This is going to hurt

Tim Toohey | Yarra Capital Management

In a December Insight piece of the cashflow crunch ahead for discretionary spending we noted:

“The argument that Australians have accumulated ‘buffers’ via $260bn in ‘excess savings’ since the pandemic and via pre-payments on mortgages will exceed additional interest payments for most borrowers is illusionary.

While this might be true in an accounting sense, the RBA is likely asking itself the wrong question. It is not a question of how big a ‘buffer’ is before tightening policy will hurt, it is why did household accumulate such a buffer in the first place? And is the economic outlook improving or deteriorating?”

In the interim the RBA has continued to cite the buffers argument while pivoting to a seemingly much more hawkish position over the summer period. The RBA has recently lifted their estimate of the scale of accumulated savings to an estimated $300bn. We don’t believe the excess is quite that large. If we hold the saving rate at its pre-COVID level and look at the savings accumulated since the start of COVID the ‘excess saving’ is between $250bn and $260bn. In this note we will continue to use the upper estimate of that range as the ‘excess saving’ buffer, yet the conclusions remain unchanged if we adopt the RBA’s higher figure.

The RBA referenced this ‘buffer’ on numerous occasions during its testimony to Parliament in mid-February, yet we have seen nothing from the RBA on the distribution of this savings ‘buffer’. We have, however, had an update from the Australian Bureau of Statistics (ABS). Its detailed data for 2022 on income, savings, wealth and consumption enables us to look at the winners and losers since COVID commenced, and to assess who is likely to be impacted most as we move into a slower growth, higher interest rate and more fiscally austere environment.

There are several initial key points that can be gleamed from this ABS data set.

#1. The bulk of the savings have been accumulated by 'mature’ households.

Approximately $163bn or 63% of the ‘excess savings’ of $260bn have been accumulated by households over the age of 45 years old. Remarkably, those of retirement age managed to save $51bn, just as much as working age workers (45-54yo) and only slightly less than the 55-64yo cohort. Households aged 65yo and above have historically had a very low single digit saving rate, with older households actively dissaving into retirement.

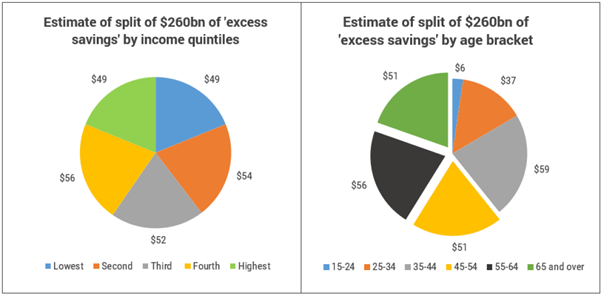

#2. The ‘excess savings’ were very evenly distributed across the income spectrum.

This is an unexpected finding, since typically the bottom 20% of households ranked by income demonstrate negative saving behaviour through time. The second lowest income quintile has also historically demonstrated negative or only marginally positive saving patterns. By contrast, the top 20% of income earners typically save around 35% of income and the second highest quintile of income earners save around 17% of income. However, since the start of COVID each of the income quintiles saved between $49bn to $56bn. This is a remarkably consistent saving achievement regardless of income level.

Exhibit 1: ‘Excess savings’ by income and age – a remarkably even distribution of savings

Source: ABS, YarraCM.

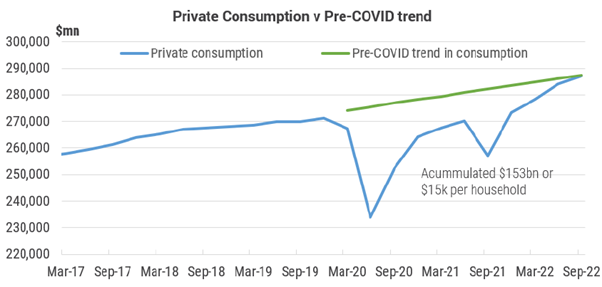

How much of this 'excess saving’ was due to 'deficit consumption’?

If we define ‘deficit consumption’ as the difference between the pre-COVID trend in consumption and actual consumption, we can then approximate how much of the accumulated saving can be attributed to deficit consumption during the COVID period and how much can be attributed to ‘precautionary’ saving and portfolio decisions.

