The Best US Tech Stocks to Buy

Tori Brovet | Morningstar

Technology stocks offer investors the promise of growth in ways few other sectors can. After all, tech is synonymous with innovation, spawning new products, services, and features.

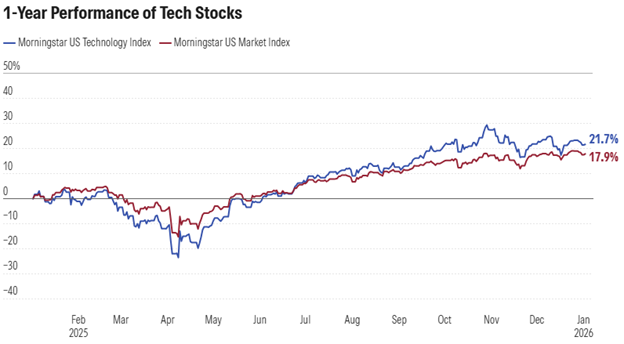

Over the past 12 months, the Morningstar US Technology Index rose 21.70%, while the Morningstar US Market Index gained 17.92%.

Source: Morningstar

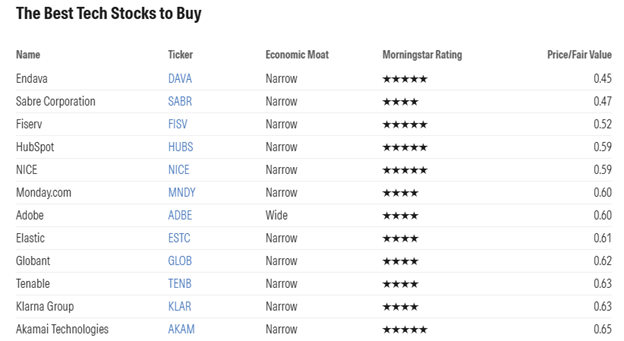

The 12 Best Tech Stocks to Buy Now

These were the most undervalued tech stocks that Morningstar’s analysts cover as of Jan. 2, 2026.

- Endava DAVA

- Sabre Corporation SABR

- Fiserv FISV

- HubSpot HUBS

- Nice NICE

- Monday.com MNDY

- Adobe ADBE

- Elastic ESTC

- Globant GLOB

- Tenable TENB

- Klarna Group KLAR

- Akamai Technologies AKAM

To come up with our list of the best tech stocks to buy now, we screened for:

- Technology stocks that are undervalued, as measured by our price/fair value metric.

- Stocks that earn narrow or wide Morningstar Economic Moat Ratings. We think companies with narrow moat ratings can fight off competitors for at least 10 years; wide-moat companies should remain competitive for 20 years or more.

- Stocks that earn a Low, Medium, High, or Very High Morningstar Uncertainty Rating, which captures the range of potential outcomes for a company’s fair value.

Here’s a little more about each of the best tech stocks to buy, including commentary from the Morningstar analysts who cover each company. All data is as of Jan. 2, 2026.

Endava

- Morningstar Price/Fair Value: 0.45

- Morningstar Uncertainty Rating: High

- Morningstar Economic Moat Rating: Narrow

- Industry: Software—Infrastructure

Software infrastructure firm Endava is the cheapest stock on our list of the best tech stocks to buy. Endava is a next-generation IT services company that primarily assists clients with their digital transformation efforts by creating customized software for them. The stock is trading 55% below our fair value estimate of $13.60 per share.

Endava, based in the UK, is an IT services company focused on providing digital transformation and engineering services. It generates revenue primarily by charging clients on a time-and-materials basis for services such as consulting and advice, customized software development and integration, and quality assurance and testing. Endava is highly exposed to the financial-services sector, with nearly half of its revenue generated from the sector. Within financial services, Endava is known for its expertise in payments and private equity.

