Iron Ore faces long-term challenges, but two companies remain attractive

Greg Burke | Wilsons Advisory

Risks are skewed to the downside for iron ore prices in FY25, while the long-term outlook for iron ore demand is clouded by structural headwinds within China’s property market.

However, Australia’s iron ore miners are some of the highest quality producers in the world, and there are fundamental reasons to remain invested selectively within the sector, including Australia’s low position on the cost curve and the sector's reinvestment of iron ore profits into ‘future facing’ commodities.

Our preferred exposures are BHP (ASX: BHP) and Mineral Resources (ASX: MIN), which are explored in this report.

Risks skewed to the downside

China’s housing market and steel demand remains subdued

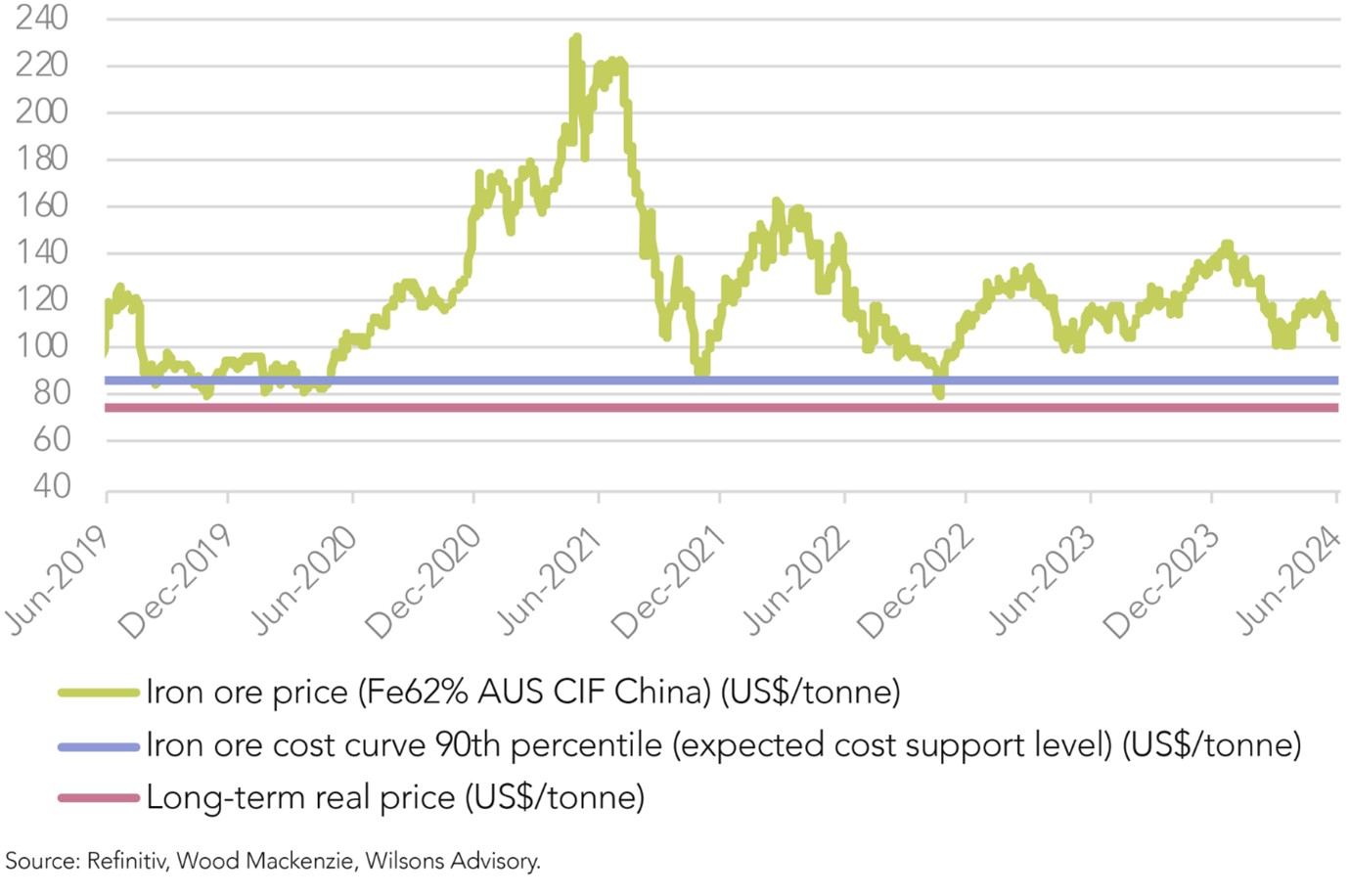

The iron ore price has remained above its long-term average over the last 12 months as weakness in China’s property market has been offset by strong steel exports, infrastructure and manufacturing investment, and measured stimulus efforts.