Naturally during COVID lockdowns, spending patterns were heavily influenced by travel restrictions, working from home and restrictions on social gatherings. By now everyone is very familiar with the stimulus induced surge in goods spending and the initial large drop in services consumption and the subsequent partial recovery in services. The consumption data results were a truly historic deviation from trend.

In aggregate, we estimate that households consumed $153bn – or $15k per household – less relative to the pre-COVID trend in consumption. From this we can infer that households precautionary saving was around $107bn or $10k per household.

Exhibit 2: $153bn of the $270bn of excess savings can be attributed to consuming less since COVID

Source: ABS, YarraCM.

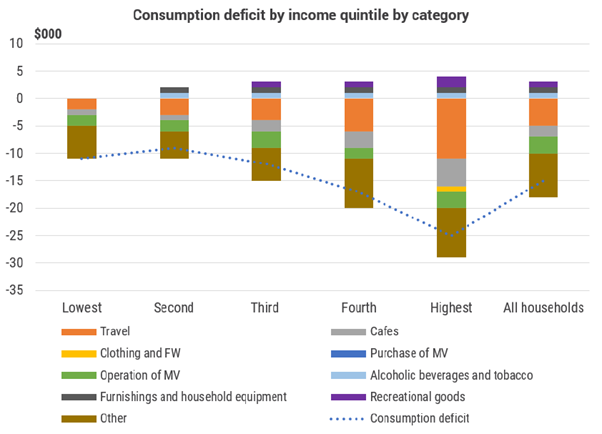

Before we delve any deeper into the nature of saving decisions, it is instructive to breakdown the consumption deficit by income and by age.

Exhibit 3 shows that that of the $15k of saving attributed to deficit consumption per household, $5k is due to a reduction in holiday travel, $3k is due to driving less during COVID and $2k is due to reduced eating out at cafes and restaurants. On the flip side, households spent $3k above trend, equally spread between alcohol, furnishing and household equipment and sporting goods.

For the top 20% of income earners the consumption deficit is $25k per household, yet two-thirds of the reduction is due to less travel and lower restaurant spending. At the other end of income distribution, a reduction in travel and restaurant spend represented just one-third of the consumption reduction. Moreover, low-income households were clearly not the ones using COVID to refurnish their houses, buy new exercise equipment nor were they the source of surging alcohol sales.

Notably, the ‘saving’ that accumulated due to a reduction in motor vehicle use, since people spent less on petrol and repairs while mandated travel restrictions remained in place, was a relative consistent $2-$3k reduction regardless of income level. This represented one-fifth of the ‘consumption deficit’ and highlights the non-discretionary nature of fuel and motor vehicle travel.

Exhibit 3: Restriction of travel/restaurant spend by high earners was a large source of ‘excess saving’

Source: ABS, YarraCM.

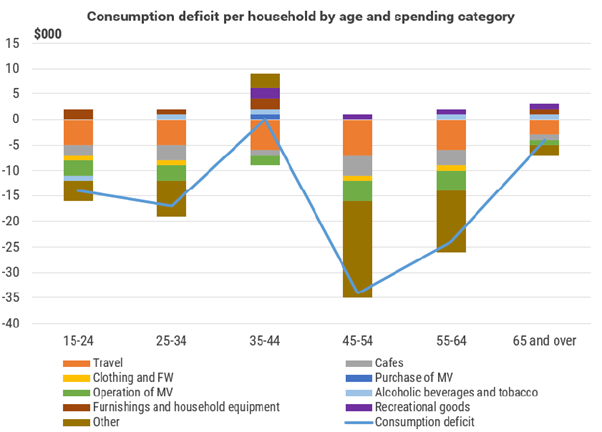

Conducting the same analysis by age group reveals some additional insights:

Firstly, there is a clear dichotomy between the behaviour of working age households above 45yo and those below 45yo.

- The data reveal evidence of a broad-based reduction in consumption for those aged over 45. The reduction in travel and motor vehicle use was broadly similar in dollar value across age brackets, however, well over half of the reduction in consumption in the above 45yo working age households is due a reduction in spending beyond the COVID impacted categories of travel, restaurants, clothing, motor vehicles, alcohol, household goods and sporting goods. This is solid evidence that 45-64yo households had been engaging in genuine precautionary saving. Regardless of whether this is proximity to retirement or collective memory of what happened to asset prices during the Global Financial Crisis, it is clear that older working age households reined in consumption relative to younger households.

