Higher US inflation derails Fed rate cut plans

Kieran Davies | Coolabah Capital

The US core CPI rose strongly for the third month in a row, pointing to the Fed delaying rate cuts - and possibly not cutting rates at all this year if inflation stays high - where high-for-longer interest rates should pressure risky asset classes that were hoping for interest rate relief.

As CCI's Chris Joye recently warned, the March CPI was likely to be a pivotal event for financial markets given many investors seemed to be underestimating the risk posed by sticky services inflation to the pricing of rate cuts this year, as well as to overly-optimistic risky assets.

As it turned out, another high core inflation print has triggered a substantial reassessment of market views on US interest rates staying high for longer.

That is, the numbers show core inflation picking up sharply over the past few months, more than reversing the run of low numbers seen late last year, which has led the market to rein in its earlier unrealistic expectation that the Fed would quickly and aggressively cut rates.

At the height of the market's optimism in January, the futures curve was pricing in about 175bp of rate cuts in the US this year starting in March.

At that time, CCI thought that market pricing was unrealistic given how falling goods prices were masking sticky services inflation, which in turn reflected a still-tight labour market.

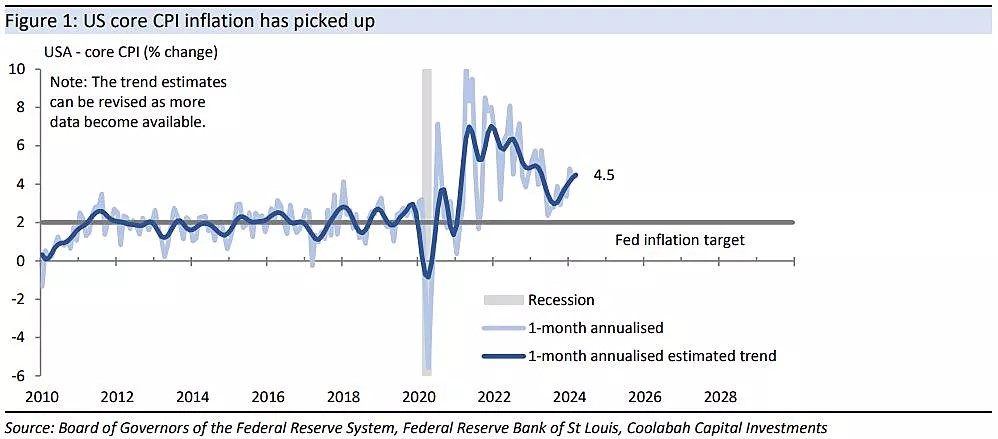

With the core CPI rising by 0.4% for the third month in a row, CCI's estimate of the trend in annualised monthly inflation reached 4½% in March on an annualised monthly basis, up from a low of about 3% late last year.

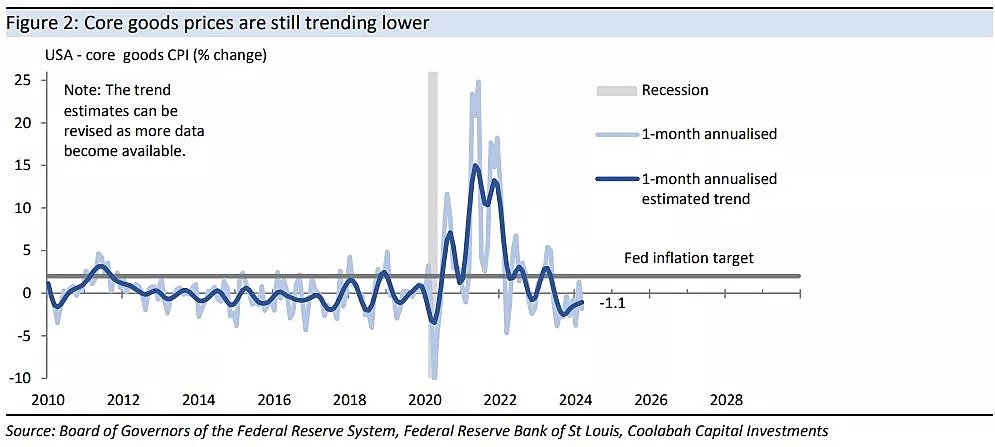

Core goods continue to fall in trend terms, declining at an estimated annualised rate of more than 1%, but services inflation remains sticky and has picked up. .

