Finding the bargains on an ASX propped up by houses and holes

Suhas Nayak | Allan Gray

In our June 2025 quarterly commentary, we discussed how five companies had been doing the heavy lifting for the S&P/ASX 300 Index (the Index) since 2024.

The first quarter of 2026 has been no different.

Despite this backdrop, it has been reassuring to see the Allan Gray Australia Equity strategy portfolio hold up, especially as it has minimal exposure to these five largest companies. And just as trees do not grow to the sky, we believe these trends cannot continue forever, which should position the Equity strategy well for potential relative performance.

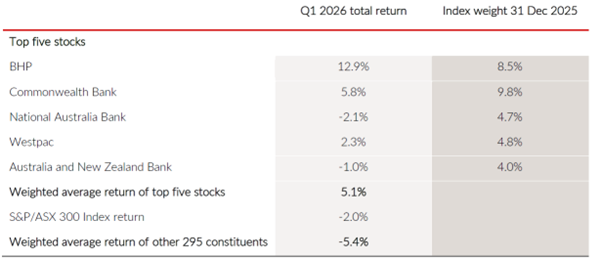

The top five companies

The Index’s returns in the first quarter of 2026 have been dominated by its top five stocks: the four large domestic banks and BHP (ASX: BHP). The weighted average return of those companies was 5.1%, versus the Index’s total return of -2.0%. This implies the 295 other companies contributed a return of -5.4%, underperforming the overall index by 3.4%, as shown in Table 1.

Table 1 - Returns in the first quarter of 2026

Source: FactSet, Allan Gray, 31 March 2026.

We don’t know what is driving this level of dislocation in the market. We hypothesised in our previous quarterly commentary that passive-fund flows and the influence of ‘Your Future, Your Super’ performance tests could be what is driving the momentum and share price performance of large stocks in general.

Regardless of the cause, it is clear that the outperformance of these few companies cannot coexist with the material underperformance of some of the remaining 295 companies in perpetuity. In particular, banks do not exist in a vacuum, and neither do the fundamental drivers of their earnings. If the underperformance of some of the remaining 295 companies continues, it will have a direct impact on the banks’ bottom lines. Below we highlight three examples.

Office workers and their banks

Dexus (ASX: DXS) has underperformed the Index by 12.5% in the quarter. The company is primarily a real estate investment trust (REIT), whose assets are predominantly office buildings that are often in prime central business district locations throughout Australia. Presumably Dexus’s share price weakness is a result of changed expectations around Australian interest rates (previously the Reserve Bank was expected to cut interest rates and now rate increases are priced in) or the fears around AI’s impact on office occupancy through redundancies.

But AI’s impact on redundancies cannot only affect Dexus. Office workers are some of the heaviest consumers of bank products, particularly residential mortgages. It is highly unlikely that out-of-work office workers who no longer use Dexus office space can still afford their mortgage repayments. And yet in the Index, these two scenarios seemingly coexist.

And while interest rates may well dampen office valuations further from lower rates of return, we must not forget that interest rates are rising due to stubborn inflation, which directly affects office rents.

Higher rates also increase replacement costs. Already, Dexus trades at a material discount to (already written-down) book value and to replacement costs, a discount that will only widen if inflation persists.

This is not to say that Dexus couldn’t possibly be more impacted than a poor bank with an outsized exposure to a soon-to-be unemployed white-collar workforce, but today’s narrative doesn’t seem to explore the delicate ecosystem that exists between companies.

Also absent from any narrative is an assessment of what is already priced into a company’s share price. Dexus’s meaningful discount to the market value of its asset base suggests that some of these impacts might already be anticipated and already reflected in its share price. Consensus forecasts for Australia’s banks do not incorporate a credit impairment cycle, the likes of which would almost certainly present if office workers were suddenly unemployed by AI or if interest rates increase from here.