Secondly, the party was at the 35-44yo’s house during the COVID lockdowns.

- This cohort was the much-maligned older half of the millennials who 15 years ago were tagged as lacking ambition and more interested in ‘experiences’ rather than working. This is clearly the most interesting of the cohorts. While everyone else was building their savings balance, this group of aging millennials kept right on spending (refer Exhibit 4). What they couldn’t spend on travel and restaurants they more than made up for by buying a Peloton bike and home gym, updating their TVs and furniture, stocking up the cellar whilst revealing that they were the only cohort who thought buying a new car was a good idea during mandated travel restrictions. As a consequence, 35-44yo households appear to have accumulated no additional savings as a result of consuming less since COVID arrived.

Exhibit 4: The party was at the 35-44yo’s house during COVID!

Source: ABS, YarraCM.

Tax, debt payments and equality – a remarkable pandemic journey

Now that we have a picture of who saved and who consumed by income and age, it is instructive to step back and look at these shifts in saving and consumption relative to shifts in household income and two of income’s biggest drivers: (i) income tax paid; and (ii) debt interest payments.

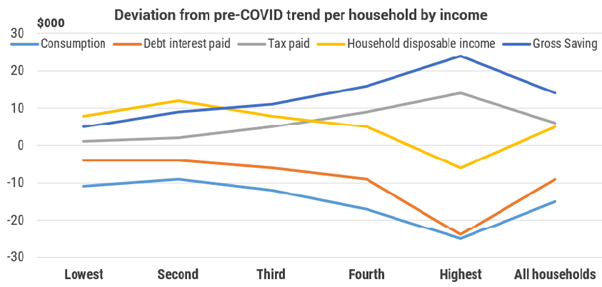

Exhibit 5: Income was above trend post COVID for all but the highest income households

Source: ABS, YarraCM.

The first question that likely comes to mind from Exhibit 5 is how is it possible that, during the hardship of a global pandemic, Australian household disposable income had a positive deviation from its pre-COVID trend for all but the highest income earners?