Nevertheless, the near-term outlook for iron ore demand remains subdued due to soft domestic steel demand from China’s property and construction sectors, combined with uncertainty around China’s future stimulus plans.

While China has announced stimulus to support its struggling property sector (cuts to mortgage rates, loans to local governments to buy unsold homes), aggregate steel (and hence iron ore) demand remains subdued, and structural imbalances within China’s property sector are an ongoing challenge (more on this below).

Figure 1: Iron ore prices have been range bound since 2022

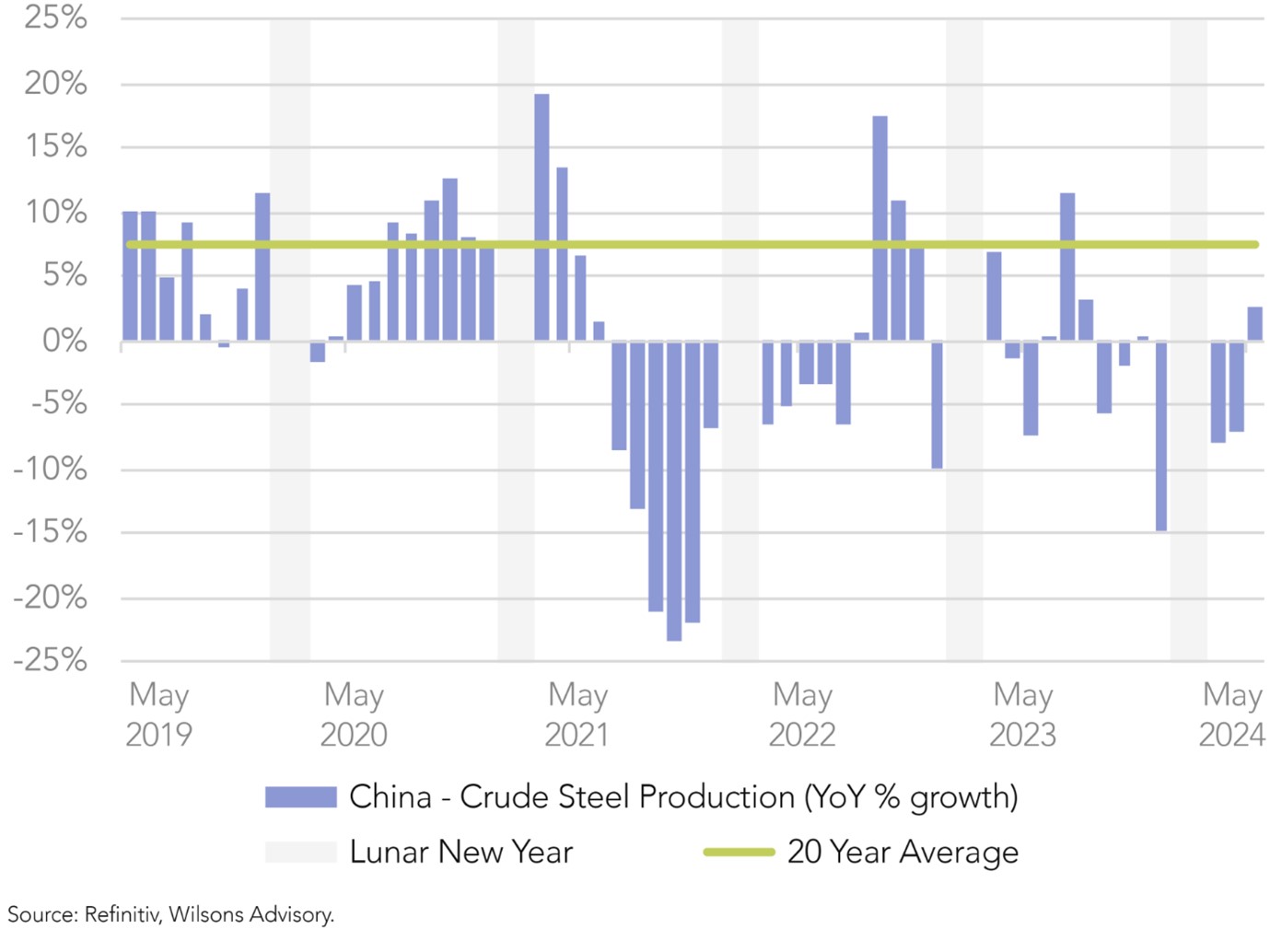

Figure 2: China’s steel industry remains subdued

Iron ore prices - risks are skewed to the downside in FY25

Everything considered, given ongoing weakness in China’s property market, risks are skewed to the downside for the iron ore price over the medium-term.

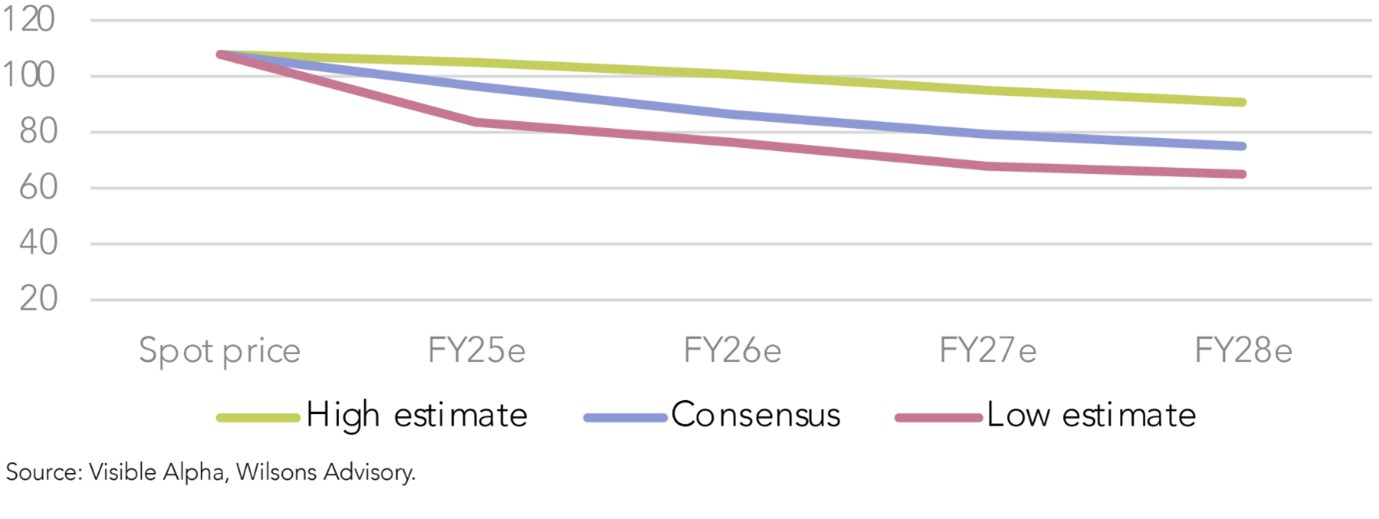

Forecasts for the balance of the 2024 calendar year range from US$110-90/tonne. In line with our thinking, the consensus of analyst estimates point to a moderately lower iron ore price in FY25 (consensus of ~US$96 vs spot of ~US$107).

With that being said, iron ore should find cost support around ~US$80-90/tonne, noting Wood Mackenzie’s latest global cost curve shows the 90th percentile of iron ore producers operate at a cash cost of US$86/tonne.

Over the last five years the iron ore price has consistently found cost support at ~US$80/tonne.

Figure 3: Consensus expectations are for iron ore prices to drift lower over the medium-term

Long term outlook - Iron Ore has a China problem

The long-term demand outlook for the steel (and hence iron ore) is clouded by structural imbalances in China’s property market and the country’s desire to transition towards a modern, consumption-centred economy.