Like many of its peers, Endava’s core strategy is to land and expand, which involves securing major clients and increasing revenue through these relationships by providing them with an increasing range of services. Endava’s 10 largest clients account for around a third of group revenue, with the largest, Mastercard, contributing around 10%. Mastercard has been a client for over 20 years.

Endava focuses on the financial services, technology, media, and telecom industries. The company aims to diversify its industry exposure by securing new clients from new verticals. In particular, Endava is targeting clients in the retail and healthcare sectors, as its current expertise is most transferable to these areas.

Similarly, the company is geographically concentrated, with around 33% of revenue generated in the UK and around 23% generated in continental Europe. To diversify, Endava is primarily growing its business in North America.

Endava’s delivery model is based on agile project management from employees in nearshore locations, which it plans to expand. To best serve its clients’ unique digital transformation goals, the flexibility of the iterative nature of agile project management is effective. Furthermore, the nonstandardized nature of these projects requires constant dialogue and interaction between Endava and its clients, which means having delivery teams with similar time zones to those of its clients (nearshoring) is best for delivering the project successfully and promptly.

Rob Hales, Morningstar senior analyst

Sabre Corporation

- Morningstar Price/Fair Value: 0.47

- Morningstar Uncertainty Rating: Very High

- Morningstar Economic Moat Rating: Narrow

- Industry: Software—Infrastructure

Sabre holds the number-two air booking volume share in the global distribution system industry. Sabre Corporation is an affordable tech stock, trading at a 53% discount to our fair value estimate of $2.82 per share. The software infrastructure firm earns a narrow moat rating.

Despite near-term economic growth concerns caused by tariff uncertainty and the US government shutdown, which is negatively affecting its corporate and government business, we expect Sabre to reduce net debt/adjusted EBITDA to 6 times by the end of 2025 from 19 times in 2024, using proceeds from the prudent sale of its hospitality solutions business. We maintain our stance that Sabre will hold its position in global distribution systems, or GDS, over the next 10 years. This view is driven by a gradual recovery in corporate travel and Sabre’s leading network of airline content and travel agency customers, as well as its solid position in technology solutions for these carriers and agents. Sabre’s 30%-plus GDS air transaction share is the second largest of the three companies (behind narrow-moat Amadeus and ahead of privately held Travelport) that together control about 100% of market volume.

Sabre’s GDS enjoys a network advantage, which is the source of its narrow moat rating. As more supplier content (predominantly airline content) is added, more travel agents use the platform, and as more travel agents use the platform, suppliers offer more content. This network advantage is solidified by technology that integrates GDS content with back-office operations of agents and IT solutions of suppliers, which would require significant costs and time to replicate, and leads to more accurate information that is also easier to book. The firm’s network prowess should be supported by its technology partnership with wide-moat Alphabet and its transition to the cloud, both of which we see driving innovation and cost efficiencies. The company’s next-generation platform, SabreMosaic, is an open-source cloud-based artificial intelligence solution that makes it easier for airlines to customize its offering and upsell content.

The company’s GDS faces some risk of larger carriers making direct connections with larger agencies, although we expect these relationships to be the exception rather than the rule and expect Sabre to still be the aggregating platform in either case.

Dan Wasiolek, Morningstar senior analyst

Fiserv

- Morningstar Price/Fair Value: 0.52

- Morningstar Uncertainty Rating: High

- Morningstar Economic Moat Rating: Narrow

- Industry: Information Technology Services

Next on our list of the best tech stocks to buy is Fiserv. Fiserv is a leading provider of core processing and complementary services, such as electronic funds transfer, payment processing, and loan processing, for US banks and credit unions, with a focus on small and midsize banks. The stock is trading at a 48% discount to our fair value estimate of $126 per share.

Fiserv’s merger with First Data in 2019 kicked off a string of three similar deals that took place in short order. While this deal looked like a winner in recent years, the picture is now more cloudy.

