Investment markets & key developments: too early to tell that shares have bottomed

Share markets managed to stabilise and, in most major markets, bounce from oversold levels over the last week as there were no new hawkish surprises from central banks and weak economic data saw bond yields fall taking pressure off share market valuations despite increasing worries about recession.

For the week (to date) US shares are up just over 3% and Australian shares rose by just over 1% led by IT, property and health stocks. Growth downturn fears pushed bond yields down (with 10-year yields down 0.4% and 0.5% from their recent highs in the US and Australia respectively) and also drove oil, metal and iron ore prices lower. The AUD remained around $US0.69 as the USD fell slightly.

After 10%+ falls over the previous two weeks shares were due for a bounce which we saw in the last week. Increasing signs of capitulation in the last few weeks – with indiscriminate selling of shares is a positive sign in terms of capitulation – and the bounce may have further to go. But it’s still hard to be confident from a technical perspective that we have seen the bottom – both put/call option ratios and VIX have yet to reach extremes seen at past major bottoms.

And the macro story remains the same with further higher inflation readings in the past week (in the UK where it rose to 9.1%yoy and in Canada where it rose to 7.7%), more hawkish comments from central banks (the Fed, ECB and RBA and a 0.5% rate hike in Norway) and ongoing fears of recession. We remain of the view that a global recession can be avoided but with central banks hiking rates aggressively the risks have increased to the point that it's now a close call. This is reflected in the breakdown in the growth-sensitive copper price and the Korean share market (often referred to Dr Copper and Dr Kospi). And if a recession eventuates shares likely have more downside, because so far the falls in markets mainly reflect a valuation adjustment (ie lower PEs) in response to higher bond yields. Either way – given the uncertainties it’s still too early to say that shares have bottomed.

The Fed remains hawkish – but maybe a bit less so than markets had been allowing for. While Fed Chair Powell’s Congressional testimony reiterated the Fed’s commitment to bring inflation down, it did not signal a further leg up in hawkishness from what markets were already expecting. That said, he did note that achieving a soft landing will be “very challenging” and recession is “certainly a possibility”. This along with falls in US business conditions PMIs saw market expectations for the Fed Funds rate at year-end wound back by about 0.25-3.45%.

- The RBA is also hawkish - but like the Fed was a bit less so than many expected. The key messages from Governor Lowe were that:

- The RBA will do what is necessary to return inflation to target but is not seeking to do so immediately;

- It is very focused on keeping inflation expectations down (and hence wants to see wages growth with a 3 in front of it, but not a 5);

- More rate hikes are on the way;

- It does not see a recession; and

- Is not on a pre-set path but will be guided by data.

Governor Lowe’s dismissal of the risk of a recession should be taken with a grain of salt – he would say that and it's hard to deny that falling real incomes and rate hikes have not significantly increased the risk of recession – and the money market has given a better lead on rate hikes than the RBA has. However, our assessment remains that the next hike will be 0.5%, the cash rate will “only” rise to 2.1% by year-end and will peak at about 2.6% in the first half of next year.

While money market expectations for the RBA cash rate have fallen sharply over the last week (from 3.86% for year-end to 3.22%) over the last week in response to Lowe’s comments and recession fears, at 3.9% in a year’s time they still look too high. Taking cash rates to around 3.9% will mean variable mortgage rates of 7.5% or so and more than a doubling of household interest payments which would push house prices down by 20-30% and knock the economy into recession given cost of living pressures hitting at the same time. Very weak consumer confidence and slowing credit and debit card transactions as reported by various banks so far this month suggest that consumer spending is starting to slow significantly already. This all means that the scale of interest rate hikes expected by the money market is unlikely to happen.

Maybe it sounds perverse – but the best outcome for share markets would be if economic data starts to slow sharply now. This would take pressure off inflation and enable central banks to ease up on tightening before driving a recession. And on this front, the cooling evident in global business conditions PMIs over the last week (see below) is a positive sign.

