Investment markets & key developments: Central bankers remain hawkish

From their June lows, global and Australian equities have run hard and are vulnerable to a pullback over the next few months.

More fundamentally:

- Central banks are still a way off from peaking and actually cutting rates; recession risk is still rising (as evident in the inverting US yield curve);

- This runs the risk of significant earnings downgrades;

- The August to October period is seasonally weak for shares; and

- Geopolitical risk is still on the rise with the escalation in China/US tensions over Taiwan, ongoing war in Ukraine and the upcoming US mid-terms.

On the positive side of the equation:

Increasing signs of a peak in US inflation;

20% or so falls in share markets possibly having already anticipated a mild recession; and

The strength of the rebound itself maintains the possibility that we may have seen the bear market low and that any pullback may just be a partial retracement of the rally since mid-June which then bottoms out above the June low and sees the rising trend continue.

Time will tell. On a 12-month view, shares are likely to be stronger as central banks stop hiking rates and recession outcomes decrease. But short-term uncertainty is very high and the risks are on the downside.

Inflation and recession risk remain the main issues for investment markets. In the past week:

- Chinese economic data surprised on the downside and US data were mostly soft further keeping recession risk high.

- The Reserve Bank of New Zealand hiked its cash rate by another 0.5% to 3% and sounded even more hawkish. Norway’s central bank also hiked by 0.5%.

- Further increases in inflation in the UK and Canada left both countries' central banks on track for more rate hikes.

- The minutes from the last Fed meeting remained hawkish, foreshadowing more rate hikes ahead with no signs of an imminent “pivot” to easier policy, but signalled awareness of the risk to growth and the need for an eventual slowing in monetary tightening as policy moves into restrictive territory to avoid over-tightening.

- Similarly, the minutes from the last RBA meeting continued to flag more hikes but reiterated that it's “not on a pre-set path”. It also appears more conscious of the downside risk to growth including for households.

- Australian data didn’t provide a firm lead on what the RBA will do at its September meeting – unemployment fell to a new 38-year low of 3.4% but employment also fell (likely due to the impact of covid and flu illnesses and floods) and while wages growth is picking up it’s a long way from a wage-price spiral.

While we lean to the RBA hiking by another 0.5% next month, we think it’s a close call as to whether they hike by 0.25%. Given the lags involved in how monetary policy impacts the economy – many households have not seen the full impact of the rate hikes so far and the fixed rate cliff is yet to impact mostly next year – and the huge blow to real wages, it makes sense for the RBA to slow the pace of tightening to give time to assess the impact of the rate hikes so far.

With medium-term inflation expectations remaining low the RBA now has some scope to slow down. Moving by 0.4% might be a good compromise (and return the cash rate to a more “normal” number). The futures market is currently pricing in a 0.38% hike in September. We still see the peak in the cash rate being 2.6% later this year or early next.