After two decades of rapid growth in steel demand driven by property construction and infrastructure investment, China’s future growth in steel demand is unlikely to match the levels witnessed historically. The World Steel Association forecasts 1-2% global demand growth over the next decade.

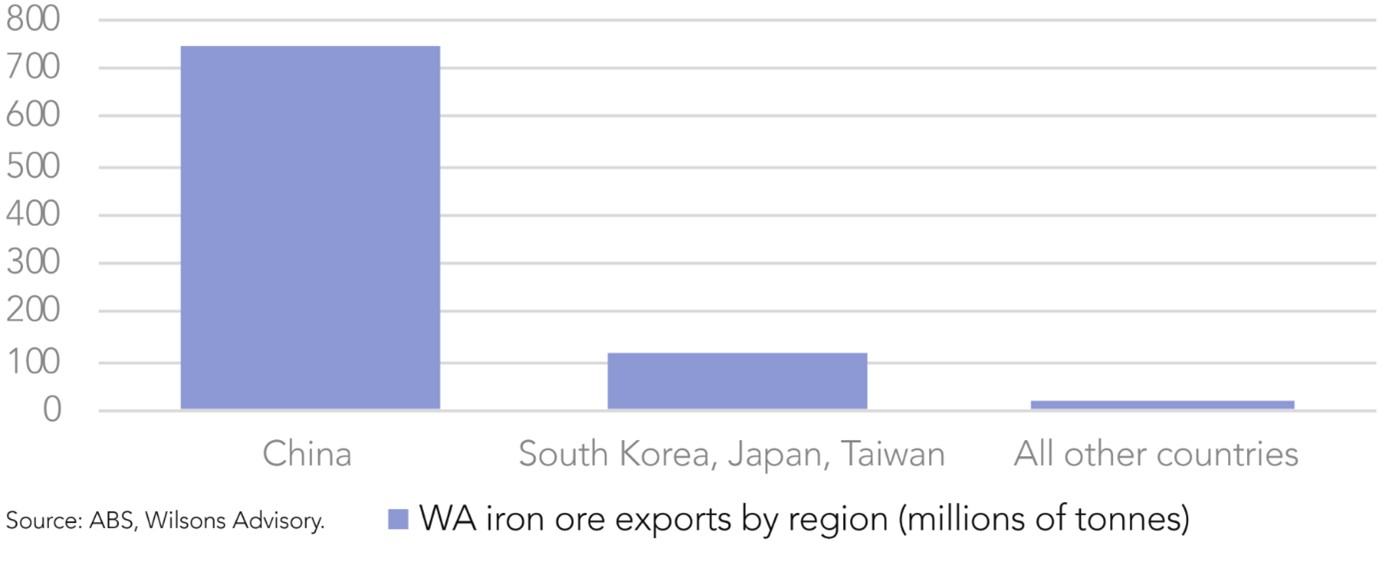

