Is Xero becoming the highest quality company on the ASX?

Michael Teran | Blackwattle Investment Partners

"Institutions of greatness can't be built quickly. You can't be great quickly, great takes time."

Mitch Rales, co-founder of Danaher Corp (DHR.US 21% TSR CAGR since 1980).

FY24 Result

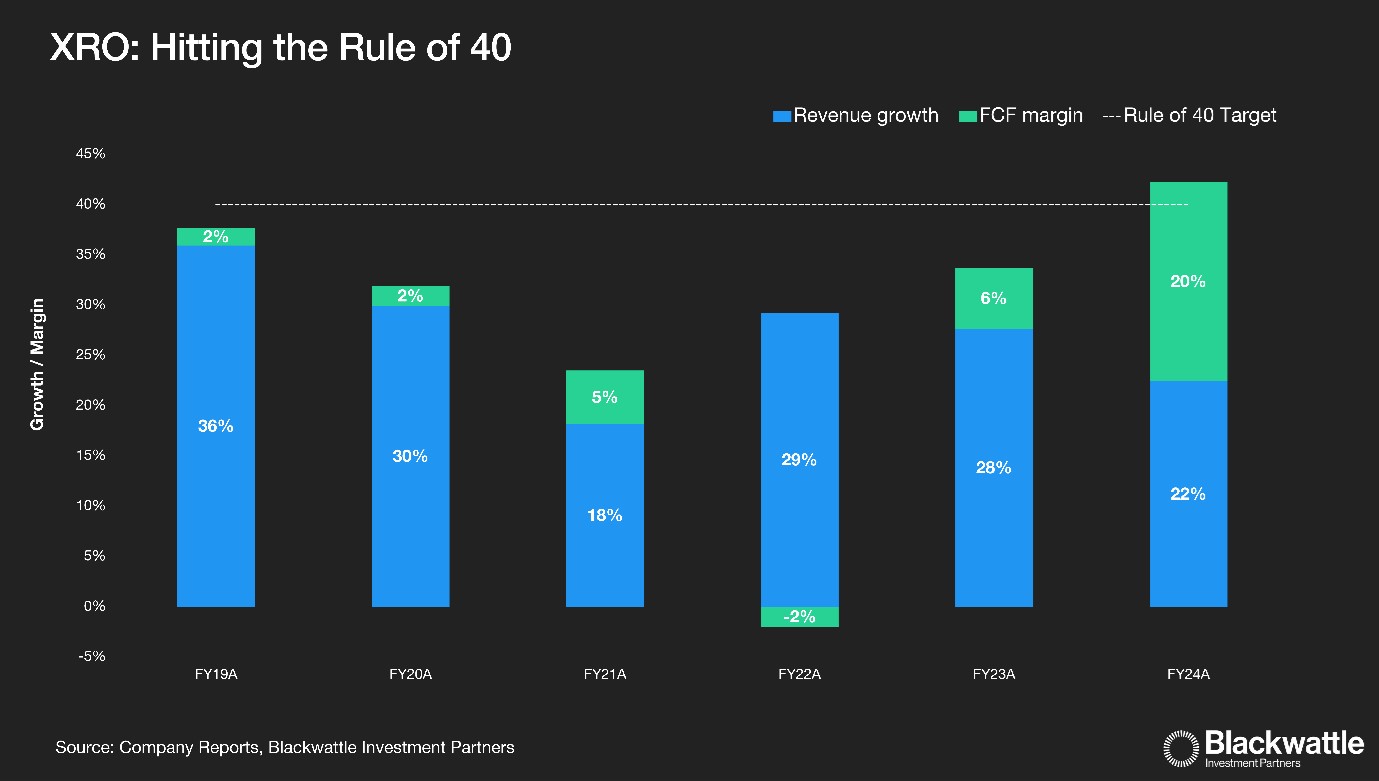

The FY24 result in late May demonstrated the financial strength of the business, following the important cultural pivot to balance top-line growth with profitability, undertaken by CEO Singh-Cassidy since early 2023. The result achieved the aspiration of the Rule of 40 (R40 = sales growth + free cash flow margin) well ahead of the market’s expectations.

The extent of the profitability pivot caught the market by surprise.

The extent of the profitability pivot caught the market by surprise.

Rule of X

Looking forward, management discussed with investors a desire to shift towards the 'Rule of X’. This measure is an evolution of the R40, where profitable growth is valued at a premium to FCF margin given the long-term compounding benefits. We believe this is a signal from XRO that now that the business’s profitability has been structurally enhanced, XRO can now selectively reinvest FCF when there is an appropriate return opportunity.

