Don’t abandon fixed income ETFs

Fixed-interest investments are typically regarded as “defensive” investments. Investors look to them to provide portfolio diversification when equity markets are volatile. However, this narrative has not really played out as one might expect, depending on the time frame used for analysis. But is now the time to abandon these investments?

Why the selloff in (some) fixed-interest markets?

After more than a decade of declining interest rates (at least in Australia), inflation has reared its head— threatening global economic stability. Policymakers are responding to this threat with a flurry of interest-rate hikes—with potentially more to follow. upward move in government-bond yields has caused a lot of pain for investors in “interest-rate-sensitive” strategies.

Interest-rate sensitivity

In fixed-interest markets, when bonds offer a fixed coupon and yields increase, bond prices decrease. Investors who bought long-term bonds that are not due to be repaid for many years (long-duration assets) have been hurt more by this increase in bond yields than have investors who hold shorter-duration assets. Why? These long-duration assets are more sensitive to changes in interest rates. That is, a higher duration results in a larger fluctuation in the bond price per unit change in the interest rate. This sensitivity works both ways— when interest rates are decreasing, longer-duration assets fare better than shorter-duration assets.

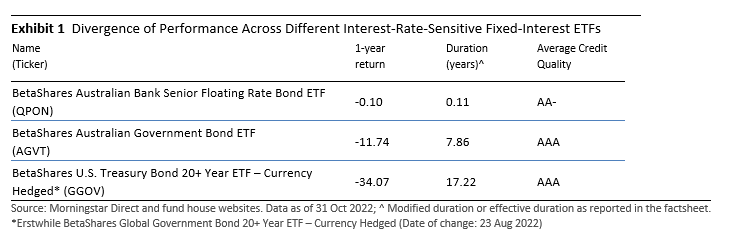

As seen in Exhibit 1, the BetaShares U.S. Treasury Bond 20+ Year ETF – Currency Hedged (erstwhile BetaShares Global Government Bond 20+ Year ETF – Currency Hedged) has a long duration of almost 18.0 years and has suffered much more than the BetaShares Australian Composite Bond ETF (medium duration—that is, eight years) in a rising interest-rate environment over the past year. Meanwhile, the BetaShares Australian Bank Senior Floating Rate Bond ETF, with a very short duration of less than 1.0 year, is less sensitive to rising interest rates and has fared reasonably well.

While interest-rate-sensitive assets and duration have been the main stories in 2022, the underlying credit quality of your fixed-interest investment cannot be ignored. In a recessionary environment, default rates (borrowers not repaying their debts in part or in full) often increase. And if credit quality is low, investors face the risk that they won’t be repaid. So, while we focus on interest-rate-sensitive investments here, fixed-interest funds of low credit quality could be tomorrow’s story. And it is worth keeping an eye on the credit quality of your fixed-interest portfolio.

What interest-rate-sensitive fixed-interest assets does Morningstar rate?

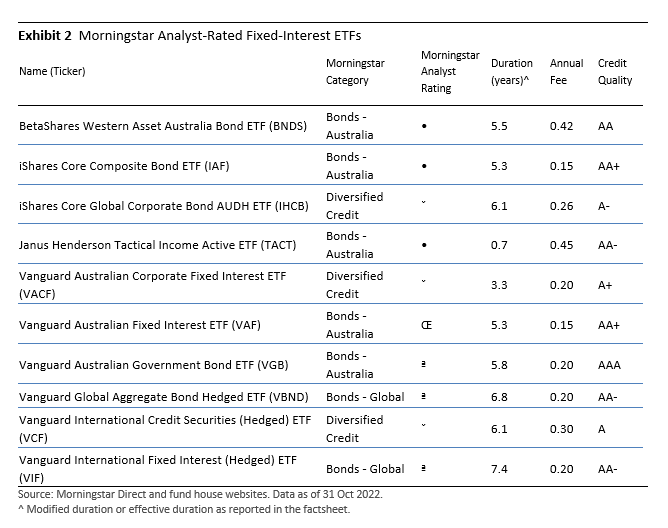

The following table lists the various interest-rate-sensitive fixed-interest exchange-traded funds rated by Morningstar:

