Tell us what you’re good at

The role of investors in sensibly estimating a business’ worth can easily morph into rolling the dice when emotions are running high.

“There are a hundred and eighty slides in this pack. Which one tells me what you’re good at?”

This was a famous line from my learned colleague Mr Fleming in a meeting with a large ASX company some years ago. Suffice to say, they’d left this bit out of the presentation. Remembering to stand back and think about what we’re doing isn’t easy. As Warren Buffett noted in his recent annual letter, “For whatever reasons, markets now exhibit far more casino-like behaviour than they did when I was young. The casino now resides in many homes and daily tempts the occupants”. Though plenty of decades have passed since Mr Buffett’s youth, it’s tough to argue with his premise. Why? As Buffett’s wise (and sadly passed) colleague Charlie Munger noted, “Show me the incentive and I’ll show you the outcome”. Incentives matter. While countries such as Australia and the US insist on taxing capital gains at lower rates than personal income and resort to monetary stimulation as the antidote to any perceived economic woes, we should be unsurprised that speculating on shares and property becomes a gradually more popular way of getting ahead than working.

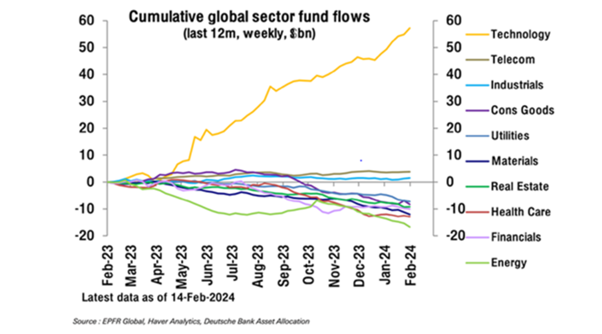

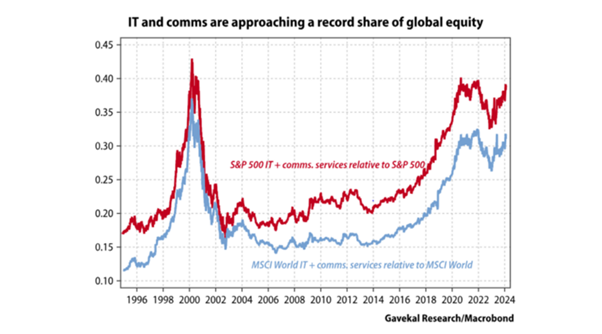

As funds continue to pile into technology stocks and bitcoin, causing prices to climb rapidly, the question of whether we are in a bubble and whether much of current market activity has anything to do with investing, is important. It will always be easier to answer in hindsight than in prospect, and those profiting from its continuing inflation have little incentive to cry wolf. Scarily, the US equity market now represents some 70% of total global equity market capitalisation, despite being significantly less than 20% of global GDP. Profit margins are near all-time highs. Around 40% of the US equity market is in technology and communication services, with Nvidia alone, now bigger than the entire US energy sector. While it’s true the crazy valuations attributed to loss-making businesses in 1999/2000 are less prevalent, pricing extremely large businesses as though they will be perpetually dominant global monopolies may merely be a different manifestation of a bubble.

Artificial intelligence is becoming a powerful aphrodisiac, and no-one wants to be left out.

Booming earnings for tech companies are a result of booming spending by other companies and governments, despite a relative lack of clarity on how productivity gains will be delivered. As one large company CEO jokingly quipped in our recent meeting, when asked by the Board whether the company should be investing more in artificial intelligence: “No, I’m surrounded by it”.

Within the casino, focus is now dominantly on ‘beats’ and ‘misses’, the atrocious Wall Street parlance for whether short-term earnings were better or worse than expectations. Analysis focuses almost solely on the extent of the earnings surprise and the commentary on short-term outlook. This seems to us the wrong question. In order to have a sustainable role, active management needs to assist in determining a company’s worth, rather than merely assimilating high frequency data on short-term earnings direction. While outsized reactions to often immaterial incremental information may hold appeal for the speculators, they are more likely to deter genuine investors. This is perhaps one reason why many larger investors are choosing to leave the casino in favour of unlisted assets. Share price reactions to recent earnings announcements provided an increasingly common mixture of the understandable (where moves seemed to roughly align with our perceptions of value changes), surprising (where reactions seem outsized relative to new information) and bewildering (where moves relative to new information seemed almost incomprehensible).

