Spotify, Factor ETFs and the evolution of investment

Andrew Ang, PhD | Managing Director, Head of Factors, Sustainable and Solutions

I went to high school in Perth during the 1980s and I really loved buying music. The first LP I bought was Kylie Minogue’s album, ‘Kylie’. As much as I liked Kylie Minogue, I preferred ‘I Should Be So Lucky’ and I didn’t really like ‘The Locomotion’ that much - but in those days you had to buy the whole album.

What’s happening today with finance is exactly the same as music – today you don’t have to buy the whole thing. With streaming services like Apple Music and Spotify, you can listen to precisely the songs and tracks that you want, in the format that you want, when you want. In asset management, we used to have to buy the whole album - one manager that gave us a collection of index or market exposures. We also had that asset manager give us tilts towards style factors like value, quality, momentum, low size or low volatility. That alpha manager also gave us returns in excess of those style factors and market exposures - but you had to buy the whole album to get them. Today, you can buy the parts you want, that are appropriate for your investment goals, in a format that is suitable for you.

The five factors - value, quality, low volatility, small size and momentum - are not new. They were first referenced by Columbia accounting professors Graham and Dodd in their book Securities Analysis in 1934, which became a bible for the investment management industry. They advocated using a systematic approach through analysis of financial statements, balance sheets and earnings statements to come up with a stock valuation – effectively the big data of the 1930s. Their analysis showed that these five factors were the key drivers of equity market returns over the long term.

What is new is the ability to put these factors into different formats, to harvest these in different ways – to put the power of buying cheap, or buying into trends, or buying quality stocks, into ETFs, tailored portfolios or managed accounts that can be used by all sorts of investors. What is new is the ways we can access these long-term drivers of return.

Create your personalised playlist using factors

How can we use these factors? They’re highly complementary to existing passive and active investment strategies.

There’s actually nothing wrong with broad market exposure, or being average. I wish I were average, but unfortunately I’m only 163 centimetres tall on a good day. But sometimes being average is not good enough – you might want to seek higher expected returns or greater robustness and resilience in your portfolio. Factors can really help with that.

We can also use factor strategies as a complement to active investment strategies. Sometimes you may build a portfolio of actively managed funds, or individual stocks, that doesn’t have all the factors, so we can add factors that are diversified. In some cases, we might be able to replace expensive, underperforming active managers.

