All budding investments begin with elements of discomfort

It is unclear if we are on the cusp of a deep or protracted cyclical downturn. What is clearer though, is that if a recession is imminent, it is likely to be one of the world’s most telegraphed recessions yet. Share markets are forward looking so we consider that these expectations have already been factored into share prices, at least to some degree.

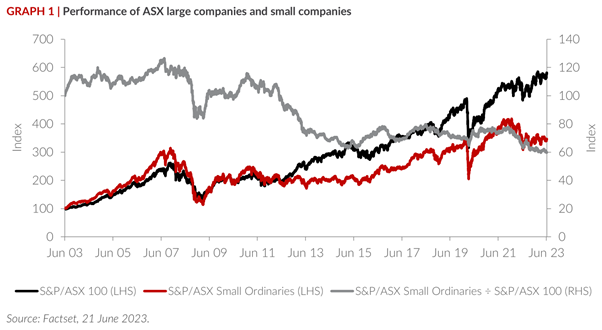

Over recent months, equity investors have gravitated to the perceived safety of large companies at the expense of ‘riskier’ smaller companies. Graph 1 illustrates this. It plots the performance of the S&P/ASX 100 Index (the largest 100 companies listed in Australia) and the S&P/ASX Small Ordinaries Index (the next 200 largest companies listed in Australia). The Small Ordinaries Index is now at its lowest point relative to the ASX 100 Index since April 2000 when the Small Ordinaries Index first launched.

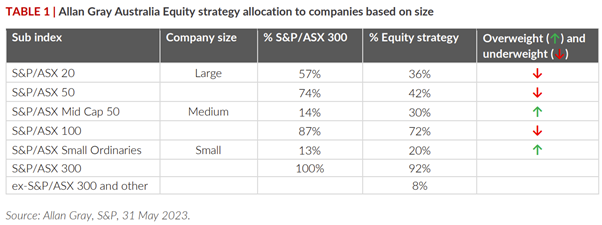

While the Allan Gray Australia Equity strategy does own some large companies, it has a significant skew towards medium-sized and smaller companies (see Table 1). It is here that we think the greatest upside potential exists. Lendlease (ASX: LLC) is one such medium sized company. If it’s true that good investments often begin with an element of discomfort, then Lendlease would fit the bill.

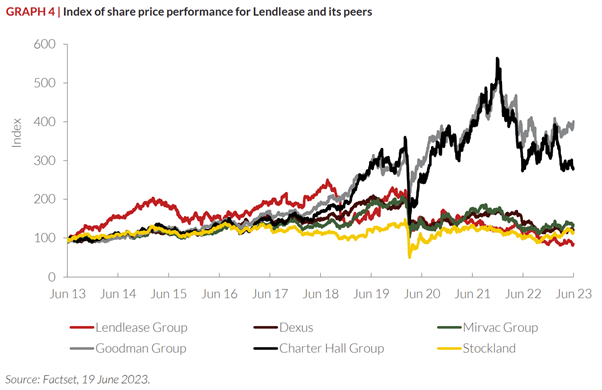

Lendlease’s share price performance has been woeful and makes the performance of the Small Ordinaries Index look like that of an artificial intelligence chip designer. Analyst, Tim Morrison, discusses our Lendlease discomfort below.

Lendlease is best described as a global real estate company with vertically integrated operations across development, investments, and construction:

- Development – funds and project manages new real estate projects from idea to execution to sale.

- Investments – earns fees on Lendlease-managed real estate fund assets. It currently has $40 billion of assets under management. Approximately $36 billion of this is from third party investors with approximately $4 billion being from Lendlease’s own balance sheet as it invests alongside external capital partners.

- Construction – builds real estate projects, including some internal Lendlease-developed projects. Lendlease has a $10 billion external construction backlog.

Each of these segments is described further below.

Development

In its development business, Lendlease has $5.9 billion of invested capital, which funds projects at various stages of completion. The development business first secures a site and planning approval, only typically entering a fixed-price construction contract once it deems there to be sufficient presales (apartment deposits) or pre-leasing commitments from major tenants (offices) in place. Lendlease’s development business employs either an external construction firm or Lendlease’s own construction business to build its development projects.

