Investment markets and key developments

Global share markets have rallied again this week with US up 3.5%, Australia 2.9%, Europe 3.4%, Japan 3.8% while Chinese stocks are down by 0.3%. Positive gains in most share markets recently after weeks of declines is leading to questions about whether we have seen the low in markets. Our view has not changed – we think the risk is of more downside to equities until there are clearer signs that inflation has peaked (which means central banks can pause on rate hikes) and until economic data troughs (but hopefully avoids a recession). On a 6-12 month view, we are more optimistic on shares as inflation recedes, central banks stop raising interest rates (and maybe even cut rates) and a deep recession is avoided.

The US 2/10-year bond spread remained inverted this week, European bond yields were a tad higher because of Italian political mayhem (Italian 10-year yields are up to 3.5% from 3.2% at the start of the week), the US dollar is down marginally from recent highs but is still elevated and the $A is at 0.69 USD.

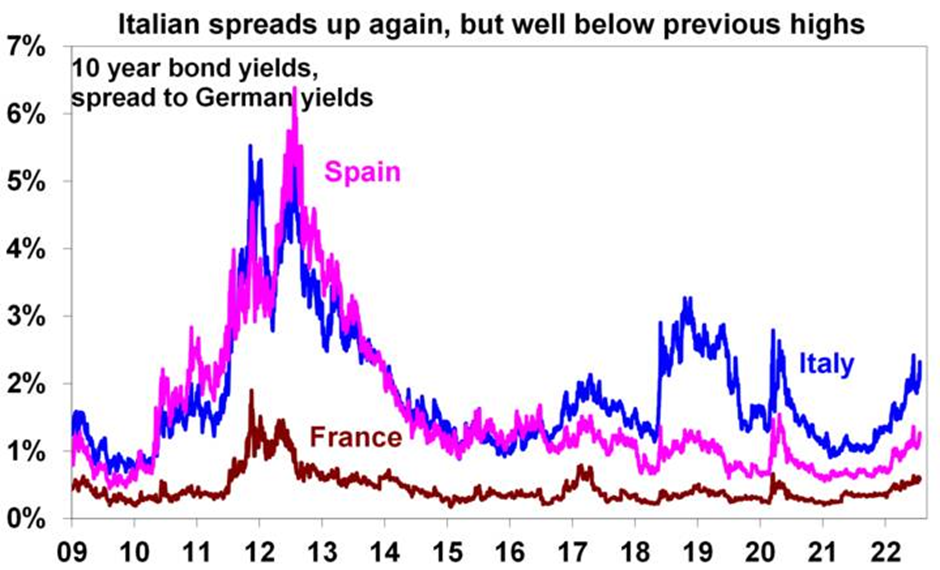

After three key parties in Italian Parliament cast a “no confidence” vote over the government Italian Prime Minister Mario Draghi resigned which means that an election will occur, on 25 September. Italy is no stranger to political instability (because of a highly fractured parliament with lots of minor parties) the last 161 years yielding 132 governments – that means an average 15-month tenure (Draghi’s government lasted 18 months – more than normal!). No doubt there will now be concern around whether this instability has implications for Italy’s membership in the Eurozone. The pandemic and war in Ukraine have strengthened the Euro and support for the Euro remains very strong in Italy, with the latest Eurobarometer survey showing that 72% of respondents in Italy supported the Euro (above the 69% reported for the EU 27). Nevertheless, new elections and populist parties increase the risk of calls for Italian independence. Italian bond spread to Germany were up again this week on political uncertainty but are well below previous peaks like in the Eurozone debt crisis or 2019/20 which also saw political uncertainty.

