CSL: Value or value trap?

Shane Ponraj, CFA | Morningstar

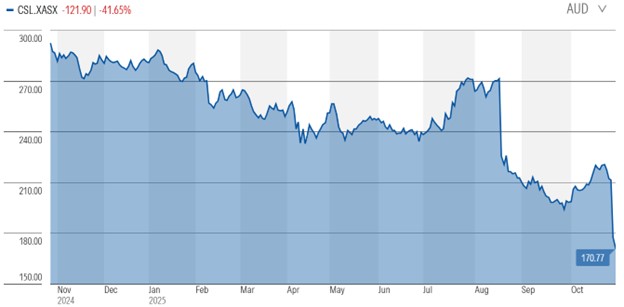

CSL (ASX: CSL) cut its fiscal 2026 guidance for revenue and net profit after tax before amortization growth to 3% and 6% at the midpoint, respectively, from 5% and 9%. This was driven by declines in US immunization, with the firm also delaying its plan to demerge the Seqirus vaccines arm. Shares fell 15%.

Why it matters

We cut our EBIT forecasts by 3% on average, largely due to softer influenza vaccination rates in the US than we expected. The impact is limited, with Seqirus contributing less than 15% of group earnings. We expect vaccination rates to largely stabilize by fiscal 2028.

- We see a return to growth as health practitioners drive rates. Vaccine declines were inevitable after the pandemic boom, but infections remain high. We expect the US administration to maintain its positive recommendation of influenza vaccines, with efficacy supported by clinical trial evidence.

- CSL no longer targets June 2026 to demerge Seqirus, but is waiting until the US influenza vaccine market improves. We expect Seqirus to outperform broader industry declines as it prepares launches in new geographies and approaches 20% market share in the fast-growing pediatric market.

The bottom line

We cut our fair value estimate for narrow-moat CSL by 3% to AUD 295 as we expect stabilization of Seqirus to take longer. However, shares are undervalued as we expect margins to rebound on plasma efficiency initiatives that are on track and yet to flow through.

- We forecast plasma gross margins recover 600 basis points to 57% by fiscal 2028. We expect 80% of this uplift from recent initiatives enabling faster and larger collections, and the rest from a favorable sales mix shift as higher-margin products offer greater convenience and take market share.

- Our forecast 10-year revenue compound annual growth rate of 6% is largely driven by our 10-year immunoglobulin revenue CAGR of 8%. Long-term demand for Ig is driven by improving diagnosis rates for immunodeficiencies and is largely safe from competition.

Source: Morningstar

Demand for CSL’s plasma products persists as supply improves

CSL is one of three Tier 1 plasma therapy companies that benefit from an oligopoly in a highly consolidated market. All the players are vertically integrated as plasma sourcing is a key constraint in production. The plasma sourcing market is currently in short supply, however, CSL is well positioned having invested significantly in plasma collection centers, owning roughly 30% of collection centers globally.

One major threat to plasma products is recombinant products. Recombinants are quickly replacing plasma products in haemophilia treatment despite being more expensive. CSL has an excellent R&D track record and has developed recombinant products for haemophilia. However, we expect revenue growth to slow in the haemophilia segment based on competitor Roche’s successful launch of recombinant Hemlibra.

Immunoglobulin product sales are key to CSL. The use of immunoglobulins is currently growing due to improved diagnosis, rising affordability, and gaining approval for increased indications. This market is not yet impacted by recombinants although both CSL and competitors are pursuing R&D in Fc receptor-targeting therapy to treat autoimmune diseases.

However, gene therapy represents the biggest risk to the plasma industry as it aims to cure rather than treat diseases. While the potentially prohibitive cost may result in slow adoption, CSL has strategically expanded its scope via the acquisition of Calimmune in fiscal 2018 and licensing a late stage Haemophilia B gene therapy, Hemgenix, from UniQure in fiscal 2020.

CSL is the second largest influenza vaccine manufacturer, behind Sanofi, and is on the forefront of changes in influenza vaccines where manufacturing is shifting from egg-based to cell-based culturing. It’s also conducting preclinical testing of mRNA influenza vaccines.

The company has demonstrated good sense for R&D and evaluates spend based on the commercial outlook. The strategy for CSL Behring has been to target rare diseases, a typically low volume and high price and margin business. There is little reimbursement risk in this area or in the vaccine business, Seqirus.

Bulls say

- CSL is investing in both physical capacity and R&D, leaving it well positioned to take advantage of growth opportunities in the key immunoglobulins market.

- The acquisition of Calimmune’s gene therapy platform in fiscal 2018 and UniQure’s late stage haemophilia B gene therapy candidate in fiscal 2020 will help defend against emerging competition.

- CSL has a strong R&D track record and the ongoing rate of investment is ahead of major competitors.

Bears say

- Areas of the plasma industry could be replaced by newer therapies, which would leave CSL overinvested in plasma collection and fractionation capacity that will be hard to repurpose.

- Key segments of haemophilia and hereditary angioedema are currently facing competitive pressure from Roche’s Hemlibra and Takeda’s Takhzyro that offer more convenient delivery.

- The R&D pipeline has a highly variable range of outcomes and R&D spending could ultimately amount to nothing.

Access this research and more at Morningstar. For a free four-week trial, click here.

All prices and analysis at 29 October 2025. This information has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892.). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.