First Data had underperformed its peers prior to the merger, as it was weighed down by an excessive debt load stemming from a leveraged buyout just before the financial crisis and the defection of a major bank partner. We believe this meaningfully limited its ability to reinvest and adapt in an industry that continues to evolve. However, resolving its financial issues put the company back on track. Further, Clover, the company’s small-business solution with similarities to Square’s offering, has boosted growth, with volume running at an annualized rate of over $300 billion. Clover offers much stronger pricing and is the type of platform we think the company needs to maintain and build on its leading position in the industry.

While the company’s performance over the past few years has been quite strong, new CEO Michael Lyons recently announced that he believes the company has been underinvesting and overly focused on boosting near-term growth. As a result, he intends to reset the business. This will necessitate greater investment and lower margins in the near term, along with lower growth. Clover remains the centerpiece of management’s growth plans, but even this business will likely see its revenue growth compress. Management’s One Fiserv’s plan is light on details, but the overall trend is clear. Near-term performance will weaken considerably, and 2026 is likely to be something of a transition year.

The coronavirus pandemic did illustrate one potential negative of the merger: The acquiring business is significantly more macrosensitive than Fiserv’s legacy operations. Over the long term, Fiserv’s acquiring operations (and Clover specifically) should still be the company’s strongest engine for growth. Still, successfully resetting the business could be complicated if the macro environment sours before the new CEO can put the company back on a more stable path.

Brett Horn, Morningstar senior analyst

HubSpot

- Morningstar Price/Fair Value: 0.59

- Morningstar Uncertainty Rating: High

- Morningstar Economic Moat Rating: Narrow

- Industry: Software—Application

HubSpot provides a cloud-based marketing, sales, and customer service software platform referred to as the growth platform. HubSpot is an affordable tech stock, trading at a 41% discount to our fair value estimate of $650 per share. The software application firm earns a narrow moat rating.

We believe HubSpot is a leader in marketing and sales automation software for the midmarket. We see a long runway for growth as it gathers new customers and continues to move its existing clients up a tiered pricing structure and sell multiple hubs to larger clients. We also see the SMB and midmarket as being underserved by enterprise software providers, as the smaller deal sizes make it harder to serve efficiently. Thus, we believe that HubSpot’s robust and expanding suite has helped carve out a defensible niche.

HubSpot provides a suite of software solutions that helps companies grow “better.” Taken together, the five hubs (marketing, sales, service, operations, CMS) combine to create the growth platform. HubSpot operates a “freemium” model that has allowed it to gather hundreds of thousands of free users, with approximately 15% of these moving into paid solutions. From the free version, a three-tiered system emerges, including Starter, Professional, and Enterprise. HubSpot’s goal is to create as a wide a funnel as possible for customer gathering, and then move users up the pricing tier as they evolve, and upsell them to additional hubs as their needs change. Loosely two thirds of annually recurring revenue comes from customers that started as free users, which we think demonstrates successful strategy execution. We think approximately 60% of customers are using multiple hubs. Meanwhile, average revenue per customer has been slowly increasing over time.

While we recognize that churn is typically higher for SMB customers than it is for enterprise customers, we see HubSpot as gradually moving up the curve to serve increasingly larger customers. Over the last several years the company significantly invested in the platform to make it more suitable for customers with up to 2,000 employees. As customer size increases, we think switching costs strengthen, which is impactful, as enterprise customers generate higher revenue and higher retention than SMB customers. We estimate the Enterprise tier makes up approximately 15% of the paying customer mix, which has slowly ticked up over time.

Dan Romanoff, Morningstar senior analyst

Nice

- Morningstar Price/Fair Value: 0.59

- Morningstar Uncertainty Rating: Medium

- Morningstar Economic Moat Rating: Narrow

- Industry: Software—Application

Nice is an enterprise software company that serves the customer engagement and financial crime and compliance markets. Trading 41% below our fair value estimate, Nice has a moat rating of narrow. We think this stock is worth $190 per share.