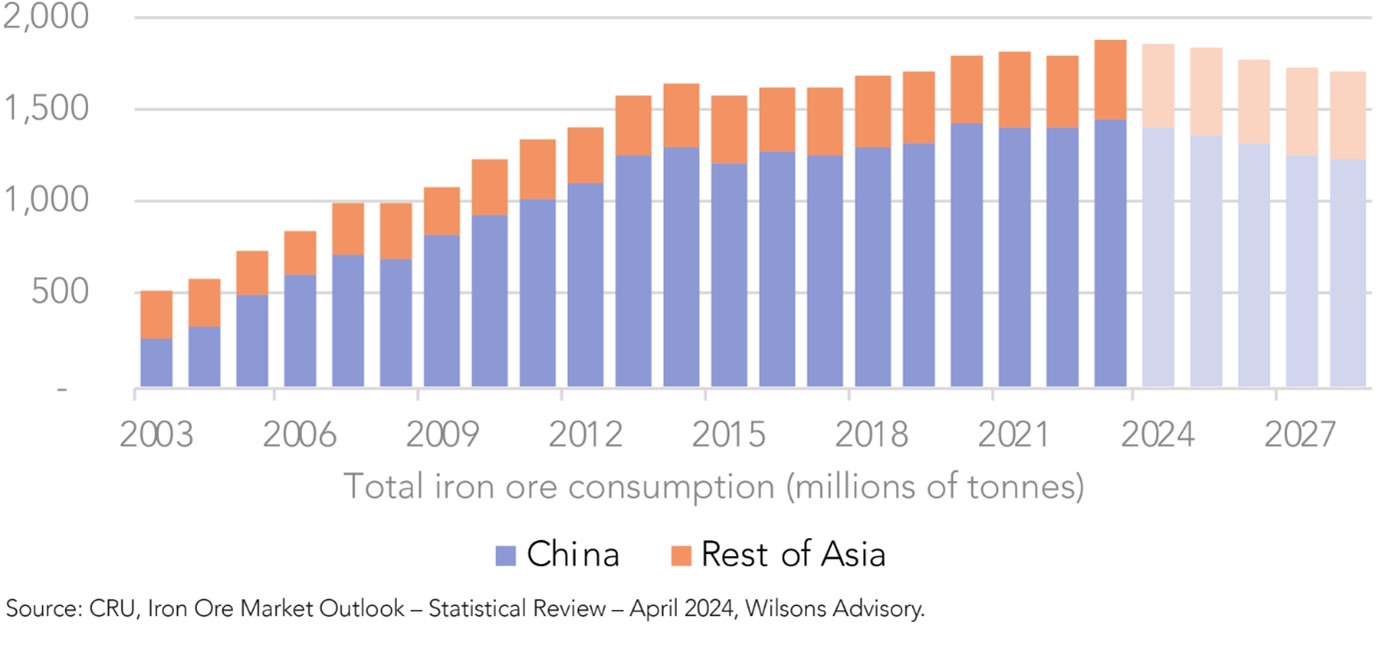

Figure 4: China is by far the world’s largest importer of iron ore

Structural pressures on China's housing market are weighing on steel demand

China’s property sector is key to iron ore demand as it accounts for ~30% of its domestic steel consumption.