Source: Bloomberg, AMP

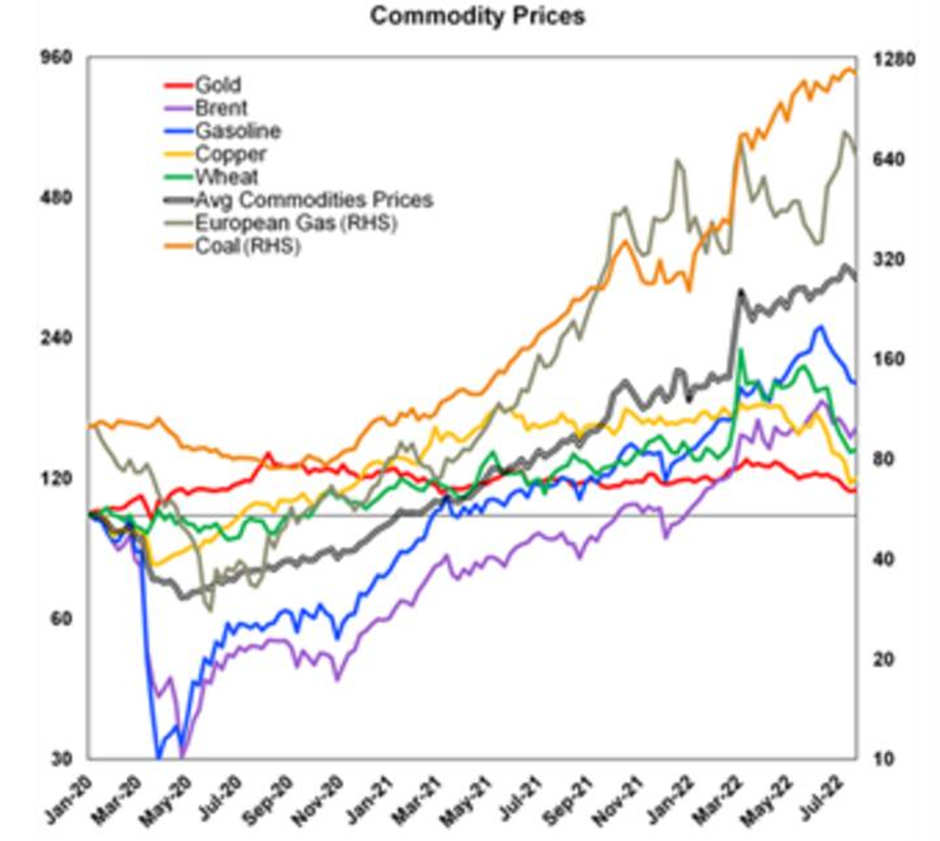

Gas flows to Europe will restart from the Nord Stream 1 pipeline which has been halted since July 11 for scheduled maintenance. Reports are mixed but it seems that initial gas flows will be at 40% of capacity (the same as pre-maintenance) but it could go down to 20% if disputes over sanctioned parts of the pipeline are not resolved. This uncertainty around supply will keep gas prices high for now. While most metals and agricultural commodity prices have fallen in recent weeks, gas and coal prices remain elevated (see the chart below).