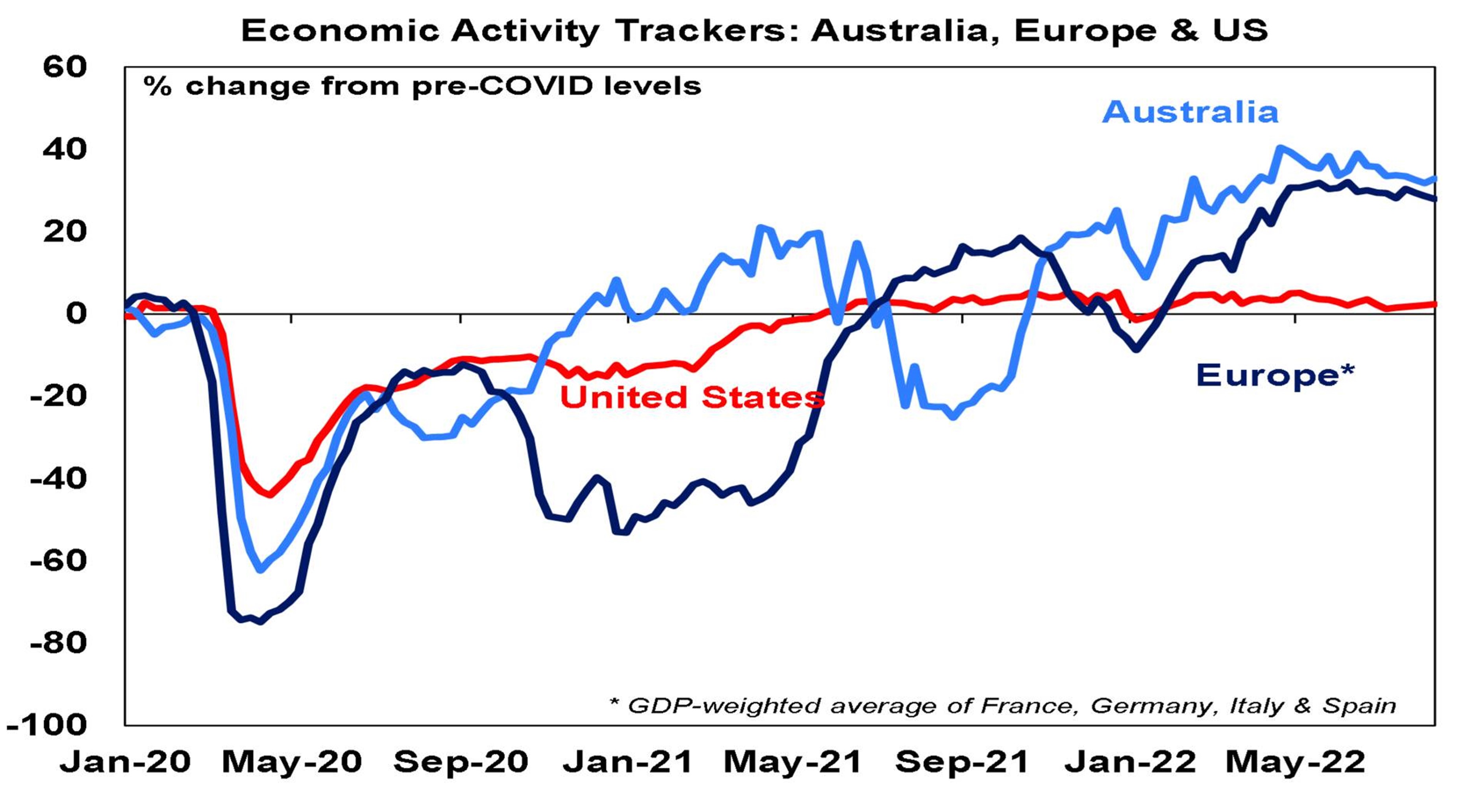

Economic activity trackers

Our Australian Economic Activity Tracker fell again over the last week and continues the loss of momentum seen since April, consistent with a slowdown in growth. Our US Tracker rose slightly and our European Tracker fell slightly.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Australian economic events and implications

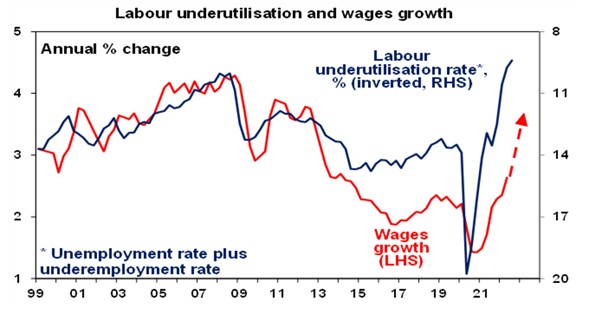

We continue to expect a pick-up in wages growth going forward as:

- Labour underutilisation is at levels consistent with 3-4% wages growth;

- Wages growth including bonuses rose to 3.1%yoy which is the highest since 2013;

- Private sector jobs experiencing a rise saw a 3.8% average gain which is up from 2.7% a year ago but it always takes time for this to flow through given multiyear EBA’s;

- The 4.6% and 5.2% minimum wage increases will push wages up from the current quarter; and

- Numerous surveys and anecdotes point to faster wages growth ahead.

As a result, we see wages growth picking up into the 3’s over the next year. This will still be well below the sort of wages growth being seen already in the US and Europe suggesting a wage-price spiral is a far smaller risk in Australia, meaning the RBA won’t have to raise rates as much as the Fed.