We expect XRO to either improve top line growth or maintain strong FCF margins, depending on the opportunity available.

Growth aspirations

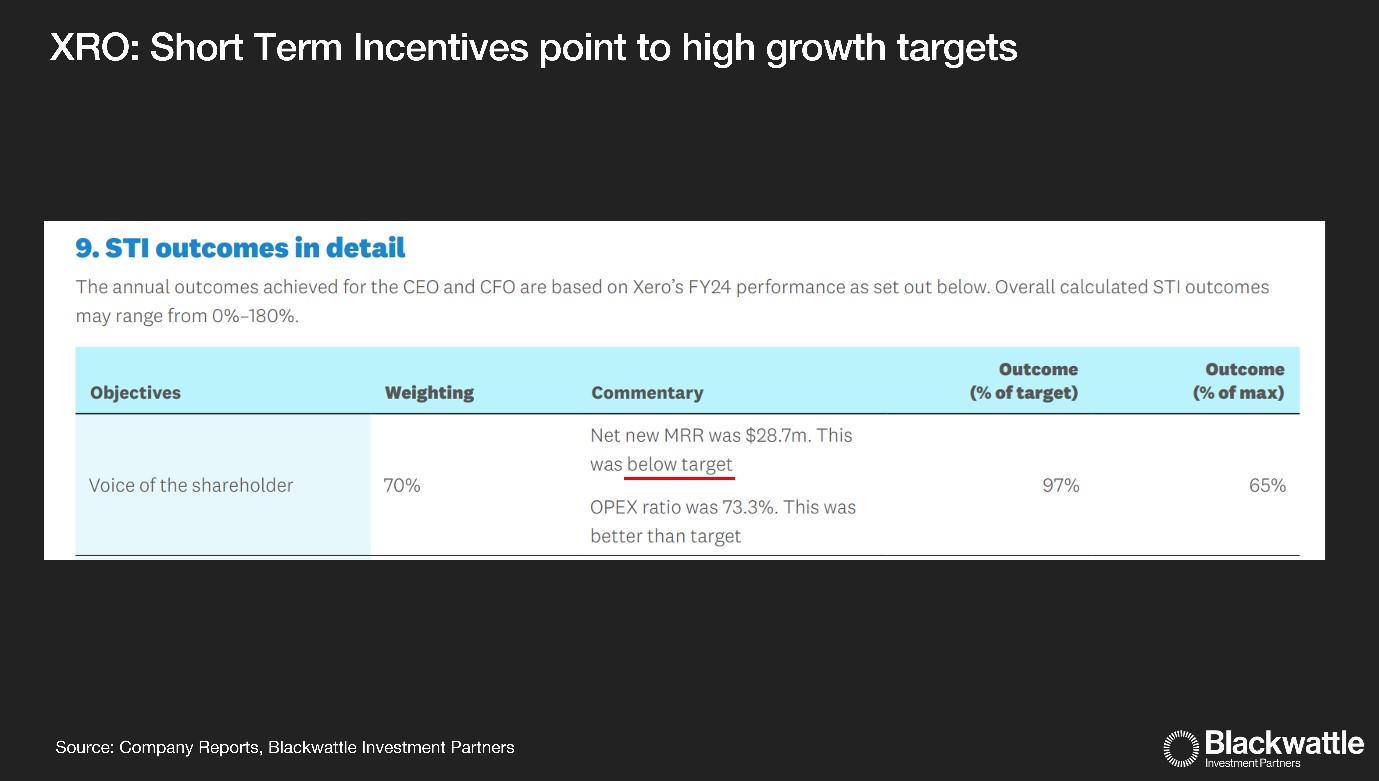

At the Investor Day in February, management talked about their aspiration of doubling revenue from FY23. As no timeframe was given, a key question is when XRO could achieve this ambition. Market expectations is for this to occur in 4-5 years (FY27 to FY28), which we believe to be conservative. A data point on possible short term growth rates was revealed on page 125 of the FY24 annual report. Short Term Incentives (STI) for FY24 for the CEO and CFO were not granted with relation to the net new Monthly Recurring Revenue (MRR) target. Whilst XRO does not disclose future growth targets, we believe a similar target growth rate for FY25 onwards is reasonable, meaning a target of more than the FY24 growth rate of 22% is likely.