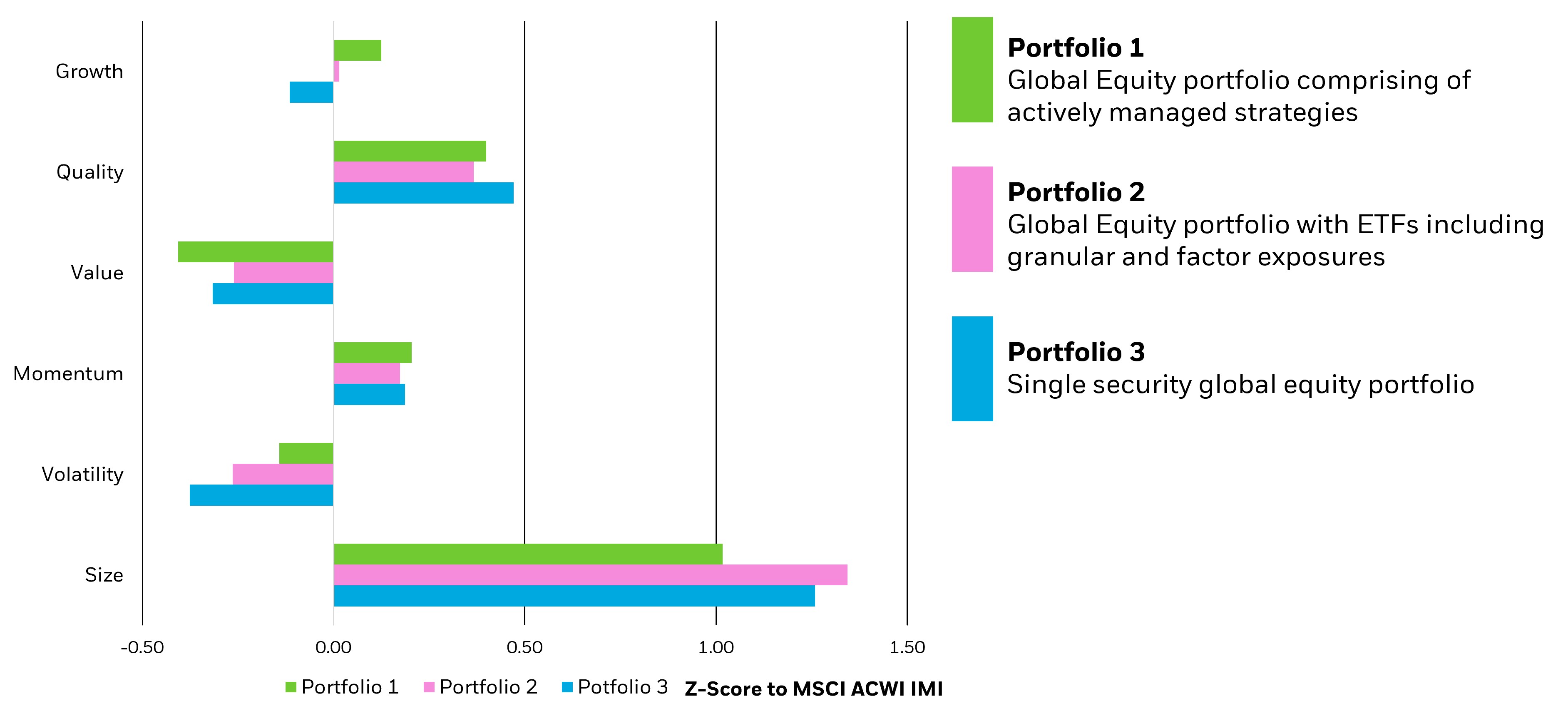

Let’s look at this example using some common types of Aussie investor portfolios. The first portfolio is using actively managed funds, the second one uses ETFs and the third one uses single securities. Let’s focus on the first two.

Source: BlackRock, 31/12/2023

Source: BlackRock, 31/12/2023

One of the interesting things to note is that Aussie investors tend to have a pronounced large cap tilt in their portfolios. What we can do is add single factor ETFs to round these out and better diversify your exposure.

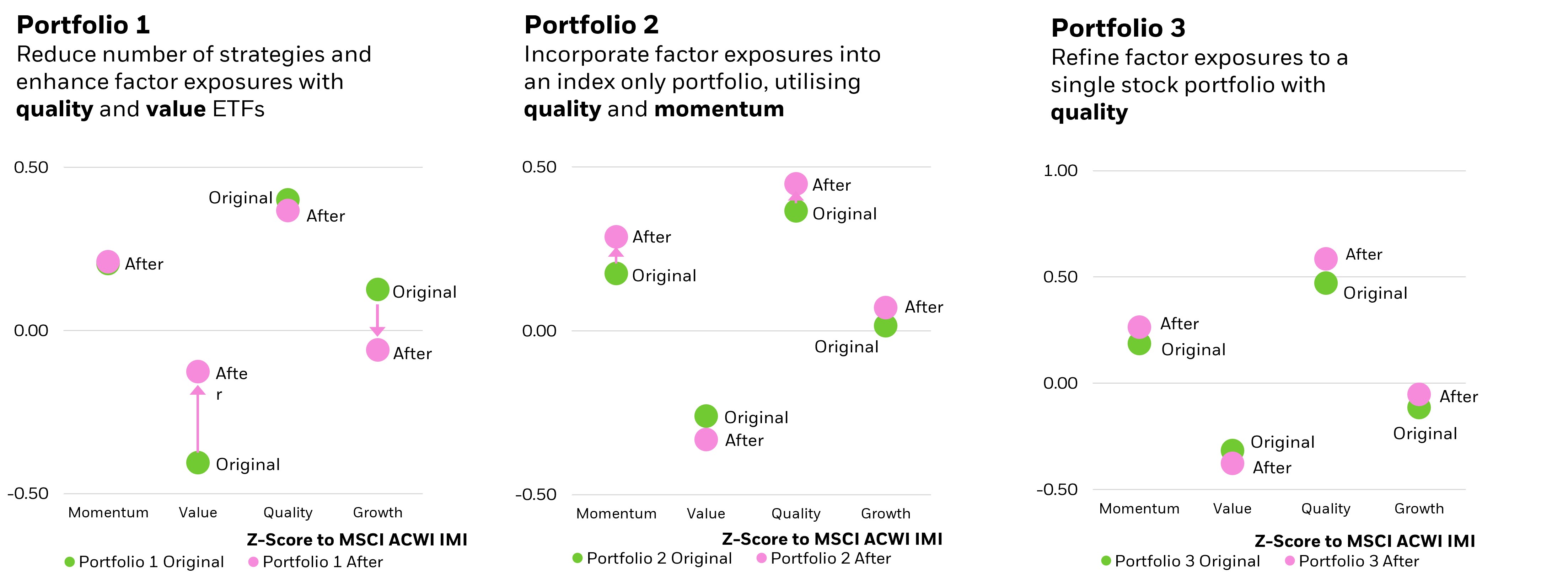

For the portfolio that uses active funds, you can see there’s a big rise in the value exposures for this portfolio, and a bit of an extra increase in quality, when we add quality and value ETFs. For the second set of portfolios using global equities ETFs, we add quality and momentum ETFs for a significant increase in this investor’s exposure to the momentum factor, as you see in the first column.