Source: ABS, AMP

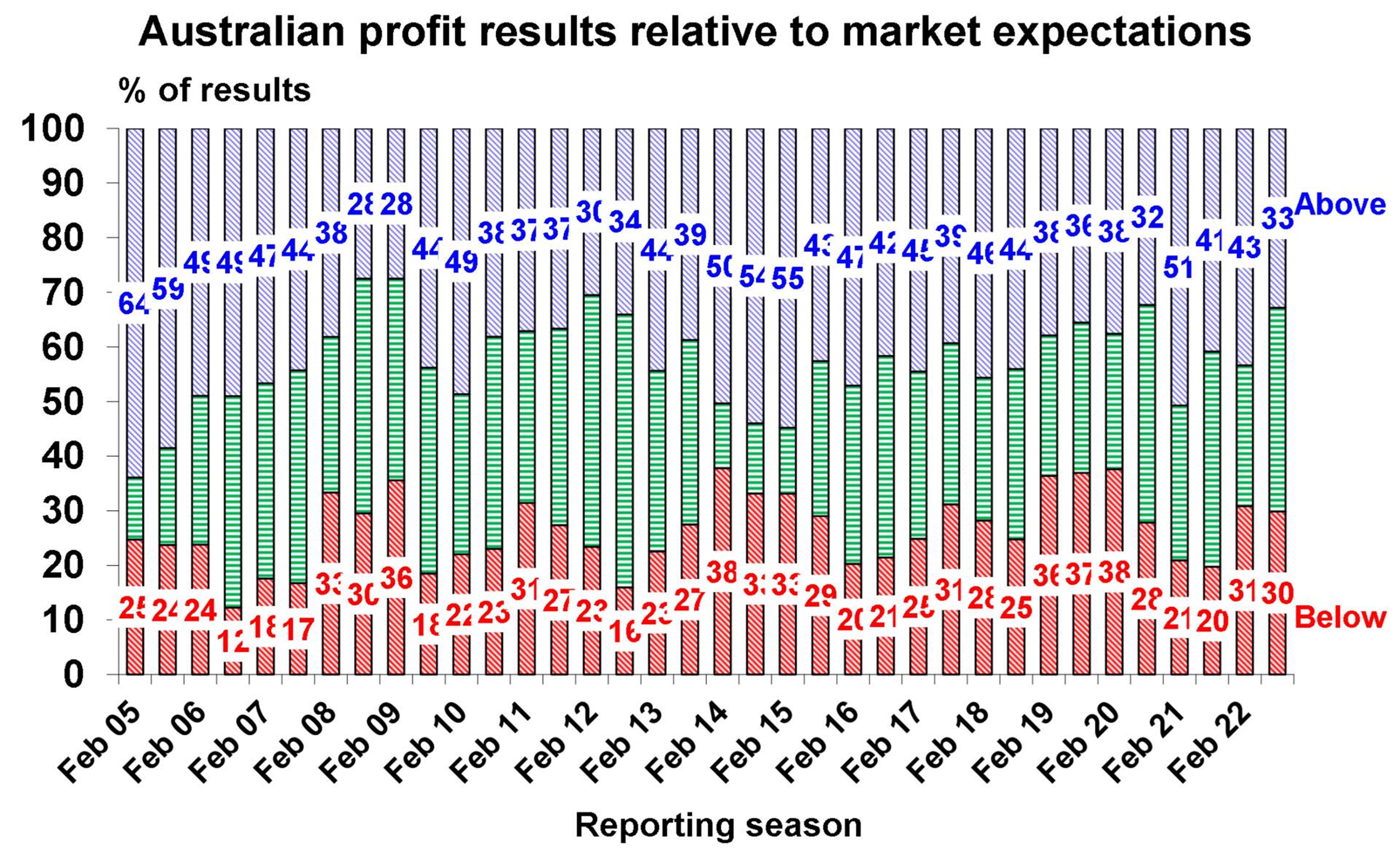

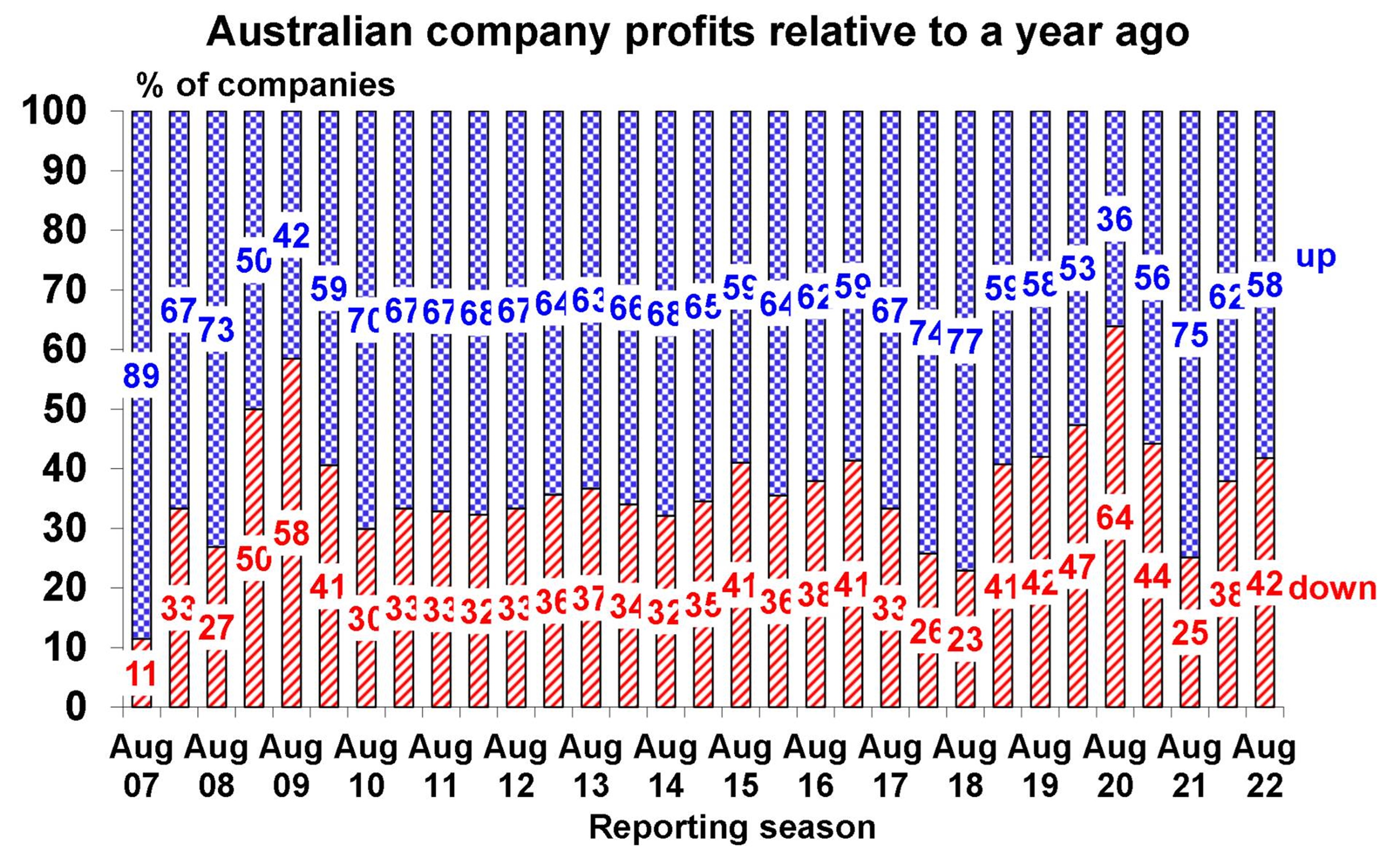

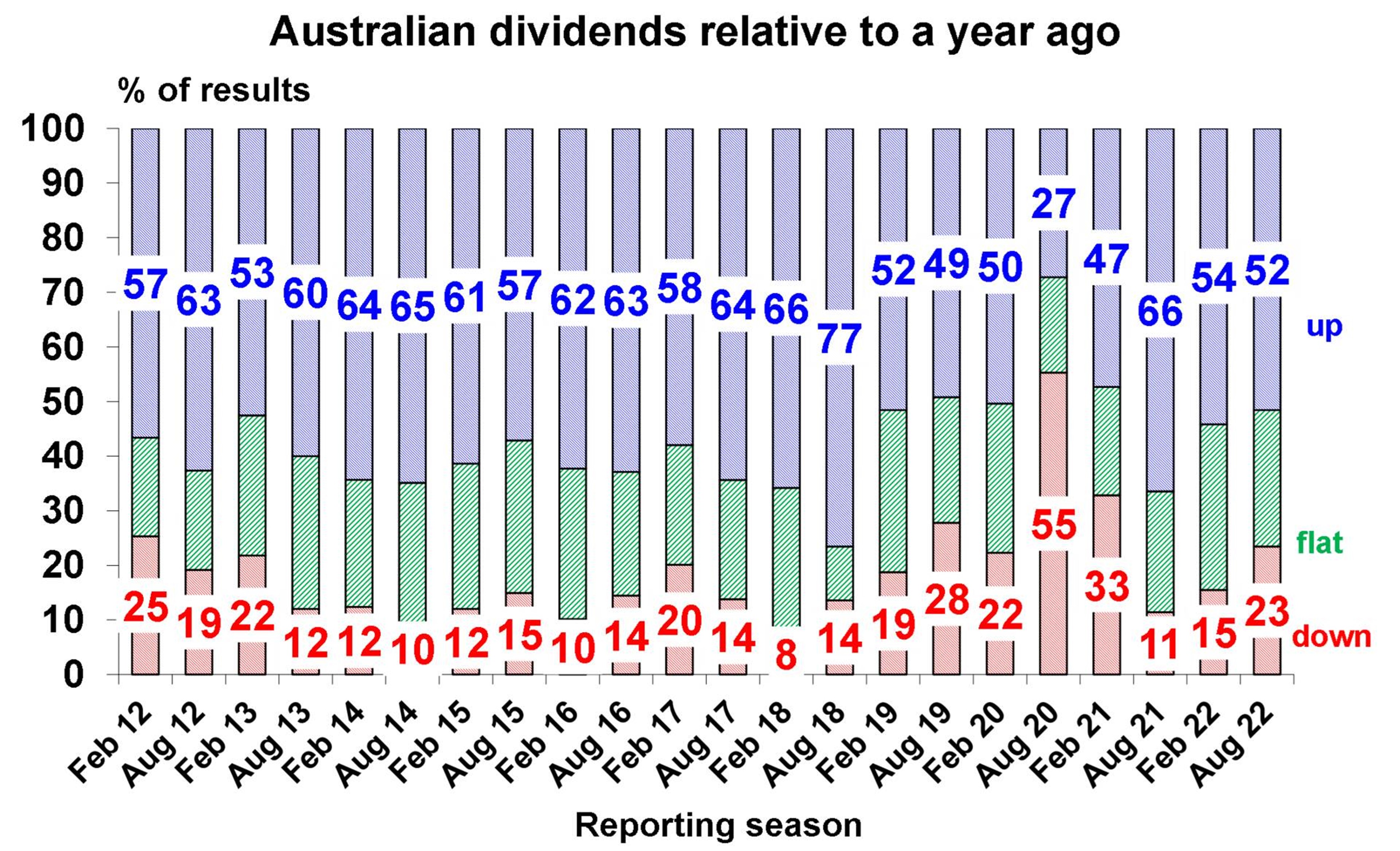

The Australian June half earnings reporting season has now seen about 65% of company profits by market capitalisation report. Overall results are a bit soft, and they have slowed down since the initial recovery from the pandemic lockdowns.

So far only 33% of results have surprised on the upside, 58% have seen earnings up on a year ago and 52% have increased dividends, all of which are below average reflecting the cost pressures some businesses are facing. Reflecting this, only 45% of companies saw their share prices outperform the market on the day results were released which is well below the norm of 54%. A significant proportion of companies have flagged earnings growth this year below inflation.

Source: AMP