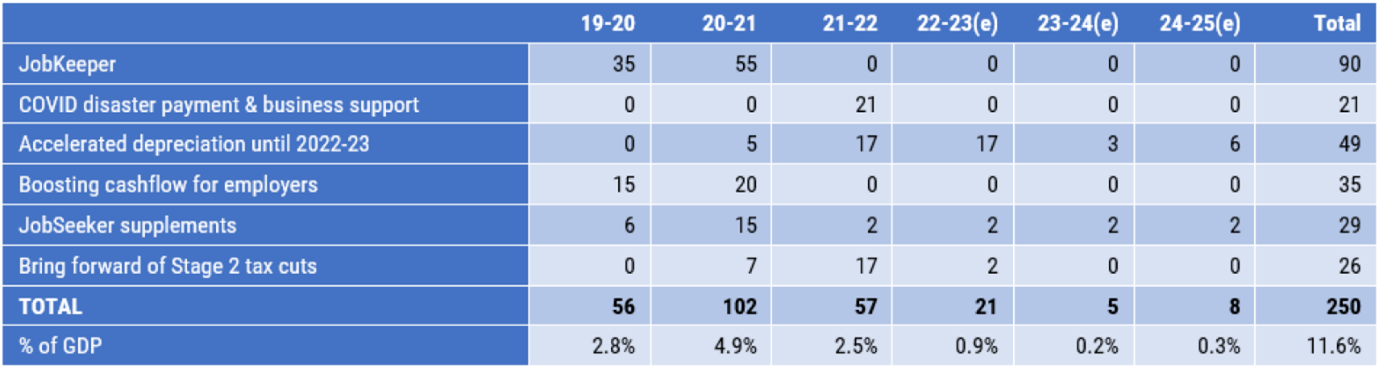

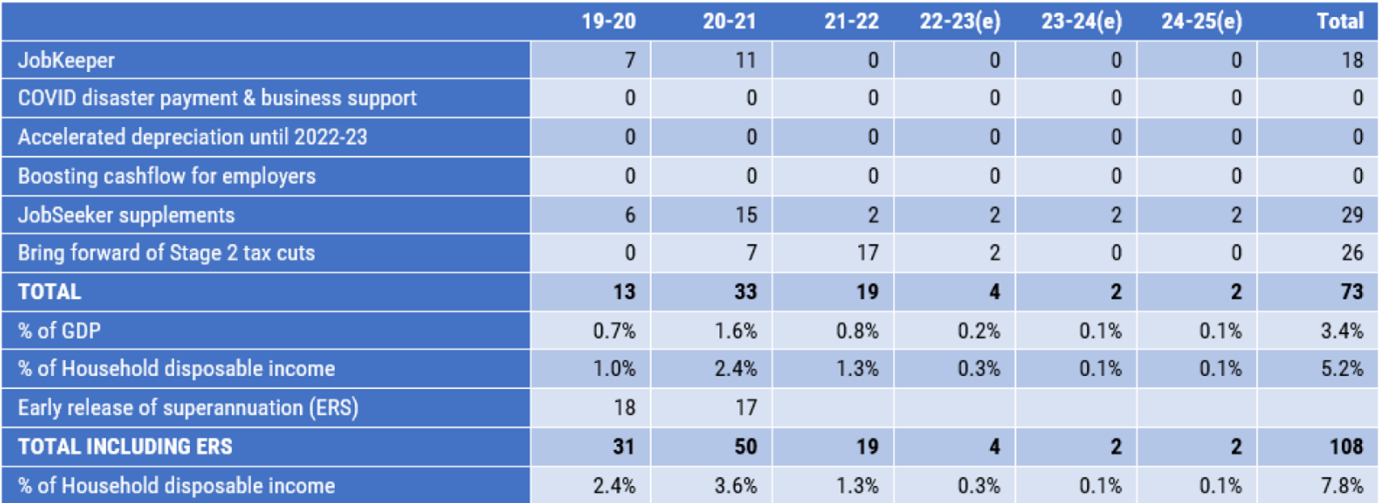

To answer this, recall that size of Australia’s fiscal stimulus during COVID was of unprecedented proportions – amounting to $215bn in the three years to 2021-22 or 10.4% of GDP (see Table 1). Not all of this flowed directly to households. In particular, while the JobKeeper program was technically a business subsidy, around 20% of JobKeeper funds was a replacement for unemployment benefits or JobSeeker. We estimate that the higher payment of JobKeeper relative to JobSeeker for these recipients provided an $18bn boost to household income between 2019-20 to 2021-22. Together with the temporary increase in the JobSeeker payment ($23bn) and the bring forward of the stage 2 tax cut ($24bn) this has resulted in an additional $65bn flowing directly to household income via the fiscal pandemic response. Of course, this excludes the boost to spending capacity from the Early Release from Super (ERS) policy which released a further $35bn. Including, the ERS the direct fiscal benefit for households since 2019-20 equates to $100bn, a massive 7.3% of household disposable income (see Table 2).

Table 1. Federal Budget cost of COVID-era policy measure ($bn)

Source: Commonwealth Treasury, YarraCM.

Table 2. Federal Budget cost of COVID-era policy measure - Estimated household benefit ($bn)

Source: Commonwealth Treasury, YarraCM.

The vast majority of the fiscal package was directed towards average and lower paid households, and, in terms of the ERS, the Australian Prudential Regulatory Authority (APRA) has detailed that that it was young and low-income households that dominated the withdrawal from super. There are 10.2mn households in the Australian economy and excluding the top 20% of income earners there are 8.2mn. In simple terms, the $65bn fiscal boost to household income divided by 8.2mn households equates to $7.9k of fiscal support per household. This is almost exactly the average increase in household income relative to its trend (refer Exhibit 5) and provides a useful cross-check on the attribution of the boost to household income.

In other words, the boost in household income relative to trend can be directly traced to the size and timing of the fiscal payments, and the $7.9k per household perhaps provides a retrospective assessment of the magnitude of ‘excess’ fiscal stimulus that was delivered during the COVID period.

The principal reason that the distribution of saving had been so even across the income spectrum was that the generosity of the fiscal transfer flowed disproportionately to lower income households. The scale of the fiscal transfer was clearly excessive, but from a fairness perspective the design of the fiscal package was a success.