Some of the helicopter perspectives from earnings season include:

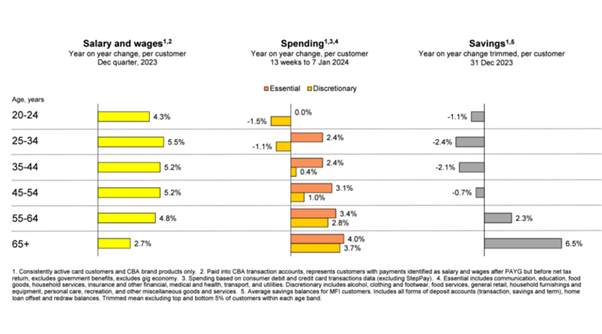

- Profitability across consumer facing businesses held up surprisingly well. While interest rate increases and broader cost of living challenges are impacting (with experience diverging depending on wealth and demographic exposure), demand held up well and pricing had generally moved ahead of cost inflation, supporting margins. However, as a number of companies cautioned, price inflation is abating and cost inflation, particularly in wages, isn’t.

Source: CBA 1H24 Results Presentation

- Government dependent revenue streams in areas such as pathology and hospitals (intermediated by private health funds) have not kept pace with cost inflation, creating significant margin squeeze.

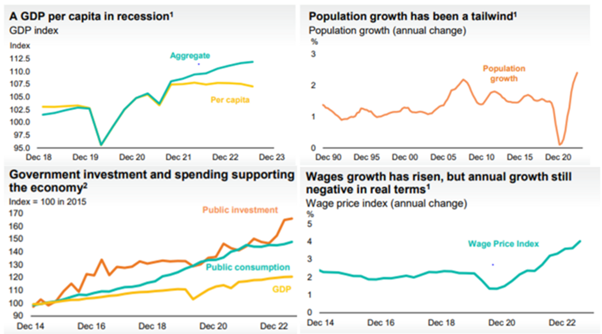

- High population growth continues to disguise weak per capita results and increasing reliance on government support. Companies remain almost universally supportive of high population growth given benefits to demand and labour availability despite the obvious pressures this is placing on housing affordability and living standards.

Source: CBA 1H24 Results Presentation, ABS

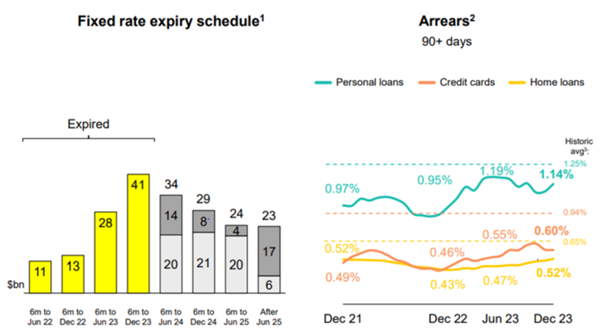

- The lags from fixed rate loan expiry are past the peak (albeit still in the early stages of impacting), and while arrears are rising, the lack of any material house price adjustment in the face of higher interest rates means bad debt issues remain largely non-existent for banks. The lack of house price falls creates a tricky environment for lowering interest rates.

Source: CBA 1H24 Results Presentation

- Plenty of companies who believed they were appropriately geared at zero interest rates proved to be less appropriately geared when interest rates moved above zero.

- As question marks on the Chinese economy abound, the divergence between Chinese exposed and US exposed businesses continues. Whilst the sustainability of a US economy propelled by massive deficit spending (offsetting any semblance of monetary tightening) causes little concern, no such optimism prevails in relation to China. Resource stocks are responding to negative commodity price momentum and resource projects are again seen as a hole in which to pour money.

- Manipulating earnings remains as popular as ever. When the casino is looking for ‘beats’, focusing on ‘adjusted EBITDA’, ignoring share based payments (also known as salary), capitalising salaries and calling it ‘R&D”, moving technology and numerous other expenses below the line, generally proves easier than actually making more money. The extent to which investors are happy to overlook these charges remains astounding.

