Investment markets & key developments: recession fears run rampant

Recession fears dominated over the last week pushing US, European and Japanese shares down, although Chinese shares (having already had a 35% bear market) rose. Australian shares were little changed with gains in utilities, energy and industrials offset by falls in property, IT and telco shares.

Recession fears also pushed down long-term bond yields, oil prices and metal prices with the iron ore price falling about 10% on Friday. And this also pushed the AUD down to near $US0.68 as the USD continued to rise.

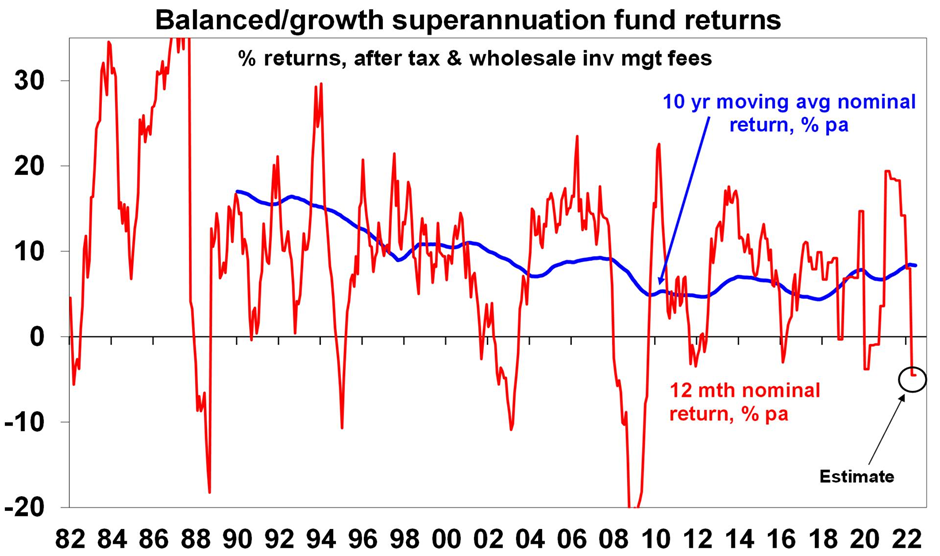

A rough financial year

Thanks to central bank monetary tightening on the back of the worst inflation break out in decades not helped by the invasion of Ukraine, bond yields surged over the last financial year (resulting in an 8-10% loss for bonds) and shares fell (with Australian shares returning -6.5% and global shares returning about -10%).

As a result, balanced growth superannuation funds are estimated to have seen a negative return of about -3 to -5% over the last financial year. No one likes to see their wealth fall but it's wise to bear in mind that: periodic share market falls are normal; as a result, super funds also have periodic setbacks; but the longer-term returns from shares and super are solid with the latter averaging a 7.5%pa return over the last 30 years; switching to cash after a fall will just turn a paper loss into a real loss; and when shares fall they are cheaper offering higher long term return prospects.

Source: Intech, Morningstar, AMP

More of the same from central bankers who remain hawkish

The key messages from global central bankers (the Fed’s Powell, the ECB’s Lagarde and the BoE’s Bailey at the ECB’s Sintra conference and RBA Governor Lowe in Zurich late last week) were that:

- The low inflation environment is behind us:

- “I don’t think we are going back to that environment of low inflation … [inflationary] forces have been unleashed as a result of the pandemic [and] geopolitical shock” (Lagarde);

- “We are now in this new world ... with higher inflation and many supply shocks” (Powell).

- There is increasing concern about rising inflation expectations making it harder to get inflation back down without even higher interest rates. For example, Lowe noted that if workers and businesses don’t believe the RBA will credibly get inflation back to target then it will have to impose much higher interest rates.

- They are resolutely focussed on getting inflation back down with recession risks a secondary consideration – “we are committed to and will succeed in getting inflation down to 2% ... The process is highly likely to involve some pain, but worse pain would be from failing to address this high inflation and allowing it to become permanent.” Governor Lowe noted that there is just a “narrow path” to control inflation without having a recession.

So the bottom line remains that until there is clear evidence inflation is falling central banks will continue tightening, keeping recession risk high. And if a recession eventuates shares likely have more downside as earnings start to fall, because the falls in markets so far mainly reflect a valuation adjustment (i.e. lower PE’s) in response to higher bond yields. Either way – given the uncertainties it’s still too early to say that shares have bottomed. And share markets have yet to see most of the technical signs coming out of major market bottoms (e.g. VIX above 40, very high put/call ratios and strong volumes on bounces). The September quarter is traditionally weak for shares which suggests shares could make a bottom around September or October.