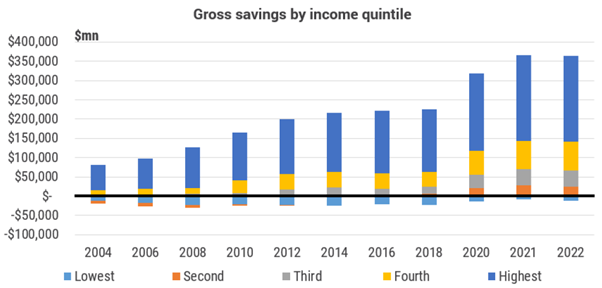

A second question that likely arises from Exhibit 5: how is it that higher income households saved just as much as the other quintiles saving despite household income for the top 20% being negative relative to the pre-COVID trend? As Exhibit 5 shows, this occurred despite high income earners enduring a greater relative increase in income tax paid. The simple answer is high income earners are always the predominant source of savings in the economy, and hence have greater bandwidth relative to others to shift their spending and saving habits. This is best seen by a simple chart of the level of gross saving by income quintiles (see Exhibit 6).

Exhibit 6: Income was above trend post COVID for all but the highest income households

Source: ABS, YarraCM.

The slightly more complicated answer is that the top 20% of income earners were the only quintile to materially alter their appetite for debt. Relative to the pre-COVID trend, the highest income earners reduced mortgage debt by $19k on average, compared with a $18k increase in debt per household by the next two income quintiles. This mortgage debt reduction relative to trend was also only recorded in households over the age of 45. Thus, despite higher income households receiving less income relative to the pre-COVID period, paying more income tax, and receiving relatively little of the $100bn of COVID fiscal relief that boosted the incomes of younger and lower income households, higher income older households made deliberate decisions to be more conservative in their spending and appetite for debt.

All of this data crunching reveals that the vast bulk of the accumulation in ‘excess saving’ has been in households where the household head is over the age of 45. Households over the age of 45 simply took a more cautious approach. They consumed less, they took on less debt and, given the top 20% of income earners hold 40% of total household debt, the reduction in the mortgage interest rate during the COVID period saw a greater reduction in debt interest paid.

It is relatively obvious at this point to note that the vast majority of mortgage holders that are ahead of their scheduled pre-payments are highly likely to reside in the top 40% of income earners, with a large skew to the top 20% of income earners and they are more likely to be households over the age of 45. These are the households that could afford to keep their repayments unchanged as mortgage rates fell, enabling a faster repayment of the principal. The RBA has referenced raising interest rates to eliminate the pre-payment buffer for households as a measure of where they expect monetary policy to really begin to impact. However, by focussing on a system-wide average of pre-payments rather than focussing on income and age profiles of borrowers, the RBA’s aggressive rate hikes are about to leave the bottom 60% of income earners and younger households in a highly exposed financial situation.

The surprising lack of household wealth & income distributional impacts of the COVID era

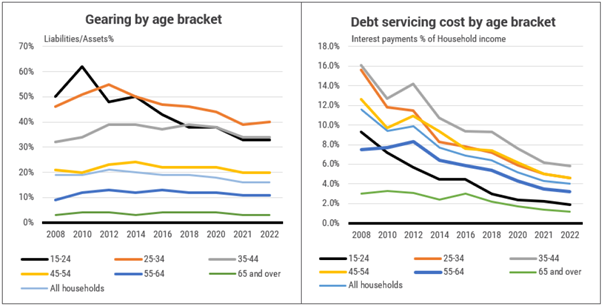

Perhaps one of the more surprising findings from the ABS data is that it is difficult to identify material wealth and debt distributional shifts since the start of COVID. We suspected that lower interest rates, booming credit growth and rising asset prices would have altered the gearing and debt distribution across the Australian economy. Apparently not.

If we define household gearing as simply household debt divided by household assets, then for the 10 years prior to COVID average gearing was relatively constant at 20% across all households. By income level, the level of gearing was also relatively stable over that 10-year period. Lower income households clearly have much lower levels of assets, but relative to the level of debt the gearing ratio of the lowest quintile averaged 23% which was the same as the gearing ratio of the highest income earners. Remarkably, since the start of COVID, the gearing ratio for all income levels fell by 2-3% by mid-2022. The assets held by lower income households appreciated by a similar rate as the assets held by higher income households, and this asset appreciation exceeded the pace of debt accumulation sufficient to reduce leverage.