- While productivity and margin benefits from technology remain fairly elusive for most companies, enthusiasm for technology spending remains high. When mentioning AI can add enormous amounts to market capitalisation, most companies give in to the temptation. Next DC (ASX: NXT) helpfully called it the 4th industrial revolution and painted a typically optimistic picture of long run data centre demand, aiding in another $1.8bn or so being added to market value over the month. Just the increment to value in February was about 9 times the total EBITDA of the business. Whipping investors into a frenzy is invariably easier than making a lot more money. It seems surprising to us that technology developments in which some of the greatest potential improvements are in productivity gains in producing code are not seen as a threat to companies built on lines of computer code.

The $68.50 all cash takeover bid for Altium from Japanese company Renesas (which I believe translates to ‘Paid too much’) provided the fuel for another month of extraordinary gains for everything tech related. The $8.8bn enterprise value of Altium at the takeover price is around 20 times sales and 100 times earnings, pouring fuel on the fire of the ‘house next door’ investment strategy, where crazy valuation benchmarks justify extrapolating craziness to anything tangentially related. Yet another apparently crazy Japanese offer again forced contemplation of the value of money and the longer term end game of countries like Japan issuing seemingly endless streams of debt (with almost no obvious prospect of repayment) at negligible interest rates in return for ownership of organisations which may be crazily priced, but are arguably of more value than the debt, but that’s a much bigger question.

Of the associated tech share price reactions, Wisetech Global (ASX: WTC) probably took the award for the most outsized. In a half yearly result which saw revenue of $500m and reported EBITDA of $230m (aided by significantly increased R&D capitalisation), perhaps $20m higher than expectations, the market value increased by some $7bn over the month, or around 350 times the purported earnings surprise. In our picture of the world where value creation requires associated earnings, an 8-10% return on $7bn of additional market value requires a company to earn another $600m or so in operating earnings, FOREVER.

While Wisetech may have done a great job in growing its business, the sustainable cash earnings of the company (not the EBITDA, or ‘bullsh*t earnings as Charlie Munger called it) are not yet anywhere near the $600m to provide a reasonable return on the move in the month, let alone the $2.5bn or so required to justify the current $30bn+ valuation. A ‘trophy’ property indeed.

Other fashionable houses on very popular streets such as Xero (ASX: XRO), Technology One (ASX: TNE) and Block (ASX: SQ2), registered significant gains in value without anything much in the way of news to support them. The disappointing reported results of Altium (ASX: ALU) which followed a couple of weeks after the bid provided far more questions than answers on how the bidder arrived at their estimate of value. Nevertheless, the fortunate shareholders will record the gains and winners write the history.

Back in reality, where most of the holdings in our client portfolios reside, a takeover bid for Alumina (ASX: AWC) by Alcoa, the controlling shareholder in the AWAC JV, caused the share price to decline over the month. As Homer Simpson would say; Doh! If successful, the bid will see the joint venture in one of world’s largest bauxite and alumina businesses unwound and exchanged for a shareholding of 31.25% in Alcoa. While the transaction history is yet another bitter one for Australia (like BHP’s bid for Billiton and the RTZ CRA merger which formed Rio Tinto) where the 40% interest of Alumina in the AWAC JV was a result of Western Mining contributing some very good assets while Alcoa received a 60% interest through contributing some very bad ones, this is history. Merging the assets again makes sense and removes cost and operating complexity. Given the AWAC JV is the only asset of Alumina and the major asset of Alcoa, the debate around a fair ownership interest for Alumina shareholders is around the value of residual aluminium smelters in the Alcoa portfolio. These are a mixture of very good assets (hydro powered in Canada) and poor assets (European refineries exposed to high energy costs). The view on the value of these assets reduces the extent to which Alumina shareholder’s interest in Alcoa falls from the 40% level (which would imply no value for any assets outside the AWAC JV). While an informed view of refinery value is complicated, with increasingly investor unfriendly jurisdictions in Europe raising the spectre of some assets being a liability, our initial assessment would see the deal as reasonably fair. Debating the pluses and minuses on a combined business with assets which would cost tens of billions to replace yet is valued at little more than the Wisetech monthly market value gain often seems surreal, but the casino sets the values. Commodity prices and demand dictate low levels of current profitability and when most see no earnings momentum they see no value. We see plenty.

Interestingly, while trends remain firmly against asset intensive businesses, domestic building materials are a notable exception.

