Can we learn anything from the short sellers?

Love them or loathe them, short sellers are here to stay. Theoretically, at least, they add stability and reduce volatility because they can be “buyers” when others dare not (reducing sudden dips down), and “sellers” when everyone else is stampeding to buy, which helps to cap sharp swings up. The academic research largely supports the proposition that short selling is a net positive for the market – and that’s why ASIC allows it in Australia.

Of course, short selling is selling something that you don’t own. A short seller profits from a falling price – selling at a higher price first, and then buying back at a lower price. It is the exact opposite of normal trading: buying first at a lower price to sell out at a higher price.

To short sell a stock, something that you do not own, you need to be able to “borrow” the stock to make the delivery on the ASX. This is where the major fund managers and large superannuation funds come in – they lend the stock to the short sellers. In return, the short seller secures the loan by giving the super fund cash. When the short seller closes the position on the ASX by buying the stock back, he/she returns the stock to the super fund and gets their cash back. The super fund gets paid for lending the stock by taking a margin on the cash.

Not all big super funds lend stock – but many do, so if you don’t like short selling, join a campaign to tell the super fund to stop. They will argue that they are boosting the returns for their members.

But let’s move on from the debate about whether short selling is good or bad and look at what we can learn from their actions. Firstly, it is useful to reflect on the “types” of short selling.

Broadly, there are four “types”.

The first type is just a simple outright short sale – “company ABC is a dog of a company” – so the short seller sells ABC.

Secondly, the relative short sale. This involves being “long” one company from an industry sector and being “short” another company in the same sector. Essentially, the short seller is saying that company A will do better than company B. Examples could be buy Woolworths and sell Coles; buy Fortescue and sell Rio; buy QBE and sell IAG; or buy CBA and sell ANZ etc. By being long one stock and short the other, the short seller is not taking market or industry risk, just relative performance risk.

The third type is a sector position, where companies from a particular industry or sector are sold because the short seller thinks that there are significant headwinds, or they are over-hyped and over-priced.

The final type, which some argue is “good” short selling, relates to market makers and other professionals hedging derivative positions such as exchange traded options and warrants, or catering for settlement mismatches. Occasionally, a short seller may arbitrage the futures markets, resulting in widespread short sales of physical stocks.

Short sellers are required to report details of positions opened to ASIC, who then collate the data and publish a daily report. The sellers aren’t required to report the reason for taking the position out, so in reviewing the data, what we look for are unusual positions and how they are changing. This is further complicated by the reality that most stocks have some level of open short positions, so again, we need to be careful in rushing to judgement.

