Three ETFs for defensive investing

An occupational hazard of writing weekly share market columns is a constant demand for money-making ideas. But sometimes the best ideas are about protecting money.

Preserving capital is the key to investing in any conditions. Investors who ride out the big downturns – without losing a chunk of their wealth – live to fight another day. They benefit from an equities market that historically rises over time.

Yet I’ve seen too many investors over the years “buy the dip” in bear markets, only to destroy even more capital. They don’t realise how far – or for how long – sectors can fall when they lose favour. The tech bear market still has further to go, for example.

I have an uneasy feeling about the Australian equities market. The size and pace of the Reserve Bank’s rate-tightening cycle is madness. It’s too much, too soon. Sadly, some consumers will be crushed under rising mortgage repayments, food and petrol prices.

Waning consumer confidence and easing demand will trigger earnings downgrades from listed companies. I suspect more companies during the reporting season in August will issue gloomy outlook statements or downgrade their earnings guidance.

I could be wrong, but the odds favour further market falls. Or at least a more volatile difficult market for this year and next. If consumers are hurting now, what happens when the cash rate is above 2% in FY23?

Yes, the market looks forward and there’s a chance that the RBA won’t have to lift rates by as much as expected to tame inflation. But with the US probably already in recession, it’s hard to see how Australia can escape the economic carnage overseas.

How to respond

Investors should respond in four ways:

- First, beware of speculative stocks in this market. Loss-making companies that need to raise equity capital to survive will struggle. There are always exceptions, but this is no market for speculating on the “next big thing”.

- Second, consider cash and fixed-income allocations in portfolios. Cash is always most valuable when nobody has it – and when other asset classes are tumbling, as most have this year-to-date. Near-zero returns on cash investments looked awful last year; now they look relatively attractive compared to equity-market returns this year. As interest rates rise, cash and some bonds will become more attractive. Today, I can get a 4% trailing yield from Commonwealth Bank shares (before franking). Or 3.65% in a two-year term deposit from AMP that is government guaranteed (under $250,000). If I’m investing for yield – and need that income to live on – the return on risk-free cash compared to volatile equities is starting to look more attractive.

- The third response is defensive equity investing. That is, ensuring the equities component of portfolios has sufficient exposure to quality companies that have pricing power and are in reasonably defensive industries (I focus on three Exchange Traded Funds below to highlight this style of investing).

- Fourth, investors need realistic expectations. If you can get a 5% yield and a few percentage points of capital growth, you’re doing well this year. Even some of the largest superannuation funds are delivering negative annual returns right now.

Aiming for a single-digit portfolio return – and most of all, capital preservation – this year won’t get readers’ pulses racing. But if you can weather what could be a bumpy couple of years, your portfolio will be well placed for an eventual strong recovery.

Here are three ETF ideas that fit my strategy of defensive equity investing:

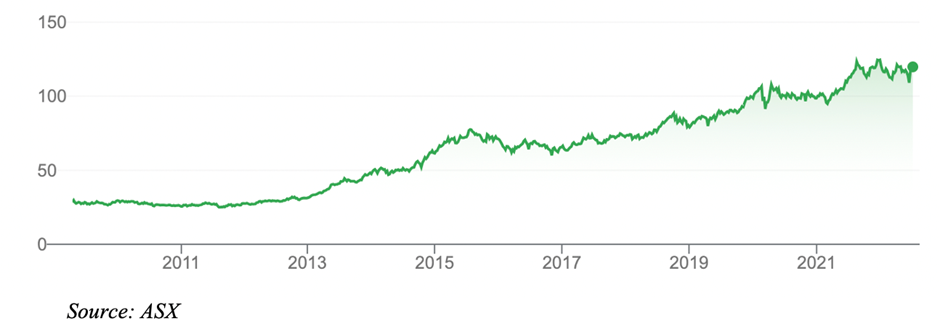

1. iShares Global Consumer Staples ETF (IXI)

Quoted in Australia since 2009, IXI tracks the performance of the S&P/Global 1200 Consumer Staples Sector Index.

By member, the index’s largest holdings are Procter & Gamble, Nestle SA, Coca-Cola, Pepsico, Walmart and Unilever. The index also includes US and UK tobacco stocks, which might deter some investors who don’t want exposure to that industry on Environmental, Social and Governance (ESG) grounds.

By country, IXI has about 56% exposure in the US, 12% in the UK and 9% in Switzerland. Clearly, it’s a play on the world’s largest manufacturers and retailers of everyday household goods. That’s a better place to be when inflation rises and consumers cut back on discretionary ideas, but still need food and beverage staples.

IXI is up 5.3% over one year to end-June 2022. Since its inception, IXI has delivered an average annualised return of 8.3%. Within that have been some large calendar-year returns (about 20%) and some slightly negative years.

IXI is unhedged, meaning an easing Australian dollar relative to the US dollar (which I expect to continue this year) should provide modest return support.

iShares Global Consumer Staples ETF (IXI)

2. VanEck FTSE Global Infrastructure Hedged ETF (IFRA)

Most portfolios should have some exposure to global infrastructure and particularly now as inflation and interest rates take off, and market volatility spikes.

Many core infrastructure companies – think electricity and gas utilities – have inflation-linked revenues. Regulators allow them to pass through higher inflation, and in some cases higher interest costs, to consumers through higher prices.

Chosen well, global infrastructure provides more defensive exposure and takes some volatility out of portfolios. Infrastructure has a lower correlation (relationship) with equities. Wholesale investors who want even less impact from falling equity markets on infrastructure assets should consider unlisted infrastructure funds.

VanEck’s IFRA ETF has attracted good funds inflow this year. It gives investors exposure to 134 of the world’s top infrastructure stocks. Only companies with 65% of their revenue attributable to core infrastructure are included in the index. By sector, half the index is weighted to utilities, making IFRA more defensive.

As a currency-hedged ETF, IFRA eliminates currency risk from the equation. IFRA has returned 8.1% over one year to end-June 2022, Morningstar data shows.

VanEck FTSE Global Infrastructure Hedged ETF (IFRA)

3. iShares Global Healthcare ETF (IXJ)

I have written favourably about this ETF several times for this Report over the past decade. It hasn’t disappointed: the five-year average annualised return is 12.1%.

IXJ has returned 7.72% over one year to end-June 2022. Like IXI in consumer staples, IXJ is down a little this year, but far less than the Australian equities market.

IXJ invests in the world’s largest healthcare companies, about three-quarters of which (by market capitalisation) are in the US. UnitedHealth Group, Johnson & Johnson, Pfizer, Novartis and AstraZeneca are among its top 10 holdings.

I like IXJ for a few reasons. The healthcare sector has good long-term prospects as the global population grows and ages. Healthcare demand is more defensive: people still need medication and healthcare services in good and bad economies.

Also, ASX has a limited choice in large-cap stocks. You have to invest globally to get exposure to the world’s best pharmaceutical companies.

Healthcare exposure should be a portfolio mainstay for long-term investors. Getting it through an ETF that invests in 1200 global healthcare stocks appeals. IXJ is particularly timely as more sectors face waning demand as interest rates rise.

IXJ is unhedged for currency movements.

iShares Global Healthcare ETF (IXJ)

Tony Featherstone is a former managing editor of BRW, Shares and Personal Investor magazines. All prices and analysis at 18 July 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.