Nice provides cloud and on-premises software solutions that serve the customer engagement and financial crime and compliance markets. Most of its revenue is generated in the US, but international expansion has become a bigger priority.

The customer engagement segment contributes around 85% of total revenue. It is mainly driven by Nice’s flagship product, CXone Mpower, which is a cloud-native contact-center-as-a-service platform. CXone helps companies manage customer service. It brings together tools for handling phone calls, chats, emails, and social media messages in one place, so contact center agents can assist customers more efficiently. CXone is the world leader in the CCaaS market and is considered to be the most comprehensive platform. Nice’s CXone strategy is focused on winning large enterprise deals, increasing penetration in international markets, expanding reach through strategic partnerships, and continued product innovation, mainly integrating advanced artificial intelligence capabilities.

The company earns about 15% of revenue from its financial crime and compliance business, which provides solutions to help financial institutions detect, prevent, and manage financial crimes (money laundering and fraud) and regulatory compliance. Nice’s strategy is to support financial institutions’ move to the cloud and expand its market reach through its two main cloud platforms, X-Sight and Xceed. X-Sight targets large financial institutions while Xceed is designed for midtier banks and financial institutions. The shift to the cloud has been slow for financial institutions, given their conservative nature and regulatory burdens. However, high switching costs mean this segment earns high margins despite being much smaller than the customer engagement segment.

Rob Hales, Morningstar senior analyst

Monday.com

- Morningstar Price/Fair Value: 0.60

- Morningstar Uncertainty Rating: Very High

- Morningstar Economic Moat Rating: Narrow

- Industry: Software—Application

Monday.com is a work management platform allowing for increased collaboration and visibility across an organization. Monday.com is an affordable tech stock, trading at a 40% discount to our fair value estimate of $241 per share. The software application firm earns a narrow moat rating.

Monday.com seeks to operate as the unified backbone of an organization through its flexible and broad WorkOS platform. The company’s strategy should continue to center on expanding within its enterprise customer base and broadening penetration across newer vertical solutions. Penetration within enterprise accounts remains relatively low, giving the company substantial room for growth and higher retention through deeper product adoption. Additionally, Monday’s horizontal platform approach positions it to compete not only against traditional work management peers but also entrenched incumbents in adjacent categories, expanding its total addressable market. While scaling these newer verticals will take time, we believe the opportunity is significant and should enhance customer stickiness, drive upsell potential, and support durable long-term growth.

Originally, the firm offered a work management solution targeting the greenfield collaboration and project management market. The platform’s flexibility and modular architecture enabled Monday to easily add additional solutions and target additional verticals: customer relationship management, product development, and IT service. These additions supported growth and enhanced its competitive position.

Historically, Monday.com targeted small and midsize businesses, or SMBs, where its intuitive platform resonated with a historically underserved customer base seeking access to flexible and enterprise grade tools. Over the years, it has moved upmarket to larger customers, creating more stability in the revenue base and mitigating some of the volatility inherent in smaller customers. Today, enterprise customers drive greater than one fourth (26%) of annual recurring revenue, which we expect to grow in the coming years.

Monday.com uses a software-as-a-service model, charging customers a monthly per-seat fee. As it has expanded into larger accounts, its go-to-market approach has shifted away from a predominantly product-led, performance marketing motion toward a more traditional enterprise sales model supported by channel partners, allowing for higher service levels, more efficient growth, and stickier relationships.

Alex Medow, Morningstar analyst

Adobe

- Morningstar Price/Fair Value: 0.60

- Morningstar Uncertainty Rating: High

- Morningstar Economic Moat Rating: Wide

- Industry: Software—Application

Adobe provides content creation, document management, and digital marketing and advertising software and services to creative professionals and marketers for creating, managing, delivering, measuring, optimizing, and engaging with compelling content multiple operating systems, devices, and media. The firm earns a wide moat rating, and its stock shares appear 40% undervalued relative to our $560 fair value estimate.