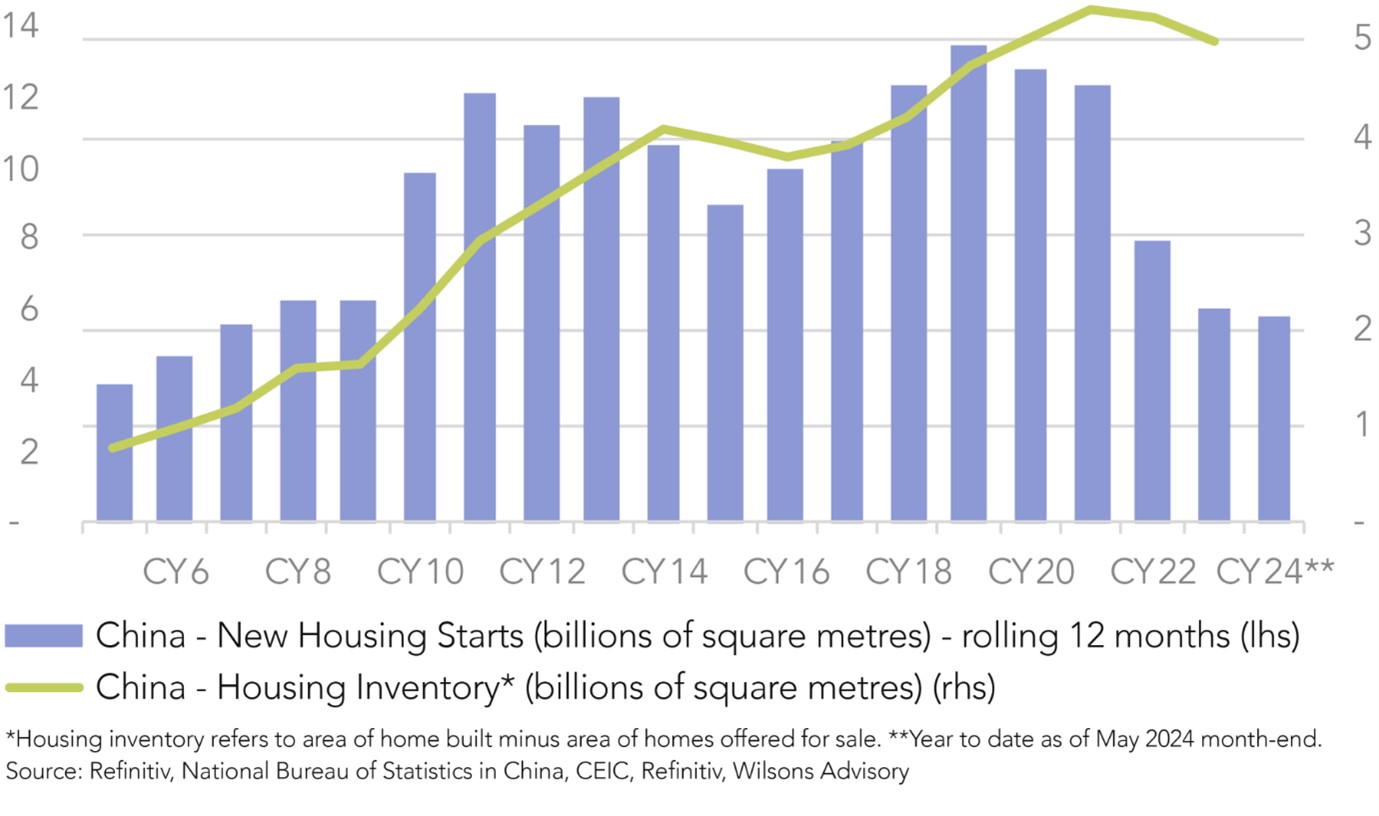

The country’s housing market is under significant pressure amidst falling house prices, weak new home sales volumes, and depressed construction activity. Demand for new housing in China is set to drop by ~50% over the next decade according to the IMF, driven by:

- Housing oversupply – after years of speculative housing construction from heavily indebted developers, there is a mismatch of supply/demand. China now has excess housing inventory of nearly five billion square metres, which is enough to house 150 million people.

- Loss of confidence – following the bursting of China’s property bubble and several high-profile developer bankruptcies, there is little confidence in the housing market from home buyers and investors which is weighing on new home sales.

- Population crisis – China’s population is expected to decline by ~100 million people by 2050 according to the UN, which will negatively impact future housing demand.

While China has signalled its intention to stabilise the property market with measured stimulus, this is being delicately balanced with the desire to transition towards a consumer-centred economy.

Overall, we expect structural pressures on housing to weigh on China’s construction activity and hence global steel demand over the medium and long-term.

Figure 5: Weak housing starts and elevated inventories in China augurs poorly for future steel demand…