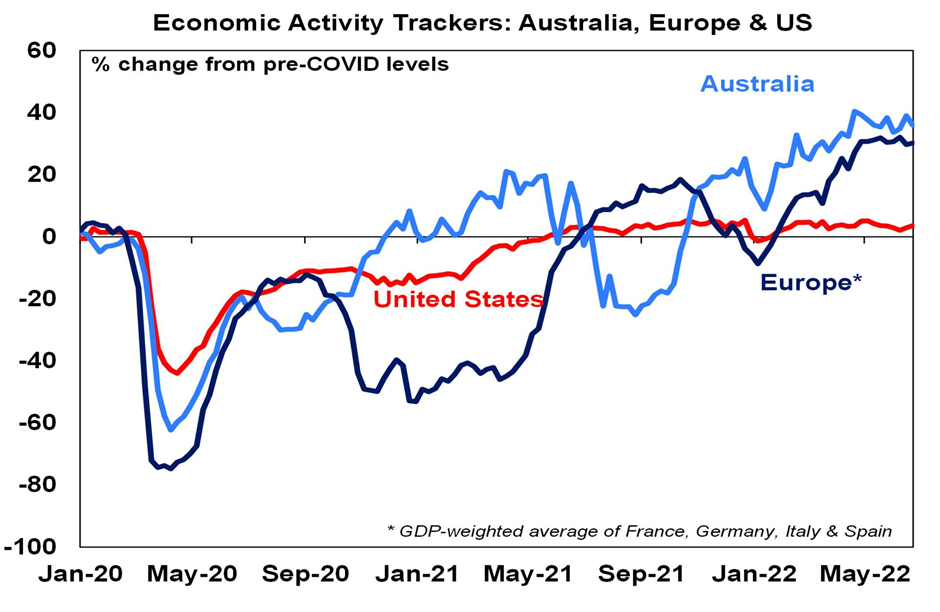

Economic activity trackers

Our Australian Economic Activity Tracker slipped in the last week with declines in hotel and restaurant bookings and shopper traffic. It remains strong but appears to have stalled since April. Our US Tracker rose slightly but Europe was little change. All are yet to show clear indications of recession.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Major global economic events and implications

US economic data was a mixed bag. Durable goods orders remain in a decent upwards trend auguring well for business investment and home prices are still rising rapidly. However, real personal spending fell in May and more leading indicators are soft with falls in consumer confidence and regional manufacturing conditions indicators. The Atlanta Fed’s GDPNow has June quarter GDP at -1% which if realised will meet the “two quarters in a row” definition of a recession as March quarter GDP fell too. However, with real final demand, personal income and payrolls remaining strong it's unlikely that the NBER will define this as a recession.

US inflation as measured by the core private final consumption deflator fell again in May but it's still high at 4.7%yoy and trimmed mean underlying inflation rose further to 4%yoy. So, the fall in May is unlikely to see the Fed ease up on rate hikes. Note that PCE deflator inflation tends to run lower than the CPI because it effectively allows for compositional shifts in consumer spending (as people spend more on falling price products and less on rising price products) and has a lower exposure to shelter.

Eurozone economic sentiment fell again in June but remains well above 2020 pandemic lows – although this is not so for consumer sentiment which is now very weak. Unemployment fell further to 6.6% in May but is likely to be at or close to the low for a while. A 60% cut in Russian gas flows via the Nordstream pipeline to Germany (supposedly due to part supply disruptions) is raising the risk of a complete gas flow shutdown to Germany and a deeper hit to the German economy.

Japanese economic data was mixed with strength in retail sales and mild Tankan business conditions readings but weaker consumer confidence, a sharp fall in industrial production and a rise in unemployment.

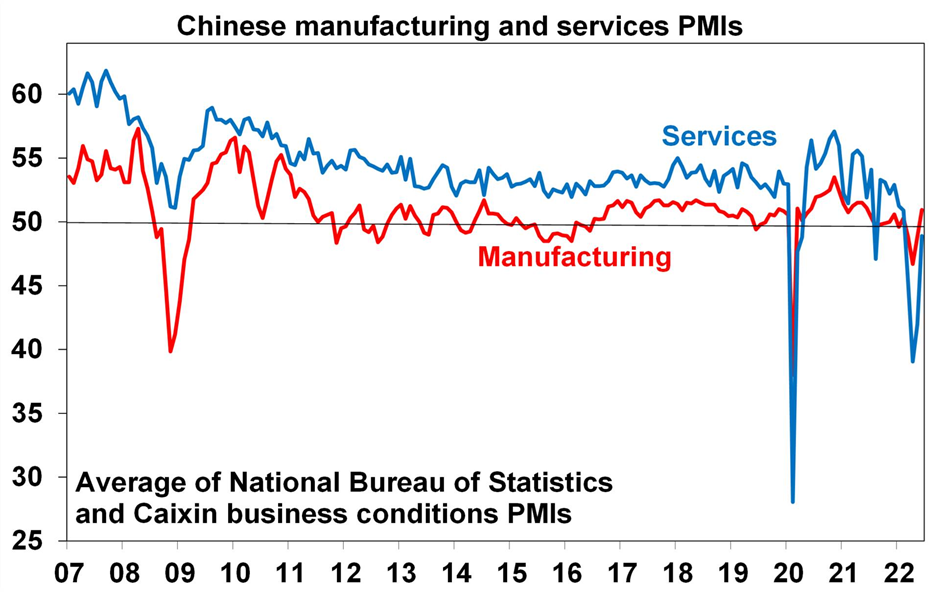

Chinese business conditions PMIs rose sharply again in June as covid restrictions eased driving the official composite PMI to a solid reading of 54.1.

Source: Bloomberg, AMP

All prices and analysis at 4 July 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.