Source: AMP

What to watch over the next week?

Business conditions PMIs for August for the US, Europe, Japan and Australia will be released on Tuesday and will likely show further signs of a slowdown. Hopefully, pricing pressures, supplier delivery lags and work backlogs with have improved further adding to signs of a peak in inflation pressure.

The annual central bankers’ gathering in Jackson Hole, Wyoming (Thursday to Saturday) where the topic is 'Reassessing Constraints on the Economy and Policy' will be watched closely for any change in direction regarding global monetary policy – but its likely central bankers, including Fed Chair Powell, will remain hawkish in dealing with inflation albeit with a bit of caution creeping in given the emerging economic downturn.

In the US, core private final consumption deflator inflation for August (Friday) will likely show a 0.3%mom rise with annual inflation remaining unchanged at 4.8%yoy adding to signs that inflation may have peaked. Personal spending and income are likely to show continued modest growth. Durable goods orders for July (Wednesday) will likely show a further rise and home sales data (Tuesday and Wednesday) is likely to remain soft.

The June half Australian earnings reporting season will hit its busiest week with about 100 major companies due to report. Consensus expectations are for about 20% earnings growth for the 2021-22 financial year with this boosted by energy earnings (+275%) and industrials averaging about 9.5% growth. The focus will likely be on outlook statements given cost pressures, labour shortages and slowing consumer demand.

All prices and analysis at 22 August 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.