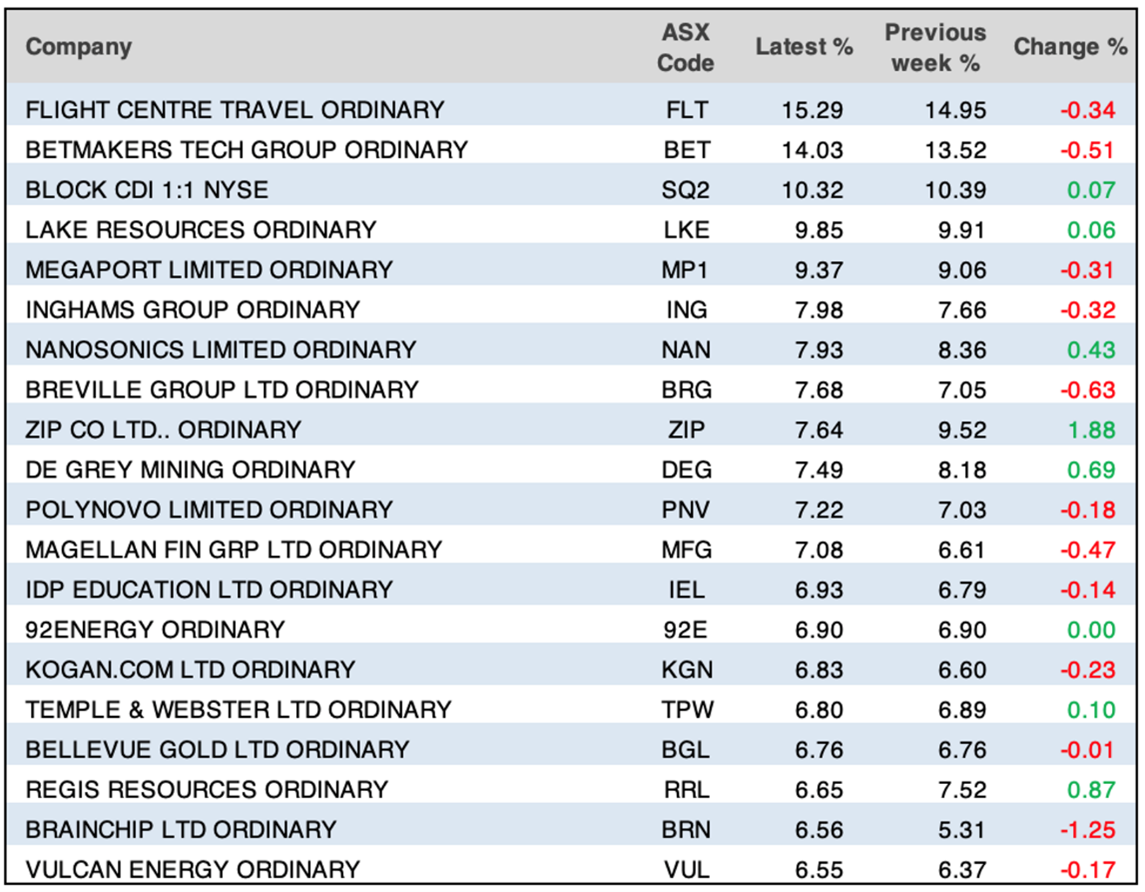

Listed below is the table of the twenty most shorted stocks as of 23 September. We compiled this list from the ASIC data and published it in last Saturday’s Switzer Report.

Flight Centre is the most shorted stock based on the percentage of its share sold short. As of Friday, 15.29% of its ordinary shares, or 30.5 million shares out of a total base of 200 million shares, had been sold short.

Magellan Financial Group, MFG, which has 184 million shares on issue, had 13 million shares short sold. This gave it a ranking as the twelfth-highest shorted stock at 7.08%.

In contrast, BHP came in 342nd place, with 21 million shares short sold out of a base of 5.06bn ordinary shares (0.42%).

20 Most Shorted Stocks – as of 23 September 2022

The table also shows the change over the week. A “green” or positive change means that net short positions were closed, and a “red” or “negative” change means that net short positions were opened. So last week, short sellers opened positions in Breville (BRG) – it recorded an increase of 0.63% as short positions went from 7.05% to 7.68%, while short positions were closed by 1.88% in Zip.

What can we learn from the short sellers?

Here are some current observations:

- Two industries that remain out of favour are travel and betting. (An alternative hypothesis is that they are fully priced). Flight Centre (1st) and Webjet (23rd with 5.99%) have material short positions. In the second category are Betmakers (2nd) and Pointsbet (30th with 5.49% short sold);

- Retailers, particularly online retailers, are out of favour. Kogan.com and Temple & Webster both have almost 7% short sold. JB Hi-Fi is in 29th position with 5.49%;

- The short sellers are still short payment companies, which have typically fallen by over 70% in 2022. Block is in 3rd position, Zip is in 9th position, Humm is in 49th position with 4.23% and EML Payments is in 62nd position at 3.64%. That said, the short position in EML payments is down considerably from its peak;

- Stocks that are exposed to consumers tightening their belts feature prominently;

- Fans of Megaport (MP1) should be wary of the short selling interest in the stock; and

- There are no material short positions in the major banks. ANZ at 0.51% is ranked 315th, CBA at 1.33% is ranked 181st, NAB at 0.89% is ranked 230th and Westpac at 1.28% is ranked 187th. However, the positions in regional banks with BOQ at 5.92% (25th) and Bendigo (BEN) at 3.32% (70th) are higher. While I don’t think you can conclude that short sellers are long the major banks and short the regional banks, there is a wariness about the regional banks.

The short sellers don’t always get it right. But they are investment professionals, so you would expect them to get it right more often than they get it wrong. Knowing how they are positioned can be an important data input into investment decisions.

All prices and analysis at 26 September 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.