After CRH’s successful $2.1bn bid for Adelaide Brighton, the past month has seen Seven Group (ASX: SVW) bid for the 30% share of Boral (ASX: BLD) it doesn’t own and Saint-Gobain bid $4.3bn for CSR. The providers of raw materials and building products essential to construction of the country’s housing stock and infrastructure remain valued at a tiny fraction of the end products; the result of long years of poor management and barely adequate margins in an industry where returns and incentives favour rampant speculation on the price of existing infrastructure and housing over building much new stuff. Vastly improved management of companies like Boral have shown what is possible with some discipline and productivity focus. While our hopes and exhortations for similar efforts at Fletcher Building (ASX: FBU) have to date fallen on deaf ears, culminating in downgraded earnings and the announced departure of the Chairman and CEO, we remain strong believers in the potential for far greater value. Perceptions can change. While property development and construction in the hands of Fletcher Building or Lend Lease (ASX: LLC) has set fire to billions in shareholder’s funds with the future valued accordingly, the same activity in the hands of Next DC or Goodman Group (ASX: GMG) sees perceptions change and wildly different valuation paradigms. Performance fees and a future of vastly profitable developments are capitalised into perpetuity. Removing the $8.80 of published NTA from the Goodman Group valuation (which includes the value of all properties and existing development holdings, leaves around $41bn extra for a property management and development business. It is no wonder there are a few data centre slides to keep analysts excited about the digital infrastructure future. While in no way diminishing the amazing job of management teams at companies like Goodman Group, when valuations expect King Midas to be in charge forever, there is plenty of scope for disappointment.

As for many in the investment community, the announcement of Brad Banducci’s departure from Woolworths (ASX: WOW) was the source of some disappointment. As the possibly apocryphal Einstein quote goes;

“Not everything that counts can be measured and not everything that can be measured counts”.

Whether Woolworths is a much better business now depends on how you want to interpret the myriad of financial, customer advocacy, staff engagement and logistics efficiency indicators. What seemed clear in talking to Brad is that he cared a lot, gave everything he had and tried to do the right thing; attributes not immediately apparent in every CEO we encounter. Having discussed the state of government intervention and regulation with a raft of companies over recent weeks it is difficult to be optimistic. Rather than looking at incentives and the structure of economy, we are hoping for salvation in excessive regulation and government intervention. Artificial intelligence does not seem to be making it easier to do the right thing. Lengthy discussions with ASX management on who they consider their important customers and how they assess the health of the marketplace in which we are all operating only serve to reinforce the validity of Charlie Munger’s wise words. Having spent years creating incentives supporting trading speed, market making, selling data to the highest bidder and a voluminous set of rules, it is little wonder we’ve ended up in a casino.

Market outlook

Most indicators would suggest the economy and profit margins are healthy having digested the challenges of higher interest rates better than anticipated. As investors happily chase profit momentum ever higher and technology and the US equity market build ever greater dominance, we can’ help feeling the picture below the surface is far more complex. Bitcoin scaling new heights or Nvidia (NASDAQ: NVDA) breaking US$2trillion in market capitalisation might be cheered by investors with a ravenous appetite for more speculative gains; it does not seem to us indicative of either a healthy equity market or economy. The blame for the cost of living crisis in Australia does not lie at the feet of supermarkets or the 65% market share of Coles and Woolworths. Incentives are crucial. Simplistic measures such GDP growth and ever greater dependence on asset prices mean population growth and house price gains have substituted for productivity improvement for many years. While many companies remain focused on excellence in their chosen fields, many others are focused on growing bigger rather than better.

Like the country overall, ensuring incentives are directed towards being better rather than bigger will remain crucial for delivering growth in value over time. Market value or economic growth which is built on hot air and speculation will never be durable.

Equity markets seem to us to be substituting earnings momentum and EBITDA growth for thinking about the how and why a company should be worth the prevailing market value and how incremental pieces of information influence business value. Chasing the next speculative gain is becoming more tempting than ever and signs of bubble-like conditions are everywhere for those with an appetite to look. Much as retaining focus is difficult when the temptation towards speculation is high, it is always when it’s most important.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 18 March 2024. This document was originally published on Livewire Markets website on 18 March 2024. This information has been prepared by Schroder Investment Management Australia Limited (ABN 22 000 443 274, AFSL 226473).

The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.