Investment and markets update: what investors should watch out for this week

Share markets saw a bit of relief in the past week - bouncing off oversold lows helped by less hawkish than feared comments from the ECB and Fed, a further pullback in US bond yields, improved outlooks from some US retailers and airlines and M&A activity. This left the US share market on track for its first weekly gain after seven weeks of falls, and European, Japanese and Australian shares also rose. In Australia, gains in resources and financials offset falls in telcos, consumer staples and IT stocks. Bond yields fell in the US and Australia but rose in Europe. Oil and copper prices rose, but iron ore prices fell. The risk-on tone helped the AUD rise as the USD fell.

Rate hikes continue but with mixed messages from central banks.

- At the hawkish end, the RBNZ raised its cash rate by 0.5% taking it to 2% and significantly revised up its forecasts for the cash rate to a peak of 3.9% next year all clearly aimed at slowing demand and keeping inflation expectations down. With the NZ economy already slowing though the RBNZ may be starting to get a bit too extreme (as it often does) and so may reach a peak in its cash rate earlier and lower than its currently projecting.

- The Bank of Korea hiked its cash rate by 0.25% to 1.75% and remained hawkish too although maybe not as much as the RBNZ.

- ECB President Lagarde pre-announced near-term monetary policy moves with the end of quantitative easing early next quarter, a rate hike in July and the end of negative rates by September. While this was unusual it looks designed to reduce uncertainty around monetary policy. Lagarde also pushed back against ECB Council members arguing for 0.5% hikes saying “we don’t have to rush.” This helped boost Eurozone shares.

- The minutes from the Fed’s last meeting indicated that after two more 0.5% hikes it would be well-positioned to assess the impact and need for more policy moves later this year. The market interpreted this as indicating that the Fed is prepared to be flexible, opening the possibility of a pause later this year.

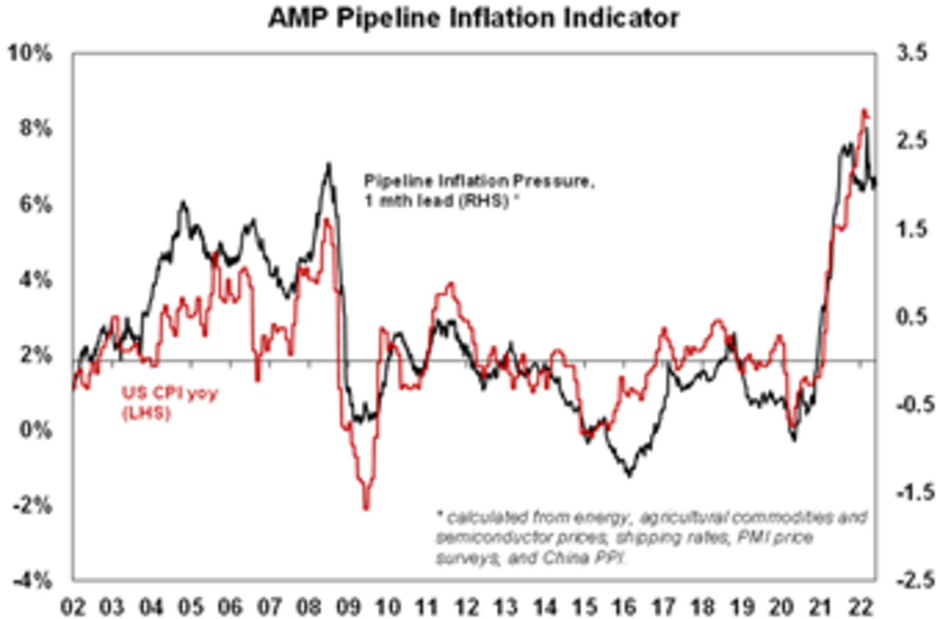

Of course, it is dangerous to read too much into central bank comments either way. Just over 6 months ago the Fed was saying it could be patient in removing monetary stimulus and the RBA was indicating a rate hike was unlikely before 2024. Ultimately central banks are data-dependent. And they want to see clear evidence that inflation is cooling. There are some positive signs on this front though: business surveys are reporting improving delivery times, reduced backlogs and some topping in input and output price pressures; US retailers have seen an increase in inventories presumably as spending rebalances back to services and production catches up; there are some signs of a slowing in hiring in the US with initial jobless claims starting to trend up, with Amazon saying it's gone from understaffed to overstaffed and giving up space and Lyft pausing hiring; wages growth in the US looks to have peaked late last year, and our Pipeline Inflation Indicator continues to point to peaking in US inflation.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components

Source: Macrobond, AMP

Though at this stage, it’s a bit too early to relax. Rising oil and hence petrol prices are a fly in the ointment of the “peak inflation” view and commodity prices generally still look strong. This could be accentuated if Europe bans Russian oil (as looks likely) and there is a disruption to Russian gas flowing to Europe. Even if US inflation has peaked it will take a while before it's fallen back to levels where the Fed can relax.

And in Australia, inflation probably won’t peak until later this year with petrol prices back up, household energy bills set to rise significantly on the back of higher wholesale power prices from earlier this year (this has been well known for a while but will start to show up in power bills from July) and supermarkets warnings of still rising prices.

At the same time shares are yet to see clear signs of a washout bottom - with VIX and put/call ratios yet to reach levels seen at past major share market bottoms. The bottom line is that while we remain optimistic that recession will be avoided in the next 18 months and so shares can rise on a 6-12 month view, shares are still at risk of more downside in the short term (notwithstanding that the current bounce may have further to go).

What to watch over the next week?

In the US, the main focus is likely to be on May job data (Friday) which is expected to show payrolls up 330,000, unemployment falling slightly to 3.5% and wages growth slowing slightly to 5.2%yoy (from 5.3%). In other data, expect house price gains to remain strong but consumer confidence to fall (both Tuesday) and the ISM manufacturing and services indexes (Wednesday and Thursday) to fall slightly.

The Bank of Canada (Thursday) is likely to raise its official cash rate by another 0.5% taking it to 1% with the BoC remaining hawkish citing the risk of higher inflation expectations as well as citing concerns about the global growth outlook.

Eurozone confidence data for May (Monday) is likely to show a further softening, core inflation (Tuesday) is likely to show a further rise and unemployment (Wednesday) is likely to remain at 6.8%.

Chinese business conditions PMIs for May (due Tuesday and Wednesday) are expected to improve a bit but remain weak reflecting Covid restrictions.

In Australia, March quarter GDP (Wednesday) is expected to be flat and up 2.3%yoy, with drags from net exports (which are expected to detract 1.8 percentage points) and dwelling investment, weak growth in business investment and solid growth in public spending and consumption. Note though that this follows very strong growth of 3.4% in the March quarter and domestic demand will still be strong. In other data expect building approvals to show an 8% gain after plunging in March and housing credit growth to remain solid (both Tuesday), CoreLogic data for May to show a 0.3% decline in average capital city prices led by a 1% fall in Sydney and 0.6% fall in Melbourne (Wednesday), the trade surplus (Thursday) to fall back to $8.5bn and housing finance for April (Friday) to fall 0.5%.

All prices and analysis as at 30 May 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531). This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.