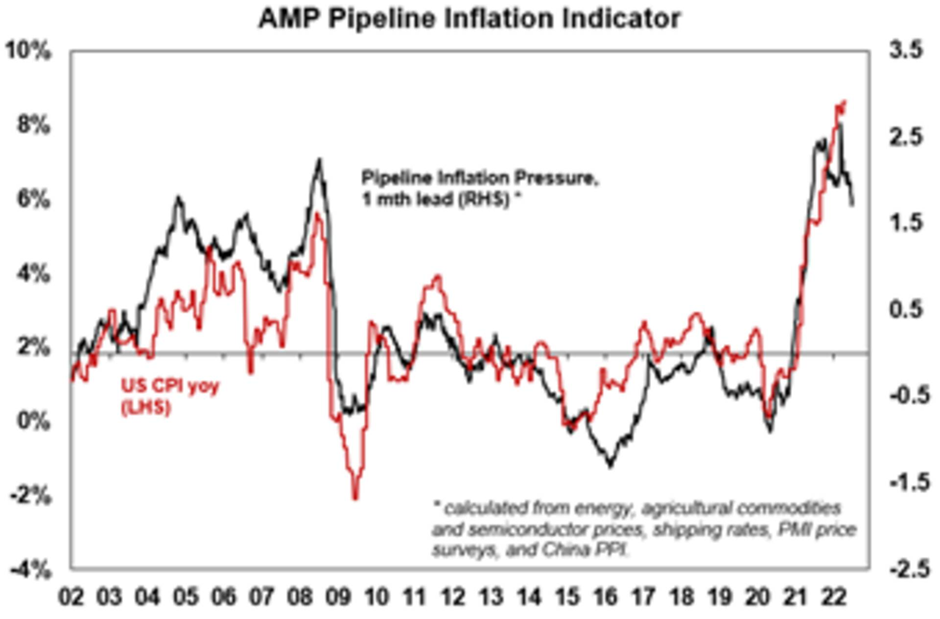

As is the continuing decline in our Pipeline Inflation Indicator. Business survey components relating to prices, work backlogs and delivery times are continuing to show signs of improvement. Shipping and cargo costs look to have peaked. And the recent pullback in oil prices – which are now down 10% from their high early this month helps support the idea that inflation may have peaked. Of course, it's still too early to get too confident on this front given the ongoing risks around Ukraine – with Russian gas being increasingly cut off to Europe and Russia threatening Lithuania over its enforcement of a blockade of EU goods into Kaliningrad.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components

Source: Macrobond, AMP

The RBA’s review of its aborted yield target (which targeted 0.25% initially and then 0.1% for the 3-year bond yield) provided few surprises. Yes, it helped lower funding costs and head off the worst-case downside risks at the height of the pandemic lockdowns. But it contributed to the RBA’s forward guidance (‘no rate hike expected to 2024’) debacle and so caused reputational damage in money markets and in the wider community. It's hard to see the RBA going down that path again.

What to watch over the next week?

In the US, the focus is likely to be on the Fed’s preferred inflation measure of the core private final consumption deflator for May (Thursday) which is expected to fall to a still very high 4.8%yoy from 4.9%. On the economic data front, expect continuing modest growth in durable goods orders (Monday), a fall in consumer confidence (Tuesday) but continuing strength in home prices (also Tuesday) and a slowing in the June manufacturing conditions PMI (Friday).

Eurozone CPI inflation for June (Friday) is likely to show a further rise to 8.3%yoy. Meanwhile, economic confidence for June (Wednesday) is likely to dip further and unemployment (Thursday) is likely to fall to 6.7%.

Chinese business conditions PMIs for June (due Thursday and Friday) may show a further improvement reflecting recovery from the covid lockdowns around March.

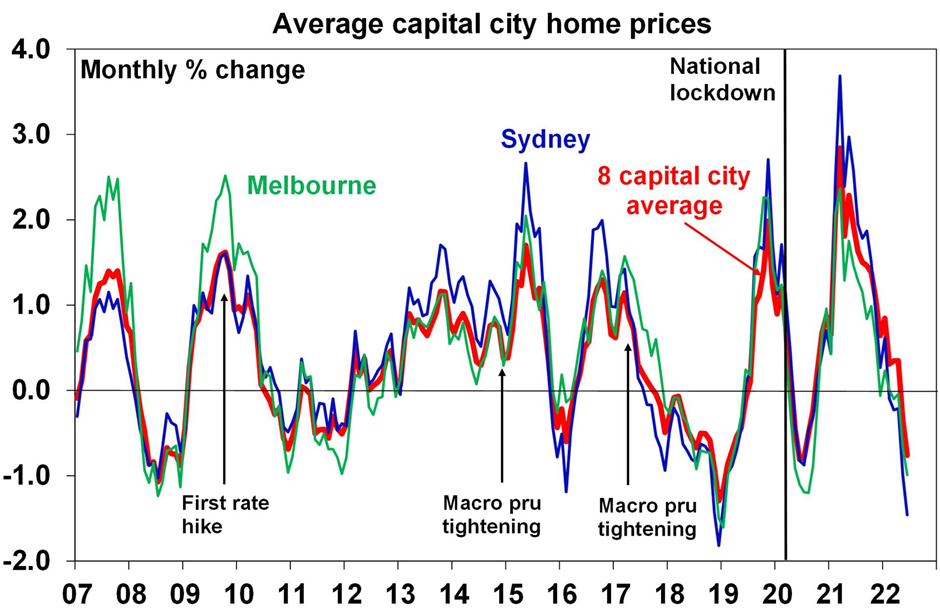

Australian retail sales growth for May is expected to slow to 0.3% reflecting the impact of cost-of-living pressures and the hit to confidence from rising interest rates. Further weakness is likely ahead. Job vacancies data for May is likely to have remained strong and credit growth is expected to remain strong reflecting earlier strength in housing finance (both due Thursday). CoreLogic home price data is expected to show capital city home price falls accelerating to -0.8% in June led by Sydney and Melbourne.

Source: CoreLogic, AMP

All prices and analysis at 27 June 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.