Adobe has come to dominate in content creation software with its iconic Photoshop and Illustrator solutions, both now part of the broader Creative Cloud. Over the years, the firm has added new products and features to the suite through organic development and bolt-on acquisitions to drive the most comprehensive portfolio of tools used in print, digital, and video content creation. The December 2021 launch of Adobe Express helps further broaden the company’s funnel, as it incorporates popular features of the full Creative Cloud but comes in lower-cost and free versions. The 2023 introduction of Firefly marks an important artificial intelligence solution that should also attract new users and help extend the competitive position of the platform. We think Adobe is properly focusing on bringing new users under its umbrella and believe that converting these users will become more important over time.

CEO Shantanu Narayen provided Adobe with another growth leg in 2009 with the acquisition of Omniture, a leading web analytics solution that serves as the foundation of the digital experience segment that Adobe has used as a platform to layer in a variety of other marketing and advertising solutions. Adobe benefits from the natural cross-selling opportunity from Creative Cloud to the business and operational aspects of marketing and advertising.

The Document Cloud is driven by one of Adobe’s first products, Acrobat, and the ubiquitous PDF file format created by the company, and it is now a multibillion-dollar business. The rise of smartphones and tablets, coupled with bring-your-own-device and a mobile workforce have made a file format that is usable on any screen more relevant than ever.

Adobe believes it is attacking an addressable market well in excess of $200 billion. The company is introducing and leveraging features across its various cloud offerings to drive a more cohesive experience, win new clients, upsell users to higher price point solutions, and cross-sell digital media offerings. We expect M&A efforts will continue to bolster all aspects of Adobe’s portfolio, which it surely will do to defend against emerging competitors.

Dan Romanoff, Morningstar senior analyst

Elastic

- Morningstar Price/Fair Value: 0.61

- Morningstar Uncertainty Rating: High

- Morningstar Economic Moat Rating: Narrow

- Industry: Software—Application

Elastic is a software company that specializes in AI-search, observability, and security deployments. The firm earns a narrow moat rating, and its shares appear 39% undervalued relative to our $119 fair value estimate.

Elastic traces its origins to the mid-2000s, with the first open-source code for what would later become “Elasticsearch” written in 2009. Elastic operates in three main segments: AI-search, observability, and security.

Elasticsearch is a search and analytics engine capable of indexing and querying all types of data, including textual, numerical, structured, and unstructured. Elastic supports vector search alongside traditional keyword search, enabling advanced querying and fast retrieval of accurate, context-rich information.

Elastic offers a free open-source version of its software and upsells users to subscription-based software and managed services through Elastic Cloud—available on various cloud platforms—or via self-managed commercial licenses, where customers deploy Elastic’s proprietary software on their own servers. A free open-source version lacks many high-value features, like shard orchestration (automatic data distribution across servers), automated server scaling (adding more servers to maintain performance), cloud-managed data compression, simplified cross-cluster search (across multiple servers and locations), and integrated machine learning models for anomaly detection.

The observability segment collects, correlates, and displays telemetry data (usage metrics and logs). Meanwhile, the security segment uses machine learning for security information and event management, anomaly detection, and automatic responses. AI-search, observability, and security services face intense market competition, but these services are rarely offered on a single unified platform, which sets Elastic apart.

Elastic competes with major hyperscalers in AI-search, but its cloud-neutral approach offers a unique advantage given the widespread trend toward multicloud environments. While Datadog may be preferred for top-tier observability, and CrowdStrike for security, Elastic’s broad capabilities, multicloud flexibility, and the simplicity of Elastic Cloud are likely to continue driving growth in platform adoption.

Mark Giarelli, Morningstar analyst

Globant

- Morningstar Price/Fair Value: 0.62

- Morningstar Uncertainty Rating: High

- Morningstar Economic Moat Rating: Narrow

- Industry: Information Technology Services

Globant is a next-generation IT services company that primarily assists clients with their digital transformation efforts by creating customized software for them. The firm earns a narrow moat rating, and its stock shares appear 38% undervalued relative to our $102 fair value estimate.

