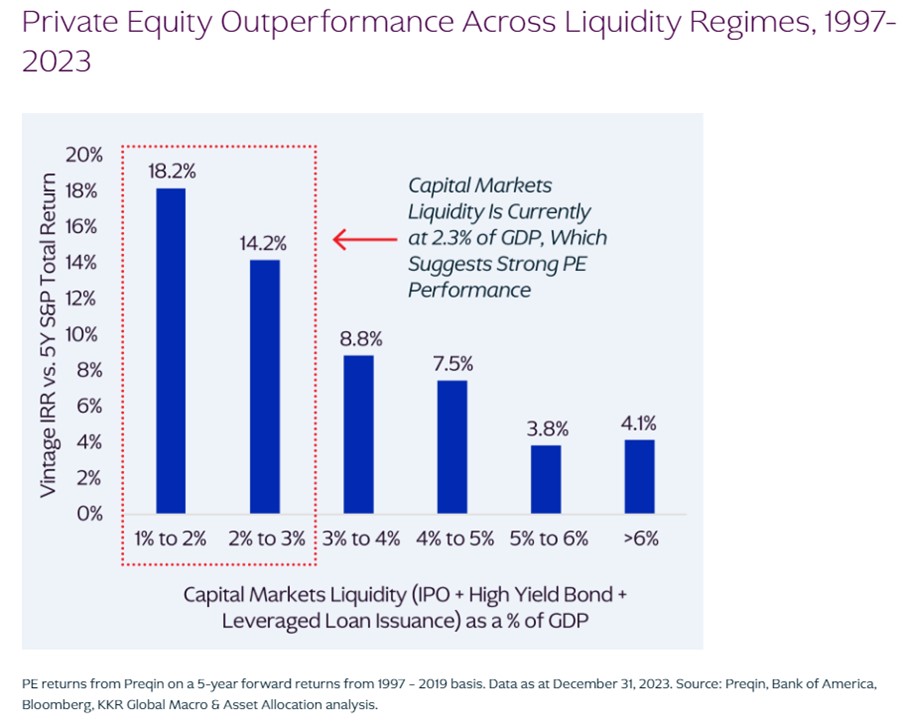

As we look ahead, we also want to signal another positive: Corporate earnings growth is beginning to broaden beyond just the Technology sector. One can see this in Exhibit 6. We think this increased breadth should create a more balanced tone within the liquid Equity markets. In addition, the technical picture remains quite compelling, with a lack of both net equity and corporate debt issuance (Exhibit 11), which generally bodes well for returns (Exhibit 12), especially in Private Equity.

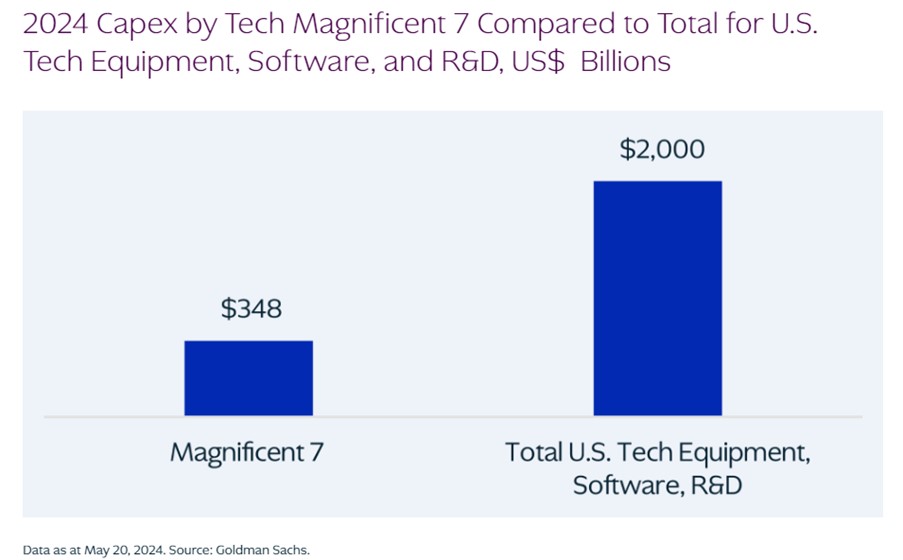

EXHIBIT 9: The Magnificent 7 Reinvests 61% of Their Operating Free Cash Flow Back Into Capex and R&D. They Now Also Account for Almost 20% of Total Capex

EXHIBIT 10: We Think the Jobs Environment Is Much More Akin to the 1990s Than Post-GFC

At the same time, we think that many investors are still actually underweight their target allocations, including holding too much Cash at a time when most central banks have finished raising rates (Exhibit 3). Our proprietary survey work within the Family Office (see Loud and Clear) and Insurance (see No Turning Back) segments supports this view, while money market/cash balances in the individual investor market are also quite high relative to trend.

EXHIBIT 11: Our Liquidity Indicator Is Still Recovering From Near-Trough Levels

EXHIBIT 12: Private Equity Tends to Outperform Public Markets in Low Liquidity Environments

Against this unique macroeconomic backdrop, however, we continue to argue that as investors we are experiencing a Regime Change. There remain four pillars to our original thesis: ongoing fiscal stimulus, heightened geopolitics, a messy energy transition, and stickier wages (driven largely by a shortage of skilled workers). If we are right, then global allocators and macro investors need to view their portfolios through a different lens. In particular, we think that more diversification across asset classes as well as less dependence on global sovereign bonds is warranted, especially given correlations between stocks and bonds have turned decidedly positive (Exhibit 14).

EXHIBIT 13: While Inflation Should Continue to Cool, We Don’t Think It Will Return to Previous Levels. As a Result, We Maintain Our Regime Change Thesis

So, where do we land as we look ahead to the second half of the year and into 2025 and beyond? Download the full outlook here.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 24 June 2024. This document was originally published in Livewire Markets on 24 June 2024. This information has been prepared by KKR Australia Investment Management Pty Ltd (ABN 42 146 164 454, AFSL 420085). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.