Exhibit 7: Household gearing and debt servicing by age bracket

Source: ABS, YarraCM.

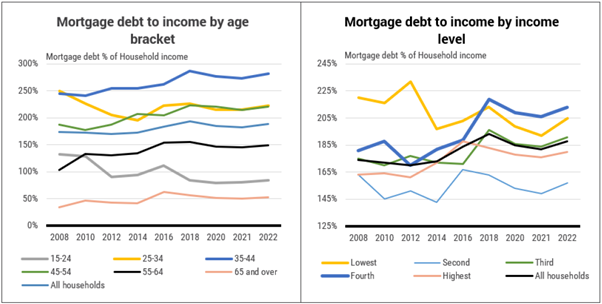

Mortgage debt to household income similarly showed a surprisingly similar improvement, regardless of income level. Before COVID commenced mortgage debt was 193% of household income. In aggregate it had fallen to 188% by mid-2022, and for each income quintile a significant decline in mortgage debt to income was recorded. Indeed, the biggest fall was for the lowest income earners. The bottom income quintile saw a 8% decline and the second income quintile saw a 6% decline. This compares to a 3% decline for the highest income earners, reinforcing the conclusion that the boost to household income via fiscal transfers skewed to lower income households.

In terms of the cost of servicing household debt, there was again little variation across income levels. In aggregate, interest payments to income declined 2.4% to 4.0% and there was little variation in this improvement across income levels.

Exhibit 8: Mortgage debt to income ratios by age and income level

Source: ABS, YarraCM.

In short, there is scant evidence that the distribution of wealth gains, debt accumulation or debt servicing altered materially since 2020. If anything, there was some modest improvement for lower income households.

While this presents as a good news story, it’s important to remember the context in which this stability in household balance sheets occurred. As noted, Federal fiscal stimulus amounted to $250bn or 11.6% of GDP. Combined with State stimulus programs this figure climbs to 13% of GDP. From the monetary policy perspective, 65 bps of interest rate cuts operated in concert with a $440bn expansion in the RBA’s balance sheet (32% of GDP), $188bn of three-year funding for banks under the Term Funding Facility provided bargain funding costs of just 0.25% p.a. for the banks, and the adoption of very long-run forward guidance that interest rates would remain unchanged until at least 2024. All this helped unleash a 25% rise in owner-occupied debt and a 35% rise in average house prices.

There is no historical parallel for this type of monetary and fiscal stimuli, particularly given it was being deployed into a restricted labour supply market and impaired global supply chains. The result was a strong V-shaped economic recovery, a tight labour market and rapid price and asset inflation. Simply put, these are not the conditions that would drive impairment of household balance sheets and financial stress.

The question that matters now is what happens as the impact of the fiscal stimuli fades, monetary conditions turn restrictive, asset prices decline, and job security comes under threat? These are the conditions that will result in a jump in impairments, financial stress and inequality. But what is the best way to isolate who are the most vulnerable sections of society?

This is really going hurt – some a lot more than others.

In our December piece on discretionary cashflow we focussed on the impact at the aggregate level and a key conclusion was:

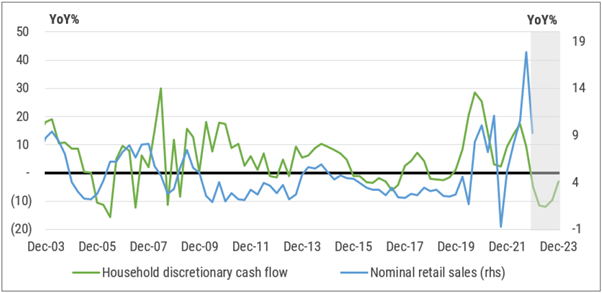

“Even if we assume the ongoing robust growth in wages and employment in 2023, the impost of higher interest costs, utility costs, insurance costs and rents will be sufficient to see average discretionary cashflow fall by 15% by mid-2023, and much more for young households with large families and large mortgages. Given, retail sales growth normally closely tracks our measure of discretionary cashflow, the inference is that retail sales will slow from the rapid rate of close to 20%(y/y) to zero growth by mid-23. Note, this is likely the best-case scenario. It could easily be worse if sub-trend economic growth reveals labour market weakness with a lag, as observable in all prior downturns.”