Our passive ETF picks in the bonds—Australia category

IShares Core Composite Bond ETF IAF and Vanguard Australian Fixed Interest ETF VAF are the top-rated passive ETFs in the category tracking the Bloomberg AusBond Composite 0+Y TR Index. Both with a modified duration of above 5.0 years, investors should be wary that if interest rates continue to rise, more pain will be felt. But if we are close to the top of the interest-rate-hiking cycle, these well-priced passive ETFs could provide the portfolio diversification characteristics of yesteryear.

VAF is considered to be one of the best choices in the category. It employs a thoughtful approach of optimized sampling to meet the index’s risk/reward characteristics. We view this approach as highly efficient for mitigating liquidity risk and keeping transaction costs low.

In the same vein, IAF provides cheap access to a well-managed bond portfolio that is complemented by iShares’ indexing abilities. The portfolio management team has reliably replicated the underlying index with minimal tracking error.

Our active ETF picks in the bonds – Australia category

On the active side, BetaShares Western Asset Australian Bond ETF BNDS is a compelling choice for domestic fixed-interest exposure owing to its best-in-class team and straightforward approach. The plus or minus one-year duration range keeps the portfolio’s active duration reasonably close to the index but, unlike its passive peers, provides some maneuverability. For example, the portfolio’s active duration was moved around judiciously and contributed strongly in 2021, a testament to the team’s ability to interpret and capitalise on shifting economic conditions.

Listed on the Chi-X, Janus Henderson Tactical Income Active ETF TACT is another appealing pick from the active cohort. The strategy maintains a low duration profile and hence low interest-rate risk relative to a typical Australian bond offering. Benchmarked against a 50/50 split of the Bloomberg AusBond Bank Bill Index and Bloomberg AusBond Composite 0+ Yr Index, the fund aims to generate alpha by identifying opportunities in macro conditions and by tapping into credit. The flexible approach is solidly backed by an experienced and skilled portfolio management team.

Should I abandon interest-rate-sensitive fixed-interest funds?

Despite a torrid year, interest-rate-sensitive fixed-interest funds still have a role to play in portfolios. If inflation fears abate and a recession looms, policymakers may well reverse their current interest-rate-hiking stance and decide to cut interest rates. If this happens, there’s a good chance that interest-rate-sensitive fixed-interest funds with a high credit quality could provide investors a very useful source of portfolio diversification. That is, we might see yields come down and prices go up—hopefully offsetting expected portfolio losses from equities in such a scenario. Also, these investments are now paying a much higher yield than they were 12 months ago. So, investors are now being better compensated than in recent history to hold these funds. While the sea of red is a lot to stomach, in a more normalised environment, interest-rate-sensitive fixed-interest funds still have a role to play in investor portfolios.

First published on the Firstlinks Newsletter. A free subscription for nabtrade clients is available here.

Annika Bradley is Director, Manager Research Ratings at Morningstar and Zunjar Sanzgiri is Senior Analyst, Manager Research at Morningstar. Analysis as at 28 November 2022. This information has been provided by Firstlinks, a publication of Morningstar Australasia (ABN: 95 090 665 544, AFSL 240892), for WealthHub Securities Ltd ABN 83 089 718 249 AFSL No. 230704 (WealthHub Securities, we), a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 (NAB). Whilst all reasonable care has been taken by WealthHub Securities in reviewing this material, this content does not represent the view or opinions of WealthHub Securities. Any statements as to past performance do not represent future performance. Any advice contained in the Information has been prepared by WealthHub Securities without taking into account your objectives, financial situation or needs. Before acting on any such advice, we recommend that you consider whether it is appropriate for your circumstances.