XRO achieving this level of top-line growth would be well above consensus expectations, which have fading growth rates from FY25 onwards.

Hands up who made it to page 125 of the annual report?

Hands up who made it to page 125 of the annual report?

Growth drivers

We see multiple levers for XRO to generate higher-for-longer top-line growth rates, enabled by their structurally improved profitability. XRO’s market leading products and continuous product reinvestment should enable further subscriber growth globally. XRO is also looking to enhance natural subscriber growth by selectively investing in optimised promotions to take further market share.

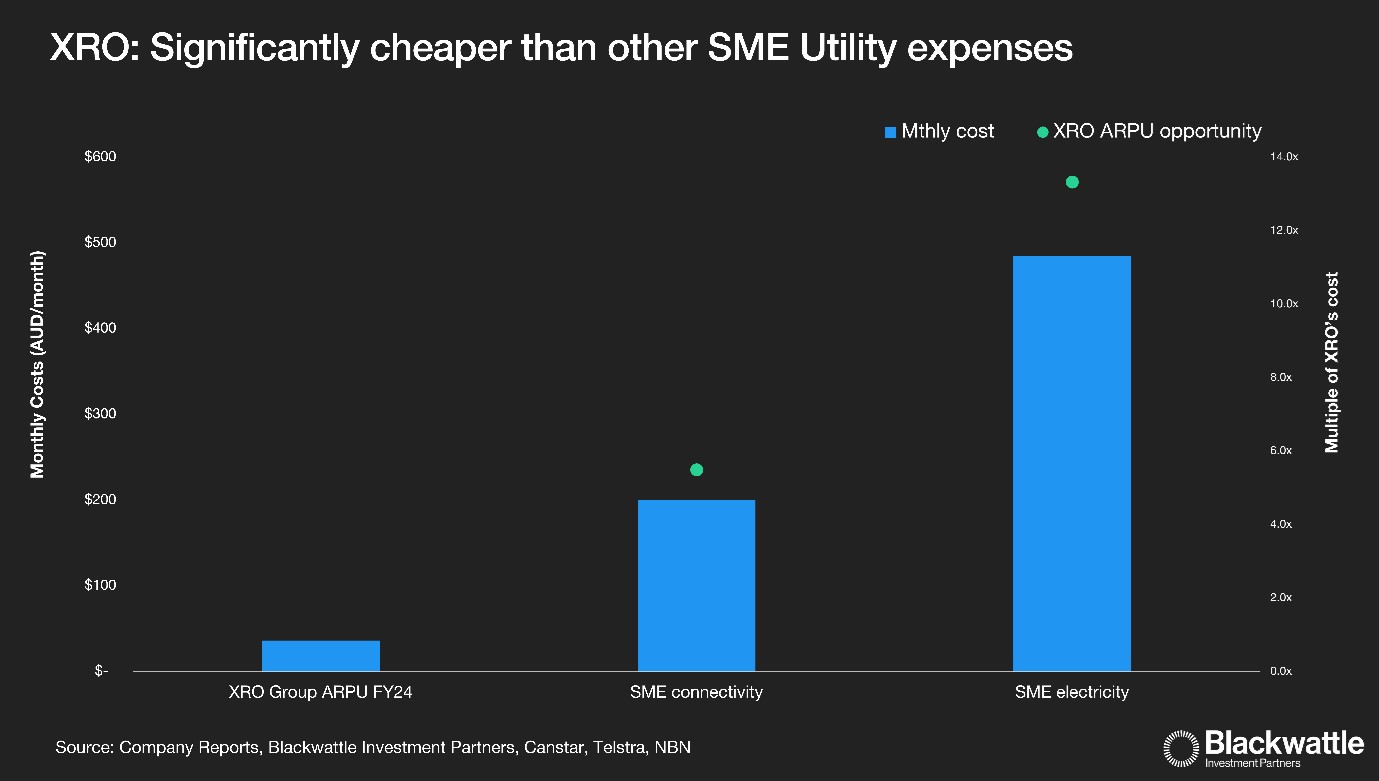

However, for us the bigger opportunity for top line growth is improving the Average Revenue per User (ARPU) on XRO’s already large, 4.2m global subscriber base.

We believe XRO have significant latent APRU growth capacity over many years, through a mix of upselling customers with products (payroll, payments etc.) and outright price increases. We compare XRO monthly cost with average Australian SME utilities including power and telecommunications. The comparison is highly favourable for XRO supporting the theory that there is ample latent ARPU capacity in XRO subscription prices if XRO’s products improve productivity for SMEs over time. This is not something that will change quickly, however the ceiling is in some cases many multiples higher than current subscription prices.