Globant, headquartered in Luxembourg but largely based in Latin America, is an information technology services company focused on providing digital transformation and engineering services. It generates revenue mainly by charging clients on a time and materials basis for services such as consulting/advice, customized software development and integration, and quality assurance and testing. Globant is primarily exposed to the media and entertainment and financial services sectors, which each account for around 20% of revenue.

Like many of its peers, Globant’s core strategy is to land and expand—securing big clients and growing revenue in those relationships by increasingly providing these clients more services. Globant’s 10 largest clients account for around a third of group revenue, with the largest, Disney, contributing around 10%. Disney has been a client for over 10 years.

The company is relatively concentrated geographically, with more than half of its revenue generated in North America. The company is now focused on diversifying geographically, particularly in Europe.

Globant’s “studio” delivery model is based on agile project management from employees in nearshore locations. By organizing itself in small units focused on a particular industry or emerging technology (studios), the company develops deep pockets of expertise and can deliver innovative solutions to its clients faster than many of its peers. To best serve a client’s unique digital transformation goals, the flexibility from the iterative nature of agile project management is effective. Furthermore, the nonstandardized nature of these projects requires constant dialog and interaction between Globant and its clients, which means it’s best to have delivery teams with similar time zones to its clients (nearshoring) so as to deliver the project successfully in a timely manner.

Rob Hales, Morningstar senior analyst

Tenable

- Morningstar Price/Fair Value: 0.63

- Morningstar Uncertainty Rating: Very High

- Morningstar Economic Moat Rating: Narrow

- Industry: Software—Infrastructure

Founded in 2002, Tenable is a cybersecurity company that began providing vulnerability management solutions under its Nessus software. Trading 37% below our fair value estimate, Tenable has a moat rating of narrow. We think this stock is worth $36 per share.

We view Tenable as a solid cybersecurity vendor providing vulnerability management and security operations solutions to its clients. The firm’s combined portfolio delivers exposure management, enabling complete assessment of customers’ threat landscape and security posture. We believe this space has a strong growth runway ahead, thereby providing additional uplift to Tenable’s robust demand base. Although Tenable faces stiff competition as it aims to grow its enterprise customer base, we think the firm will continue to benefit from its sticky portfolio.

The cybersecurity space continues to grow in threat complexity and intensity. As firms undergo digital transformations that expand their online footprints, the number of attack vectors is rapidly increasing. In this environment, we see customers opting for vendors that offer multiple security solutions versus point solutions that can inadvertently create data silos. Here, vendors like Tenable can displace point solutions with interoperable modules.

We believe Tenable is well positioned to provide several security needs for its enterprise-leaning customer base across on-premises, cloud, and hybrid environments. Tenable began providing vulnerability management solutions under its Nessus software, designed to help firms identify and mitigate weaknesses in their IT environment. However, given the secular shift toward vendor consolidation, the firm has added exposure management tools that complement its vulnerability management offering, delivered under its TenableOne platform.

While the increase in nefarious activity has induced more cybersecurity spending, it has also brought on intense competition among vendors. Tenable competes with larger, more capitalized vendors such as CrowdStrike as well as similar-sized players such as Qualys. Despite the competition, we are impressed with the firm’s solid retention metrics, showing the stickiness of its products.

Tenable has invested in research and sales to enable its own cloud transition and expand its portfolio. As a result, Tenable’s profitability has suffered. We believe margin compression will alleviate as benefits from investments come to fruition in future years.

Malik Ahmed Khan, Morningstar analyst

Klarna Group

- Morningstar Price/Fair Value: 0.63

- Morningstar Uncertainty Rating: Very High

- Morningstar Economic Moat Rating: Narrow

- Industry: Software—Infrastructure

Klarna is the largest pure-play in the buy now, pay later space. Klarna Group is an affordable tech stock, trading at a 37% discount to our fair value estimate of $45 per share. The software infrastructure firm earns a narrow moat rating.