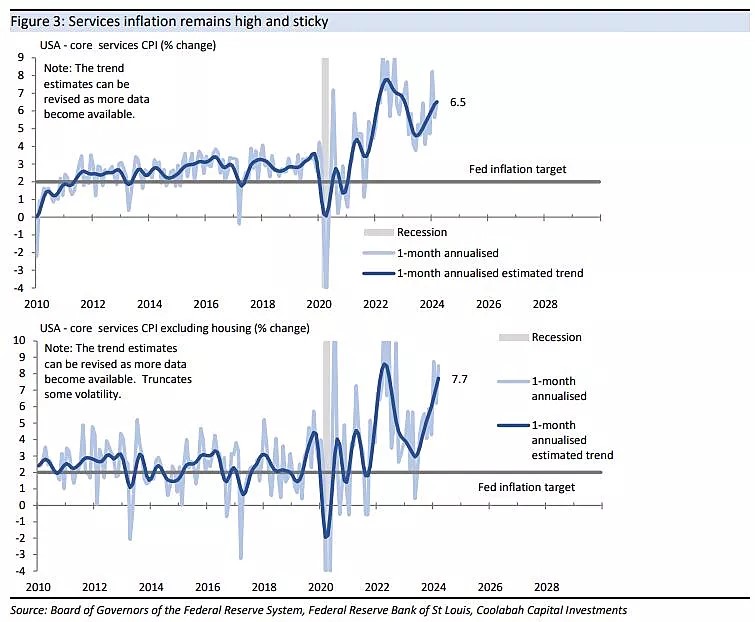

The estimated trend in core services prices shows annualised monthly inflation recently reaching about 6½%, up from a low of around 4½% in late 2023 (excluding housing, services inflation has accelerated to an even-higher 7¾%, up from around 3% in mid 2023).

CCI has repeatedly emphasised the risk posed by sticky services inflation in central banks returning inflation to target, something that policy-makers themselves have periodically acknowledged in their warnings that the "last mile" of disinflation could prove difficult.

The strength in core inflation - which should be reflected in a similar pick-up in the less timely core PCE deflator - will be disappointing news for the Fed, where some FOMC policy-makers, Fed Chair Powell included, had thought high inflation at the start of the year had reflected a temporary boost from residual seasonality in the numbers.

Higher inflation will make it hard for the Fed to have sufficient “confidence” to cut at the 11-12 June policy meeting, which is when the FOMC next updates its outlook.

This suggests the window for the start of rate cuts will shift to the 17-18 September meeting, which will start to bump up against the campaign for the presidential election on 5 November, where candidate Trump has been openly hostile towards the Fed and Fed Chair Powell.

However, if the poor run of inflation numbers persists, then it would send the Fed back to the drawing board, raising the risk that rates stay high all year, where the resumption of hikes would re-emerge as a low probability scenario if there was an ongoing acceleration in inflation.

The market is drawing a similar conclusion, with a large sell-off in rates markets leading the futures curve to now only expect less than two rate cuts this year, with the first cut fully priced in by the September meeting.

In CCI's view, the market's reassessment of interest rates staying high for longer - something that gels with the related debate over a likely increase in the neutral funds rate in recent years - presents a major challenge to the pricing of risky assets.

Risky assets - such as equities, real estate, junk bonds, and private equity - were anticipating interest rate relief this year, whereas investors should be factoring in a higher average discount rate.

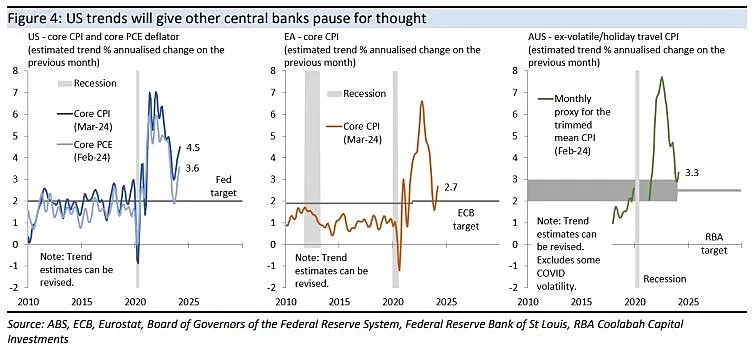

As for other central banks, US problems with sticky services inflation will give them pause for thought as some policy-makers believe the US is a little ahead of the cycle in other advanced economies given it emerged sooner from COVID lockdowns.

US core CPI inflation has picked up

Core goods prices are still trending lower

Services inflation remains high and sticky

US trends will other central banks pause for thought.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 11 April (unless otherwise stated). This document was originally published in Livewire Markets on 11 April. This information has been prepared by Coolabah Capital Ltd (ACN 153 555 867) (AFSL No. 482238).

The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.