XRO has significant price headroom compared to other SME utility costs.

XRO has significant price headroom compared to other SME utility costs.

Maintaining financial strength

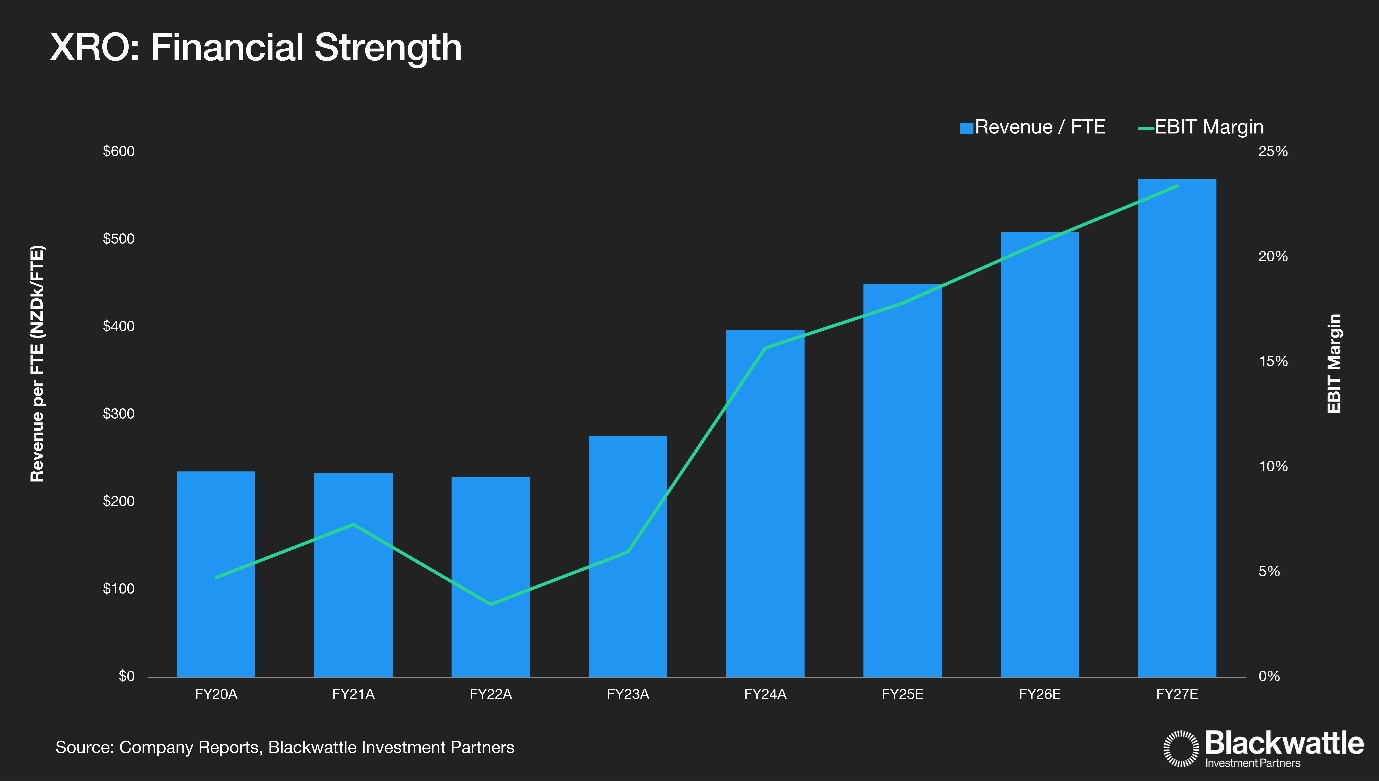

A key driver to XRO’s improved cost base in FY24 was the restructuring program in late FY23, reducing headcount by ~15%. We have continued to monitor XRO’s hiring intentions. Whilst overall employee numbers climb, the growth rate is moderate and focussed on key productive departments such as product development and AI. This is a distinct change compared to XRO’s pre-profitability days, where headcount grew over 20% p.a. and mostly for non-technical roles. XRO have also stated that there will be a continuous productivity focus, measured by revenue per employee.

Together with strong pricing growth, we see further material margin expansion over time.

XRO has shown a clear structural shift from pre-FY23 employee productivity.