Klarna has recently signed multiple agreements with payment services providers, which will significantly broaden its reach as a payment method this year and in the years to come. Growth is what it is all about for Klarna. Its platform is just breaking even, starting to eke out a marginal operating profit, but as its platform ramps up further and its underwriting models are fed more data on shopper behaviors, we think Klarna will turn itself into a profitable staple among fintechs globally.

The PSP agreements will drive a step-up in volume growth and allow Klarna to upsell merchants to its customer conversion tools over time. We are positive on this strategy, as it brings growth at a low margin, but rapid and massive scale, with the upside of growth on the merchant and customer side.

Its growth ambitions focus primarily on the US, a large, homogenous market that is receptive to credit products. That said, Klarna is facing tougher competition in this market already, primarily from card-issuing banks that retain customers through lucrative reward programs. However, Klarna’s buy now, pay later solutions are not a one-to-one equivalent to credit cards. We expect more affluent shoppers to start using Klarna as it grows its visibility on merchants’ checkout pages. More shoppers will start using Klarna as a payment method, feeding Klarna’s network effect.

Its funding profile, using retail deposits to fund its European balance sheet, is a unique feature of Klarna. We think it improves Klarna’s stability. Outside of Europe, we think obtaining local banking licenses is a desirable outcome, but it’s not an easy ask. Convincing regulators of Klarna’s stability and ability to protect depositors will be a long endeavor.

Niklas Kammer, Morningstar analyst

Akamai Technologies

- Morningstar Price/Fair Value: 0.65

- Morningstar Uncertainty Rating: Medium

- Morningstar Economic Moat Rating: Narrow

- Industry: Software—Infrastructure

Software infrastructure firm Akamai Technologies rounds out our list of best tech stocks to buy. Akamai operates a content delivery network, which entails locating servers at the edges of networks so its customers, which store content on Akamai servers, can reach their own customers faster, more securely, and with better quality. The stock is 35% undervalued relative to our fair value estimate of $130 per share.

Akamai has successfully repositioned itself to benefit from trends such as the increasing need for cybersecurity and edge computing. Its legacy content delivery network may be the firm’s foundation, but it only accounts for a third of revenue today. We think continued growth in its security and computing businesses will drive incremental value for the firm and strengthen its competitive positioning.

The CDN industry continues to face pricing pressure, primarily as major media companies and hyperscalers—once major customers of Akamai—have created their own networks in the wake of growing internet traffic. With the foresight to these intensifying competitive pressures, management began investing over a decade ago outside of the CDN business and into security, which has grown to over 50% of sales compared with only 12% in 2015. Most of Akamai’s CDN customers now subscribe to at least one security solution, with a growing proportion of customers utilizing multiple security offerings. Content delivery and security work in tandem: Akamai’s CDN business provides a large market of potential customers for its security business, while security enhances the value and reduces churn of its CDN business.

More recently, Akamai began investing in its cloud computing business. Through its 2022 acquisition of Linode, a developer-friendly cloud infrastructure business, Akamai has extended its dense, distributed network to capitalize on the growing demand for cloud computing. Although competition will remain stiff, particularly as it goes up against the major hyperscalers, we think Akamai’s differentiated and distributed network, with over 4,300 points of presence, will allow the firm to capitalize on the growing demand for edge computing, mainly as 5G enhances networking capabilities at the edge of networks.

Although CDN will likely remain in secular decline, we think it remains an essential launching pad for newer segments. Content delivery provides a baseline of customers and infrastructure the firm can capitalize on, particularly in its security and computing businesses. We believe security and computing will enhance customer stickiness and drive growth through our forecast.

Mark Giarelli, Morningstar analyst

Access this research and more at Morningstar. For a free four-week trial, click here.

All prices and analysis at 5 January 2026. This information has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892.). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.