Moated AI-proof tech play hiding in the ASX 100

Simonelle Mody | Morningstar

AI anxiety has weighed heavily on markets this year. We’ve seen broad and often indiscriminate selling across sectors as investors grapple with the implications.

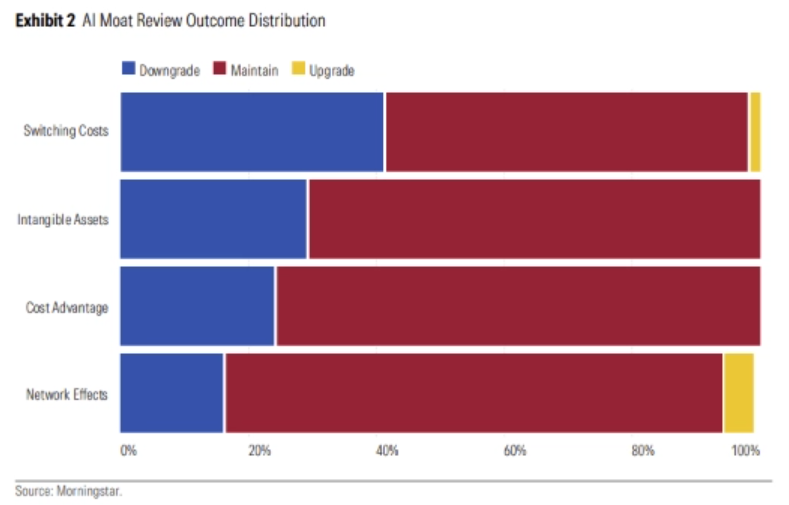

Morningstar analysts recently re-evaluated the moat ratings of 132 companies globally and found that while AI is reshaping competitive dynamics, it is far from a universal destroyer of moats. The review resulted in only a handful of downgrades where moats were directly tied to vulnerably technology rather than structural advantages. Importantly, we do not assume widespread job displacement caused by AI, instead we expect it to enhance augment labour.

Against this backdrop, Seek emerges as one of the tech platforms whose competitive edge appears intact but also structurally resilient. It is currently trading approximately 40% below our fair value estimate of $25 per share.

Seek Ltd ★★★★

- Economic moat: Narrow

- Fair value estimate: $25 per share

- Share price: $14.55 (as of 24 April 2026)

- Uncertainty rating: High

- Price to fair value: 0.58

In the six months to 31 December 2025, Seek reported a 19% increase in EBITDA, primarily driven by a 17% increase in ad yield. This increase matters because it represents an impressive acceleration and suggests fears of AI disruption are misplaced. Instead, it appears likely that AI will be a tailwind, given large language models unlock a whole new set of problems for Seek to solve and monetise.

As a result, analyst Roy Van Keulen increased Seek’s fair value estimate by 10% to $25 per share as we now model more price increases than previously. Shares now screen as materially undervalued.

What does it mean to have a moat?

An economic moat is a structural feature that allows a firm to sustain excess profits over a long period. Companies with a narrow moat are those we believe are more likely than not to sustain excess returns for at least a decade. For wide-moat companies, we have high confidence that excess returns will persist for 10 years and are likely to persist at least 20 years.

There are several sources a company can derive its moat from and these include: network effects, intangible assets, cost advantages, efficient scale and switching costs.

Seek’s moat source

Seek earns a narrow economic moat underpinned by the network effects embedded in its online employment marketplace in Australia and New Zealand. A network effect occurs when the value of a company’s goods or services increase for both new and existing users as more people use them.

Online listing platforms derive their network effects from a self-reinforcing cycle of additional demand on the network attracting additional supply and vice versa. This comes at little incremental expense to the platform operator.

In the case of employment marketplaces like Seek, the value of the network to employers increases with the size and quality of the pool of job seekers, whilst job seekers gravitate to platforms offering the largest and most relevant opportunities. As each side expands, the platform becomes increasingly indispensable to both.