The Dexus opportunity also reminds us of the retail shopping centre REITs in the lead-up to and during COVID-19. Online shopping was considered an existential threat to companies like Scentre Group (ASX: SCG) and Vicinity Centres (ASX: VCX). Instead, prime shopping centres have subsequently had a renaissance, driven perhaps by a mix of inflation, replacement costs and, importantly, retail sales. Dexus now makes up over 3.5% of the Allan Gray Australia Equity strategy portfolio.

CSL Limited’s growth and multiples

CSL (ASX: CSL) is a producer of blood plasma products, alongside other specialty pharmaceuticals and vaccines. It has had tremendous success over decades by building out a network to collect plasma, separate it into its constituent proteins efficiently, and gain approvals for its use in more indications than any of its rivals. This has seen revenues and earnings grow in the mid to high single digits for most of that period, a consistency that used to earn CSL a very high price-to-earnings (P/E) multiple.

Lately, competition from other plasma producers and from alternative therapies has seen expectations around growth reduce. This year has also seen changes to the albumin (one of the proteins extracted from plasma) market in China and persistent weakness in influenza vaccine demand in the US. As a result, CSL’s forward P/E multiple is less than 15 times 2026 financial year (FY26) earnings and a little over 13 times FY27 broker consensus earnings. The growth implied in those consensus estimates of around 8% is clearly not valued by the market, and certainly not as highly as CBA’s 4% expected growth rate, which earns it a multiple of more than 25 times earnings.

CSL has disappointed the market a number of times in the past, and it is quite possible that future earnings may similarly disappoint.

We’d argue that this is at least partly reflected in its share price. For whatever reason, the market has taken a particularly dim view of CSL’s exposure to competition while effectively ignoring the Big Four banks’ own battles with competition (the clearest example being Macquarie’s rapid share growth) and the commoditisation of their products. We see a relative value opportunity here, and CSL now represents over 4% of the Equity strategy portfolio.

Banks and the building cycle

The building cycle is typically a big driver of bank credit growth. New projects developed and sold require new loans to be advanced. And renovations typically require mortgage redraws.

We are finding opportunities in companies exposed to the building cycle. Admittedly, these companies are mostly exposed to the US building cycle, where activity levels seem low overall due to the wide spread between mortgage rates today and those that prevailed a few years ago. Unlike Australia, borrowers in the US typically lock in fixed rates for the duration of their mortgage, often 30 years. That change in spread has prevented people from moving home and taking out new loans, due to the significantly higher interest rates they would pay, which has depressed demand and in turn building activity levels.

With higher mortgage rates than the US, Australia is not necessarily immune to this building cycle.

Housing affordability in Australia (which is already at record lows) is rapidly affected by changes in interest rates, as most loans are variable or fixed for only short periods (typically up to five years). It is well known that building activity levels and discretionary spending fall as interest rates rise. But credit expansion, the engine room of bank profitability, also slows as borrowers focus on reducing their indebtedness as quickly as possible. Higher interest rates also impact the quality of bank assets and the impairment cycles which follow can be devastating for these highly geared beasts. Yet bank performance would have you believe otherwise.

Building-cycle-exposed companies like Reece, Reliance and James Hardie, all of which also have Australian exposure, have had particularly weak share price performance and may well offer considerably more upside potential than Australia’s beloved banks. We are watching these building-cycle-exposed companies closely and have recently accumulated a modest exposure to them in the portfolio.

The market dislocation is presenting us with many new opportunities because the narrowness of the set of companies driving index performance makes many of the other companies seem relatively cheap. This shows in the overall P/E ratio of the Allan Gray Australia Equity strategy (13.9 times consensus forward earnings) versus the Index’s overall 16.9 times. It’s unusual for us to devote an entire quarterly commentary to a top-down look at the Equity strategy portfolio’s relative value, but with dislocation at these severe levels, we felt it had to be covered. We will endeavour to shine a spotlight on one of the portfolio’s holdings next quarter.

This is an extract from our March 2026 Quarterly Commentary (originally published on 31 March 2026). Download the full Quarterly Commentary.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 14 April 2026. This document was originally published in Livewire Markets on 14 April 2026. This information has been prepared Allan Gray Australia Pty Limited ABN 48 112 316 168, AFSL No. 298487. The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.