Hacks fuel fear as markets count weather costs

S&P/ASX200 - Domestic market

It was a rough start to the week as the Australian market finally got to respond to the previous Fridays 403.89 point, or 1.34%, Dow Jones Industrial Average meltdown in the United States. The local market went a stretch further with the S&P/ASX200 plunging 1.4% to 6664.40 by the close of Monday.

It pushed the year-to-date fall for the index to 10.48%, but some clawbacks as the week progressed saw the index down 9.59% by Thursday’s close.

We are at that part of the cycle where stocks are punished when they disappoint. Building materials company Adbri (ABC) dived 21% to $1.45 following the release of an inflation and weather impacted trading update and the surprise departure of its chief executive. It had climbed back to $1.50 by Thursday’s close.

Horticultural company Costa Holdings (CGC) was also punished as its shares dropped 13.43% to $2.00 following Monday’s trading update that full year earnings would be “considerably lower” than it had previously advised, due to the impact of adverse weather conditions on its citrus fruit operations. It had recovered to $2.23 by Thursday’s close but volumes were low, and the stock remains in a bearish trend with its shares below a declining 200-day moving average.

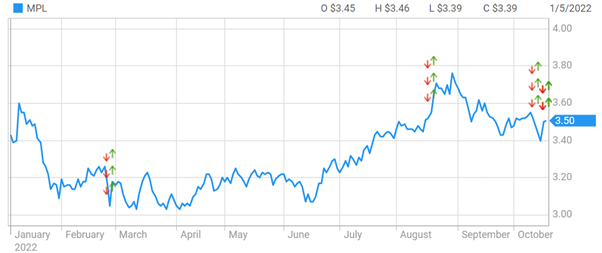

An evolving story during the week was the Medicare Private (MPL) data breach. Last week when the issue first emerged it was reported the healthcare company had caught the data hack before customer details were captured. That turned out to be false, and on Thursday Medicare revealed it had been provided with a sample of customer data by the hackers, including client’s names, addresses, birth dates and phone numbers. There is also an unverified claim the breach included credit card information. Medibank went into a trading halt “until further notice” on Wednesday.

The breach follows the recent Optus data breach, the largest in Australia’s history, and data hacks have also been reported by online wine seller Vinomofo and Woolworths’ MyDeal website.

As Optus is not listed, it will be interesting to see how the market responds to the Medibank breach once trading resumes

Source: nabtrade

International markets

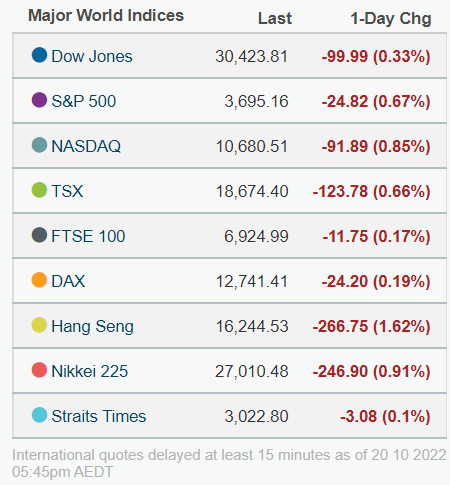

Internationally there are few bright spots to suggest the Australian market will end the week positively.

Although the UK’s U-turn on proposed tax cuts created upward European momentum during the week, as of last night ongoing economic uncertainty, recession fears and problematic inflation had European markets indicating a negative opening following falls the previous day.

Source: nabtrade

Fears of a recession and rapid-fire US Federal Reserve interest rates hikes have helped push US markets to yearly lows in recent weeks. Fears of a recession remain a topical conversation point but the current earnings cycle has thrown up some bright spots.

During the week Tesla CEO Elon Musk said it was “pedal to the metal” recession or not. Although the stock has lost 45% of its value this year its adjusted earnings of US$1.05 a share beat analysts’ median expectations of US99c a share.

Enterprise software and consulting company IBM jumped 6% on Wednesday after beating analysts third quarter earnings expectations. It also lifted full year growth forecasts. Reported revenue at US$14.11 billion compared with analysts forecast US$13.51 billion, according to Refinitiv.

Limited US economic data out next week will provide few global market leads, but ongoing blue chip earnings reports will be monitored closely.

Resources

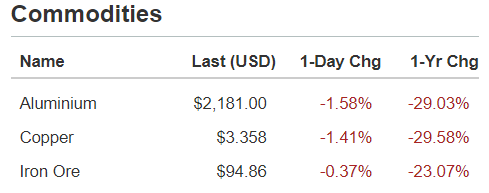

In the materials space there is little cheer as recession fears slash economic growth forecasts.

Source: nabtrade

BHP (BHP) has been under selling pressure from traders recently and its Thursday close of $38.35 is up from last month low of $35.56 but still a chunk below the $40.00+ the resources giant has traded at through most of the year.

Rio Tinto’s (RIO) share price slump has been similar to BHP’s, and since July the iron ore giant has been trading below $100 a share. It closed Thursday at $92.26

Source: nabtrade

Energy and resources companies topped the gains made on Thursday

Battery materials maker Novonix (NVX) climbed 7.04% to $2.28 on high trade volumes after an announcement it was in negotiations with the US Department of Energy for a $US150 million grant. Gas producer Woodside Energy Group (WDS) jumped 6.16% to close at $34.56 following the release of its September quarterly report revealing a doubling of both production and the realised price for liquified natural gas (LNG). While nickel miner Chalice Mining (CHN) sneaked into the top three performing stocks of the day with a 4.08% increase in its share price following positive exploration results on Wednesday from its nickel-copper-platinum project in Western Australia.

Analysis as at 20 October 2022. This information has been provided by WealthHub Securities Ltd the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 (NAB). Whilst all reasonable care has been taken by WealthHub Securities in reviewing this material, this content does not represent the view or opinions of WealthHub Securities. Any statements as to past performance do not represent future performance. Any advice contained in the Information has been prepared by WealthHub Securities without taking into account your objectives, financial situation or needs. Before acting on any such advice, we recommend that you consider whether it is appropriate for your circumstances.