The chart we used in our December piece is replicated in Exhibit 9, updated for the retail sales data. While it is true that utility futures have eased appreciably over recent months, this assists with future household cashflow only at the margin. The broad story remains unchanged from our December analysis, that the impact upon retail sales growth from the squeeze on household discretionary income is only in its initial phase. We continue to maintain that the threat to retail sales is large, is real, and is already starting to appear in retail sales data and company updates.

Exhibit 9: The crush on retail sales from discretionary income declines is only just beginning

Source: ABS, YarraCM.

However, when we replicate our cashflow analysis by income and by age bracket, it’s very clear that the next 12 months is going to be an incredibly difficult period for many households. Recall that we are assuming in this analysis that employee compensation increases a very robust 7% in 2023. The impact of high food, rent, and utility costs are all significant in exerting pain on household cashflow, yet the bulk of the damage is being inflicted by the RBA’s rate hiking schedule.

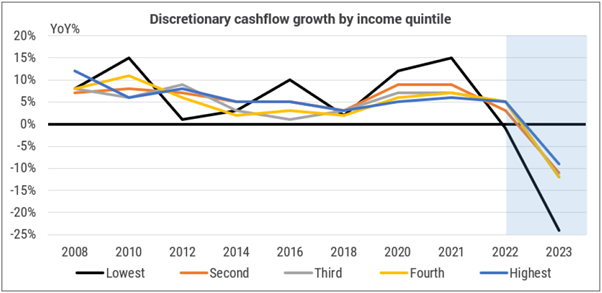

Exhibit 10 highlights just how much of the burden of the RBA’s fight against inflation is being placed on lower income households. Low income earners have very little discretionary income available at the best of times, and while it’s true that they hold a relatively small share (9%) of total household debt, they are as heavily geared as any income quintile. That is, they are even more vulnerable to rising interest rates purely from a debt servicing perspective, let alone the fact that food, rent and utilities take up a large share of their income and from the perspective that they have little other by way of assets or financial buffers. Discretionary cashflow for the bottom 20% of income earners will fall around 24% in 2023. Loss of work hours, unemployment, or illness could spell disaster for any of the 1.7mn households in this category. Notably, higher income levels are also vulnerable to a fall in discretionary cashflow. The more that income increases, the less binding is the constraint from the rising cost of non-discretionary items such as food, rent, insurance and utility costs. However, at higher income levels, corresponding high levels of debt make interest costs a proportionately greater constraint.

Exhibit 10: Low-income households will likely see discretionary income decline 24% in 2023

Source: ABS, YarraCM.

Nevertheless, the top 20% of income earners are still more likely to show greater resilience. Not only does this group have a much higher share of income available after interest, tax and essential consumption expenditure is deducted, they also own 40% of bank deposits, 40% of housing wealth and 66% of shareholdings. While we estimate that their discretionary income will also decline in 2023, they have greater capacity to smooth consumption by running down savings and selling assets.

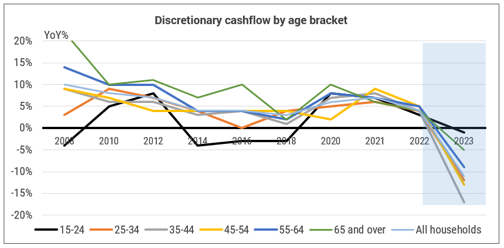

When we repeat the analysis by age group, what immediately stands out is that the party at the 35-44yo’s house is not only over, but a massive hangover is on the way. Low savings, relatively low net equity and expensive consumption tastes suggests that discretionary cash flow for our aging Millennials is set to fall close to 20% in 2023 (refer Exhibit 11). The age bracket will clearly fare worse, although few age-brackets will escape the pain. We estimate that over 9mn households will see their discretionary cashflow decline in 2023. Households aged 65 and over should see much smaller contractions, while the very young households who are relatively debt free should benefit more from rising wages relative to other age groups.

Exhibit 11: The hangover will be largest for the 35-44 year olds

Source: ABS, YarraCM.