Seek has managed to entrench these network effects through a combination of first-mover advantage and strong execution. The company estimates that its Australian platform facilitates nearly a third of job placements nationally, which view as the most meaningful measure of market share. Its closest competitor, LinkedIn (owned by Microsoft) is responsible for less than 10% of placements.

Why do network effects matter in an AI context?

Across our coverage we find that network effects are the most resilient moat source in the face of AI. While sectors such as design software, cybersecurity, travel networks and music rights also show durability, network‑driven businesses experienced the fewest moat downgrades during our reassessment.

The intuition behind this is relatively straightforward. Network effects are rooted in participation, rather than technology. Even as underlying tech evolves, the value of a large, engaged and interconnected user base is not easily displaced. AI might enhance matching efficiency, but it does not inherently weaken the gravitational pull of an established network. Furthermore, strong networks also create implicit switching costs that are non-technology dependent.

Our broader review of moat stability in the AI era shows that companies maintained their competitive advantages when they benefited from network effects, controlled infrastructure, proprietary data, deep ecosystems, regulatory barriers or unique domain logic. Seek fits squarely within this cohort.

Competitive pressure

We believe differences in industry structure and market dynamics mean the employment market is inherently less conducive to consolidation. Therefore, we expect that Seek will continue to face a more competitive environment, specifically with Microsoft-owned LinkedIn.

We see LinkedIn as offering a platform specialising in the high-end of the market, such as white-collar professionals. On the other side of the spectrum, platforms like Indeed mostly serve the lower-end of the market – low-skilled and entry-level blue-collar professions. Seek straddles across the spectrum but its emphasis is in the middle. We see employers listing on Seek as typically looking to fill enabling business functions e.g. roles in human resources, marketing and accounting.

However, we do believe Seek offers the best navigation for deliberate job seekers and has the largest serviceable market. Seek’s platform is highly intuitive, performant, and feature-rich, and provides, we believe, the lowest friction method for job seekers to actively search for a suitable job listing.

Additionally, like LinkedIn, Seek continues innovating and offers employers an increasing array of verified attributes of job seekers which exceeds the verification features of LinkedIn, such as work rights, licenses, educational attainment and professional experience.

Seek is also not limited to the managerial and professional classes, like LinkedIn, and enjoys near-universal unprompted brand recognition in Australia. Seek’s market share in Australia has averaged around a third over the past five years. Although we expect the employment market to remain highly fragmented, we believe Seek’s network effects and superior navigation features will enable it to remain the market leader in Australia and New Zealand, especially in the middle of the market.

AI fears overblown

We can understand market fears around AI at first glance. Job seekers are likely to ask AI to write their CVs to help them find vacancies. Additionally, AI has inherent advantages because it can search for job listings across multiple websites. However, we believe there is an important second-order consequence that is mitigating this risk.

As job seekers become more efficient at writing applications, they can also apply to many more jobs. From the prospective of hirers, this is resulting in a pile of job applications to sift through. We therefore expect hirers to increasingly rely on marketplaces such as Seek to pre-filter applications. Seek is already doing this in several ways.

One is by increasingly transitioning from an active search-based discovery process to a passive feed-based discovery process, whereby Seek surfaces vacancies in something more resembling a Facebook feed. Vacancies here are tailored to a job seeker’s preferences and qualifications. Another way Seek is doing this is by allowing hirers to search a database of Seek job seekers, with job seekers again prefiltered to improve matches.

Seek has unique data on what makes a good match between a job and a candidate. This is because it can correlate historical vacancies and CV data with subsequent applications and hiring. Moreover, Seek is increasingly using this unique data to serve more relevant vacancies to job seekers and more suitable applicants to hirers. We believe the arrival of large language models gives Seek a tool to do this with greater efficiency and effectiveness. We also don’t think LLM-providers, like OpenAI, can extract economics as these can be easily swapped with another provider.

Access this research and more at Morningstar. For a free four-week trial, click here.

All prices and analysis at 24 April 2026. This information has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892.). Morningstar’s full research reports are the source of any Morningstar Ratings. The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.