Source: Bloomberg, AMP

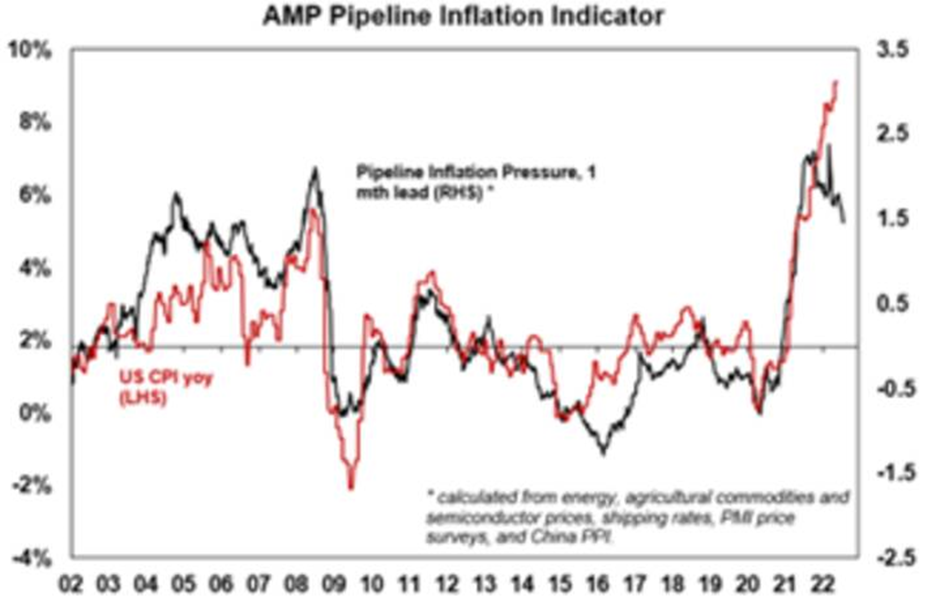

Lower commodity prices will be necessary to see a slowing in inflation. Our Pipleline Inflation Indicator (see chart below) continues to track down and points to a decline in inflation on a 6-12 month time horizon.

Source: Bloomberg, AMP

Economic activity trackers

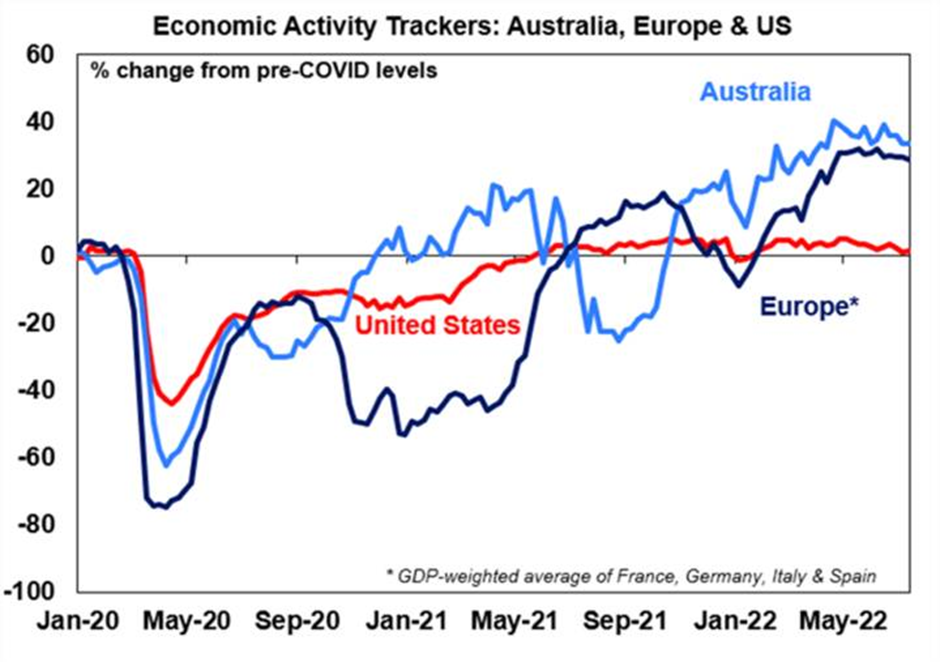

Our Weekly Economic Activity Indicators are flattening across Australia, US and Europe (see the chart below) which is expected as interest rates rise. The indicators have not fallen drastically despite economic fears and share market declines.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Australian economic events and implications