Conclusion: Focus less on the size of the buffer. Focus more on the trajectory of cashflow.

There are five key conclusions from this analysis:

- The distribution of the $260bn in excess saving is remarkably evenly spread across in the income distribution, but by age the excess savings skews heavily to households aged above 45yo;

- Of the $260bn in excess saving, or $26k per household, we estimate that $15k can be attributed to being unable to consume items that were restricted/unavailable during COVID – ‘deficit consumption’ – and $11k per household can be attributed to ‘precautionary saving’;

- Of the $15k of saving attributed to deficit consumption per household, $5k is due to a reduction in holiday travel, $3k is due to less driving during COVID and $2k is due to less eating out at cafes and restaurants. On the flip-side, households spent $3k above trend, equally spread between alcohol, furnishing and household equipment and sporting goods. When we calculate deficit consumption by age, we find clear evidence that the vast majority of the $11k in precautionary saving was accumulated by households aged over 45. In contrast, that the 35-44yo cohort have no excess saving via deficit consumption, having consumed all of the boost to their income during COVID and we find no evidence that this age group engaged in ‘precautionary saving’ behaviour;

- There is clear evidence from this data that the COVID-era monetary and fiscal stimulus was excessive, yet we find that the stimulus was remarkably ‘fair’ in the sense that the distribution of wealth, gearing and debt servings was mostly unchanged. Yet, we caution that in the absence of the fiscal stimulus, the rapid shift to restrictive monetary settings and more challenging economic and labour market conditions ahead all suggest that conditions where financial vulnerabilities could rapidly become evident are now in place;

- The impact of the shifting fiscal and monetary stance will have sharply different impacts by age group and by income distribution. We estimate that the discretionary cashflow for the bottom 20% of households will plummet 24% in 2023. By age group, this cashflow squeeze looks set to be particularly acute for the 35-44yo cohort.

The RBA Governor declared to Parliament that “nothing keeps him up at night”. But perhaps in the small hours of the morning he should consider that if the bulk of the saving has been done by older households who are now in wealth protection mode, then the ‘excess saving buffer’ that the RBA is so focussed on is not a threat to excess demand growth.

The RBA’s rate hikes already delivered, not to mention an additional 50bps or more that they suddenly seem intent on delivering, are about to unleash enormous financial pain on the lower income and younger households that risks an abrupt stoppage in retail sales and potentially a sharp jump in the unemployment rate and a raft of delinquencies.

Further tightening could perhaps be justified if there were signs of ongoing supply side restrictions, excess demand growth and unanchored inflation expectations. But from the RBA’s own analysis, 50-75% of the excess inflation in Australia is due to supply chain disruption which has now been resolved, global inflation peaked months ago, and inflation expectations remain well behaved. Moreover, it is worth noting that in the absence of the RBA hiking rates this cycle, the sharp rise in the cost of essential items was already acting as a ‘tax’ on discretionary income. We estimate that discretionary cashflow growth would have slowed to zero in 2023 in the absence of the RBA rate hikes. The 325bps of hikes implemented to date, plus an estimated 50bps more to come in coming months, are the sole reason why cashflow contracts so sharply in 2023.

In our view, the RBA is focussed on trying to re-establish its reputation as an inflation fighting central bank amid intense scrutiny of its performance by markets, government reviews and by the media. There have been some well documented missteps by the Bank over recent years including:

- Failing to see the V-shaped economic recovery;

- Failing to identify rising global inflation pressures;

- Suggesting Australia was a special case and unlikely to see the same inflation pressures as offshore;

- Excessive deployment of QE even after the economic recovery had commenced;

- Misjudging the reputational damage that was likely to result from long dated calendar based forward guidance; and

- A clumsy exit from yield curve targeting and various communication gaffes.

In our opinion, though, the biggest error thus far was to jettison forward looking inflation targeting and the adoption of backward-looking inflation targeting which unfortunately is a practice that still appears in place. However, all these criticisms will pale by comparison if the RBA merely buries poorer and younger households based on a flawed assessment of ‘excess savings’ long after the inflation battle has already been won.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

Tim Toohey is Head of Macro and Strategy at Yarra Capital Management. All prices and analysis as at 7 March 2023. This information was produced by Tim Toohey and published by Livewire Markets (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.