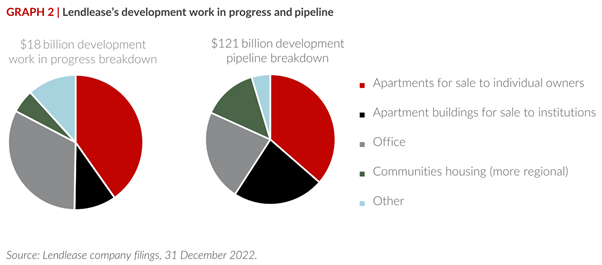

Most of the development projects are in major global city centres. It has $18 billion of work in progress today, a $121 billion long-term pipeline and ambitions to complete $8 billion of new projects annually.

More than half of Lendlease’s $121 billion pipeline is ‘land management’ deals, which should reduce Lendlease’s development downside (and upside) as the land cost for Lendlease is assessed towards the end of the project, generally subject to a priority minimum return for Lendlease.

Graph 2 details the split in Lendlease’s development work in progress and pipeline. Lendlease’s management expects the development business to make a 10-13% return on invested capital through the economic cycle.

Investments

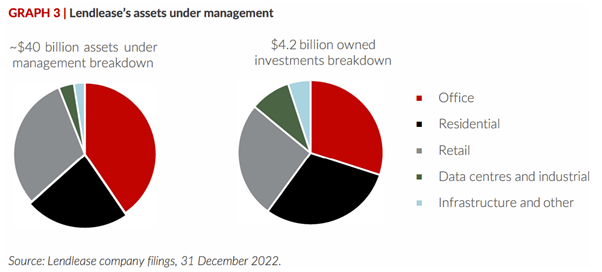

The investments segment manages $40 billion of real estate investments as well as property asset level operations such as leasing. Fees are at least 0.75% p.a. of market values on which Lendlease earns at least a 35% pre-tax operating profit margin.

Lendlease itself owns $4.2 billion of equity, largely within the $40 billion of assets it manages and so also earns an investment return (rental income plus movements in market values) on this co-investment. Lendlease targets a return on invested capital of 6–9% for its investments business.

Graph 3 shows the split of Lendlease’s assets under management and owned investments.

Construction

Construction is predominantly an Australian and United States based business. It has annual external client (non-Lendlease development related) revenue of about $7 billion currently and it targets a low 1.5-2.5% pre-tax operating profit margin. Through a mix of employees and third-party subcontractors, this segment builds social infrastructure (hospitals, train stations, museums), defence facilities (airfields and other military bases) and commercial property for Government (60%) and external corporate clients (40%).

Managed correctly, Lendlease’s business segments together represent a self-reinforcing ecosystem. A significant portion of Lendlease’s development pipeline could potentially flow into Lendlease’s assets under management upon completion. Having an internal construction capability should assist Lendlease’s development business in negotiating reasonable contracts with external construction companies.

Oh Lendlease, what have you done?

Returns to Lendlease’s shareholders have been spectacularly poor. Over the past 10 years, Lendlease’s share price has gone backwards — worse than most companies in the index. Most of Lendlease’s underperformance has come in the past five years.

There are several reasons for Lendlease’s woes:

- Engineering construction project losses — Lendlease lost $1.5 billion in the last five years on underpriced Australian fixed price engineering construction projects. The biggest loss came from the Melbourne metro train tunnel project.

- Aggressive recognition of development profits pre-2022 — when Lendlease sold partial stakes in incomplete development projects (as a way of recycling capital early), it used to recognise development profits on its incomplete retained stakes. Their changed accounting practice of recognising profits on completion has created a profit hiatus across 2022-2025 as the company plays catch up and completes its projects upon which some profits have already been recognised upfront.

- Real estate exposure mix — Lendlease’s business is generally skewed to major global city centres that were heavily impacted by COVID-19-related restrictions of movement. This has since morphed into lingering declines in office attendance (at least for now), and concerns around the need for development impairments.

- Lendlease’s investments — segment real estate valuations are expected to decline, mainly due to the recent increase in interest rates.