Source: BlackRock, 31/12/2023

Source: BlackRock, 31/12/2023

When we look at the individual security portfolio, we could get the best bang for our buck here by adding a quality ETF to the portfolio - as often exposure to the quality factor is often not the sole objective of active fund managers. Factor ETFs can help us with more cost-efficient exposures to key return drivers like quality, momentum and value, replacing the need to hold individual securities or pay additional costs for an actively managed portfolio.

It’s easy to use single factor ETFs to round out your portfolio. You can think of it as the playlist of finance – we take each of these different components and serve them up in the way you want, when you want.

The future of factors

One question you might have is if we’ve known about factors since the 1930s with Graham and Dodd, why have these factors persisted? Why are they relevant today and will they be there in the next 100 years? All of these factors are based on economic rationales. There are tens of thousands of academic papers documenting factor premiums. There are six Nobel prizes awarded in the area of factor investing. This gives us confidence that while we’ve observed them for decades, if these economic rationales persist as I think they will, they will be around for the next century as well.

A 2020 study published in one of the top financial journals, the Review of Financial Studies, looked at 30,000 stocks across 60 years of data and 94 different characteristics. They used machine learning to extract out all the performance commonalities, and they found that they were:

- Recent price trends, or momentum;

- Liquidity variables, like small size;

- Risk measures, such as volatility;

- More traditional value and fundamental (quality) signals

These factors are exactly the same as those discovered by Graham and Dodd in the 1930s, so in one sense nothing has changed. What has changed is the way we access these long-term, intuitive drivers of return.

About the Author

Adapted from Andrew Ang's, BlackRock's Head of Factors, Sustainable and Solutions presentation at the 2024 Wealth Symposium powered by BlackRock and iShares.

Andrew Ang, PhD, is a Managing Director within BlackRock’s Systematic investment team. Dr. Ang is Head of Factors, Sustainable and Solutions for BlackRock Systematic. He also serves as Senior Advisor to BlackRock Retirement Solutions. As part of BlackRock Systematic, the Factors, Sustainable and Solutions team, Dr. Ang is responsible for proprietary factor investing, delivering cutting-edge sustainable alpha, ESG outcomes and product innovation.

Dr. Ang is a well-known financial economist specializing in quantitative investing. Author of over 100 publications, Dr. Ang has published on equities, fixed income, optimal asset allocation, and alternative assets. He has written seminal papers in the area of factor investing, including research behind the minimum volatility factor, incorporating macro factors into bond pricing models and factor allocation. His book, "Asset Management: A Systematic Approach to Factor Investing" is a comprehensive guide showing how factor risk premiums can be harvested in portfolio design and incorporated in all aspects of investment management.

Dr. Ang has won many industry prizes and grants, including the Bernstein Fabozzi/Jacobs Levy award, and awards and grants from Q Group, INQUIRE, Netspar, and the National Science Foundation. According to RePEc/IDEAS, the largest bibliographic database in the field of economics, Dr. Ang is rated in the top 0.1% of world-wide economists by citations, downloads, and views.

Before joining BlackRock, Dr. Ang was the Ann F. Kaplan Professor of Business at Columbia Business School. He was previously Chair of the Finance and Economics Division and a Faculty Research Fellow of the National Bureau of Economic Research. As a professor, Dr. Ang worked with several large institutional managers as an advisor. His work with industry was recognized by aiCIO naming him one of the top 10 most influential academics in the institutional investing world.

Dr. Ang earned a BEc(Hons) from Macquarie University, and a PhD in finance and MS in statistics from Stanford University. Dr. Ang used to be a Fellow of the Institute of Actuaries of Australia.

DISCLAIMER

This information has been provided by BIMAL for WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.

BlackRock Investment Management (Australia) Limited ABN 13 006 165 975, AFSL 230 523 (BIMAL).

Information provided on this site in respect of BIMAL products comprises general information only, and does not take into account your individual objectives, financial situation, needs or circumstances. Before making any investment decision, you should assess whether the material is appropriate for you and obtain financial advice tailored to you having regard to your individual objectives, financial situation, needs and circumstances. Refer to BIMAL’s Financial Services Guide on its website for more information. This material is not a financial product recommendation or an offer or solicitation with respect to the purchase or sale of any financial product in any jurisdiction.

No part of BIMAL’s material may be reproduced or distributed in any manner without the prior written permission of BIMAL.

© 2024 BlackRock, Inc. All Rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, iSHARES and the stylised i logo are registered and unregistered trademarks of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.