XRO has shown a clear structural shift from pre-FY23 employee productivity.

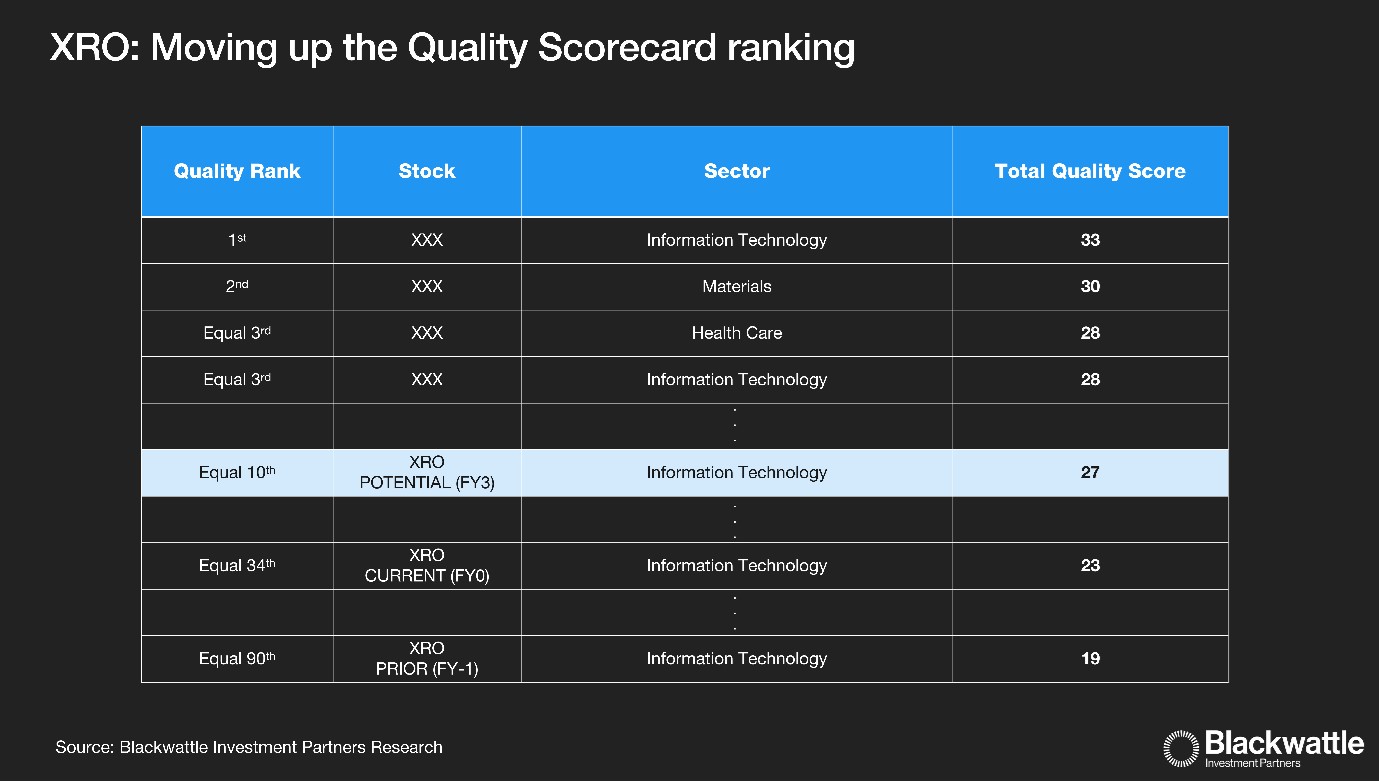

Becoming one of the highest quality companies on the ASX

In the past 2 years, XRO has powered up the rankings on our proprietary Quality Scorecard Tool, which generates a Quality Score based on multiple quality criteria. XRO now sits firmly in the top quartile of high-quality businesses on the ASX, and if XRO can continue to execute towards our expectations, we forecast XRO’s Quality Score to take XRO to the top decile of the rankings in 3 years.

XRO is finally realising its significant latent potential as a high-quality business.

XRO is finally realising its significant latent potential as a high-quality business.

We continue to look forward to following XRO on its journey to becoming one of the highest quality companies on the ASX.

This wire was co-authored by Tim Riordan and Michael Teran.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 13 June 2024. This document was originally published in Livewire Markets on 13 June 2024. This information has been prepared by Blackwattle Investment Partners (ABN 24 663 839 094)( AFSL 547 617). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.