Can A-REITS still deliver for your portfolio?

Bond yields have risen to new heights and are now roughly in line with the yields on offer from commercial property.

Many investors might eye the now juicy yields on offer from these relatively risk-free assets compared with arguably the risker commercial sector.

However, Morningstar equity analyst Alex Prineas notes that there is potential upside for investors compared with bonds, despite the higher risk that comes with commercial property.

Physical office buildings are still being priced at cap-rates, or yields, of circa 5-6%, but office REIT Dexus (ASX: DXS) is currently trading on a 7% dividend yield, as it trades at a substantial 40% discount to its net tangible assets.

The commercial property sector is confronting headwinds such as remote working which remains the norm as well as recession fears.

However, “even if earnings and distributions fell, say,25%, Dexus’ distribution would still be on par with what you are getting with a 10-year government bond,” Prineas says.

What does that mean for the outlook for commercial property? If risky commercial property offers similar yields as risk-free government bonds, could property prices fall?

“Morningstar’s view is that physical commercial property prices will fall substantially, but not as far as implied by listed markets, which have already priced in a lot of bad news” Prineas says.

Be selective

“Many of the major REITs look cheap, especially in the office sector. Caution needs to be taken in assessing the balance sheets for REITs though. Some of the weaker names are under intense pressure,” he adds.

Here is where Morningstar’s investment lens is key, with Prineas preferring to focus on high-quality names such as Mirvac (ASX: MGR) and Dexus. Importantly he highlights that these businesses have strong balance sheets that should steer them through tough times such as a recession, which may not be the case for REITs that have weaker balance sheets, or lower quality assets.

Amid a potential recession, Prineas favours large retail and office REITs due to the protection they get from long leases compared with the self-storage sector.

“In a recession, sectors like storage could get hurt as storage typically has no leases. We also note that the cap-rates for the storage sector aren’t much higher than yields on offer from retail and office. Storage has also seen strong rental growth, whereas office rents are depressed at the moment. So, we see more downside risk for storage in the event of a recession,” he says.

He also notes that businesses like Dexus have quality tenants who are better placed to work through a recession.

Local shopping centres owned by businesses like Charter Hall Retail REIT (ASX: CQR) are also well-placed in a challenged market as are high value shopping malls such as the beautiful Warringah Mall on Sydney’s northern beaches owned by Scentre Group (ASX: SCG).

“These are also a defensive play. Retail REITs face recession risk but two years of strong retailing has helped landlords to sign good tenants on long leases.”

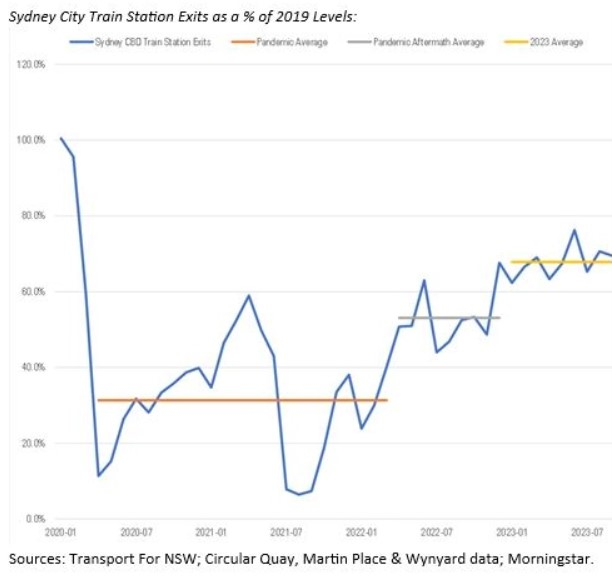

On the remote working front, data has revealed foot traffic returning to offices. “Hybrid working is a big headwind, but actually the biggest headwind has been new office supply coming onto the market from developments that started back before the pandemic,” Prineas says.

“We think we are now past the peak of supply and new developments should start to taper off. We also note that central business districts are getting busier and are likely to get busier again in the next few years from strong population growth and the rollout of new transport projects such as the Sydney Metro opening.”

What about residential?

Strong balance sheets and a good pipeline of projects are also crucial for residential REITs particularly with the high level of construction insolvencies plaguing the market.

“We think big developers like Mirvac and Stockland (ASX: SGP) are well placed to sell the dwellings coming through in their pipelines for the next couple of years.

“We’ve also seen that construction costs aren’t falling, but they’re no longer rising as fast as they were pre-COVID. So that should be supportive of profit margins for the residential developers.”

Investors also benefit not just from the commercial property yields but also the distribution and earnings from REITs which are expected to grow despite the challenged economic outlook, says Prineas.

First published on the Firstlinks Newsletter. A free subscription for nabtrade clients is available here.

Christine St Anne is communications manager at Morningstar Australasia. All prices and analysis at 1 November 2023. This article was originally published on Morningstar Australia on 1 November 2023. This information has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892 .

The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.