- Bloated cost base — despite a major cost reduction drive by the current CEO, Tony Lombardo, Lendlease still has an annual overhead cost of $700 million. Lendlease’s high cost base still poses risks to shareholders, as it may lead the company to undertake poor transactions to spread that high fixed cost base at wrong points in an economic cycle.

- Balance sheet concerns — we believe reported gearing of 16.8% understates the reality and may increase significantly. About half of the losses associated with the previously mentioned engineering projects have yet to be paid for (they have just been accrued for), and there is a significant amount of debt attached to various equity interests in unconsolidated and geared investments. Lendlease is also publicly targeting a $2.6 billion increase in investments-segment capital employed and it is not clear how this will be funded. Concerns around the need for an equity raising or value-destroying asset sales abound.

The silver linings?

The above is a long rap sheet of negatives but we believe there is cause for some optimism:

- While past losses from the engineering business are a permanent loss of capital, the recent sale of this business in 2021 means that these losses will not repeat.

- Around $0.4 billion of the $5.9 billion development capital is unrealised profit aggressively recognised under Lendlease’s pre-2022 accounting practice. Lendlease’s actual total profit from the relevant development project stakes is anticipated to comfortably exceed $0.4 billion, mainly due to two 75%-owned Barangaroo (Sydney) apartment projects that are 93% pre-sold and expected to be extremely profitable.

- Lendlease has already written down its development capital base by $0.3 billion. Most of its development capital base is reflected at historical cost (as opposed to upward-adjusted market values like REITs do). Overall, it seems likely the development capital is conservatively stated today.

- While the $4.2 billion of owned real estate equity is expected to be marked down, and the assets under management along with it, some development completions will also flow into assets under management, providing a valuable offset.

- The company’s bloated cost base is not lost on management. It has already delivered $170 million of cost reductions, and they intend to cut costs even more.

- Several sale processes are in advanced stages of execution that, together with earnings retentions over the coming years, should help the company reduce its debt burden. It remains to be seen whether the sale proceeds will be reasonable but management commentary on these processes seems to have been sensible so far. What’s more, in recent times, the company has repeatedly denied any need or intention to raise equity (although we have heard that from other companies before!).

The silver bullet?

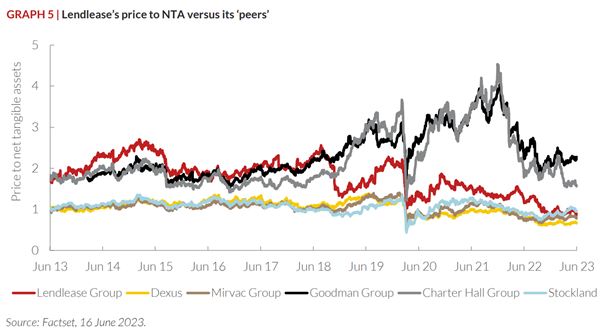

By far the biggest cause for optimism, though, is Lendlease’s share price. At $7.75 per share as of June 30th, Lendlease is trading at a slight discount to its net tangible assets (NTA).

This might look expensive relative to REITs like Dexus and Mirvac (refer to Graph 5), but these comparisons are misguided. REITs reflect nearly their entire invested capital bases at market value that, until very recently, have increased significantly. A significant proportion of Lendlease’s balance sheet is effectively carried at cost (or net realisable value if lower than cost). Also, its business is more skewed towards higher-returning development and fund management earnings than the REITs, and so it is arguably more like Goodman Group and Charter Hall, which both trade at significant premiums to their NTA.

Lendlease is targeting an after-tax return on equity of 8-10% or approximately $600 million in profit. While these return assumptions are not heroic, they have also not been achieved in a long while. At its current price ($7.75), investors are paying nine times these targeted earnings. To be on the same earnings multiple as the broader share market, Lendlease only needs to deliver a 5% return on equity, compared to its target of 8-10%.

We believe there could be significant upside if Lendlease management is able to deliver on its targets and, in our opinion, relatively more modest downside if it doesn’t.

BIOGRAPHY & DISCLAIMER FIELD

Simon Mawhinney is Managing Director and Chief Investment Officer at Allan Gray. All prices and analysis at 11 July 2023. This information was produced by Simon Mawhinney and published by Livewire Markets (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.