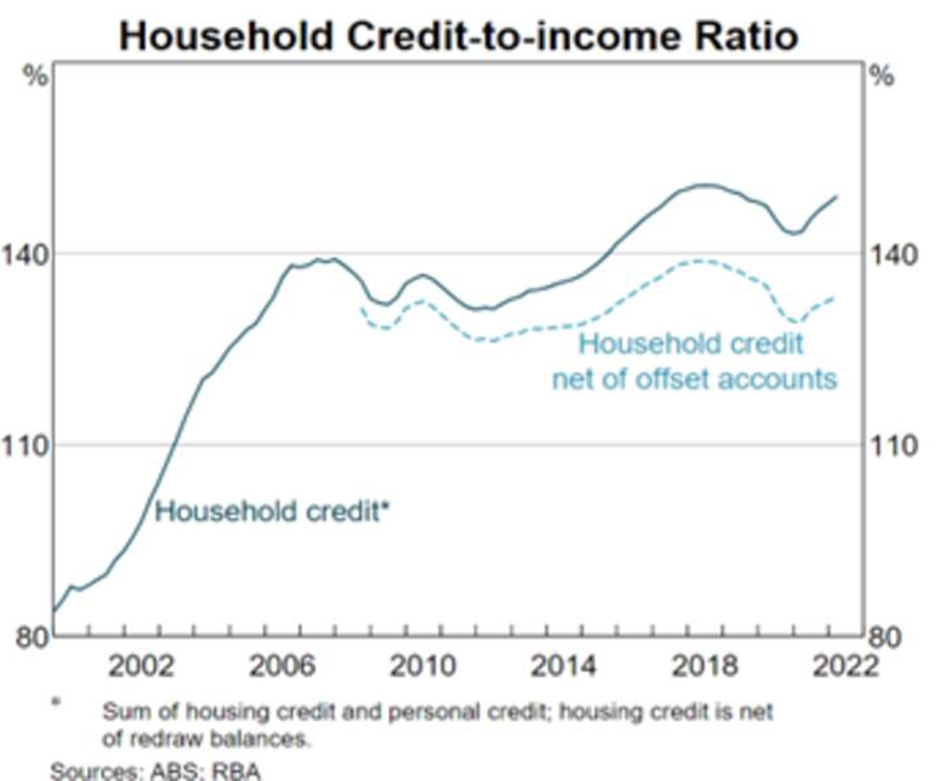

There was lots of “RBA speak” this week. The only major update in the RBA board minutes for July was the inclusion about the Board’s discussion of the neutral cash rate which the RBA assumes is at least 2.5% (but notes that there is a wide margin of error around this estimate) which means many more rate hikes from here. Governor Lowe’s speech on “Inflation, Productivity and the Future of Money” didn’t offer any new insights but reiterated the importance of defending the 2-3% inflation target which means that inflation expectations can’t shift up too much. Deputy Governor Michelle Bullock spoke on “How are households placed for interest rate increases?” and downplayed the potential impacts to indebted households from higher interest rates. Bullock highlighted the usual positive sentiments around households including high accumulated savings worth $260bn that can be drawn down and the large stock of mortgage prepayments, with the household credit to income ratio around the same level as in 2007 once you account for offset accounts (see the chart below).

The RBA’s overall message is that the average household with mortgage debt will be able to withstand at least 300 basis points of rate hikes. We think this underestimates the risks to the economy from those borrowers which are heavily impacted by rate rises. On the RBA’s own estimates, around 38% of households with a mortgage will see a lift in monthly repayments of 40% or more, which is around 1.3 million households. Out of interest, for borrowers on fixed-rate mortgages expiring next year, the median increase is expected to be around $650/month. This is a huge increase and is too large to be compensated by a rise in wages growth. Along with higher inflation (particularly on essential items), these households will have a significant pull-back in spending, especially if the unemployment rate increases.

Treasurer Jim Chalmers formally announced the terms of reference for the review on the RBA this week which will be overseen by three exports, with a recommendation to the government by March 2023.

The June quarter NAB business survey was also released which showed a drop in drop in confidence over the quarter to June (down to 5 from 14 last quarter), after a fall in the March quarter. The July composite PMI fell to 50.6, from 52.6 last month, with a larger drop in services while manufacturing fell only slightly.

All prices and analysis at 25 July 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.