Figure 6: …which is expected to drive weaker Asian demand for iron ore

Soft medium-term supply/demand outlook

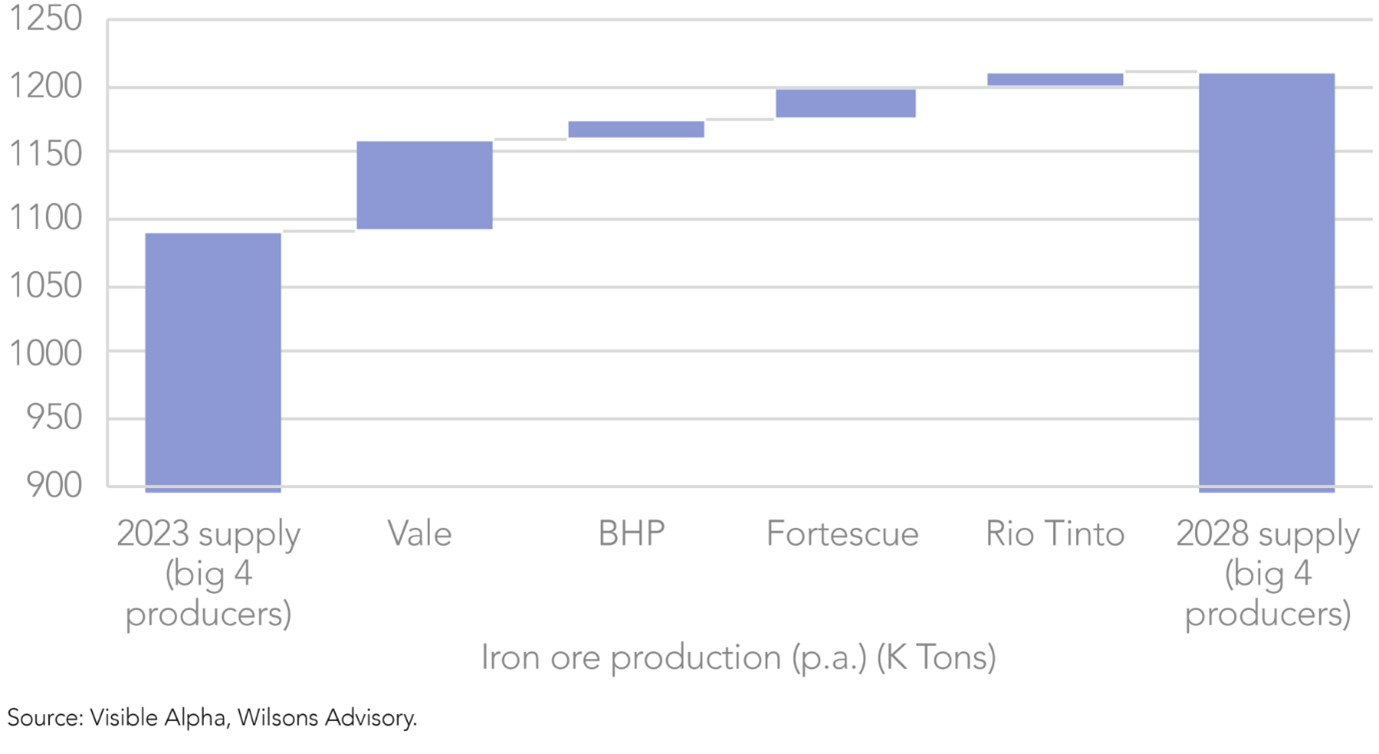

Global iron ore production is poised to moderately increase over the medium-term. Supply growth will be led by Brazilian major, Vale, as it progresses on its key expansion projects.

In combination, the challenged demand outlook and moderate supply growth together is likely to underpin a moderation in iron ore prices over time, which is reflected in consensus estimates.

Figure 7: Vale will drive global supply growth over the medium-term

Retaining selective Iron Ore exposures

While iron ore faces long-term headwinds, Australia’s iron ore majors are among the lowest cost producers in the world (with average total cash costs of ~US$40/tonne), which underpins significant profitability even at considerably lower iron ore prices.

Another key appeal of the sector is that robust iron ore profits are increasingly being reinvested by the major producers into ‘future facing’ commodities with stronger structural outlooks (i.e. copper, lithium).

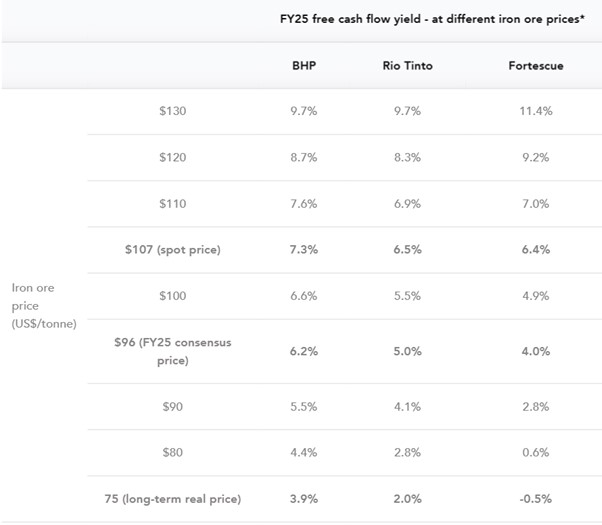

Figure 8: Major iron ore producer valuations - BHP offers the best free cash flow yield under most iron ore price assumptions

*Analysis is based on a number of assumptions for costs/production, and assumes other commodities (excluding iron ore) remain at spot prices through FY25. Analysis is based on ASX share classes (in AUD terms). Source: Refinitiv, Visible Alpha, Wilsons Advisory. Data is accurate as of 17/06/2024 market close.

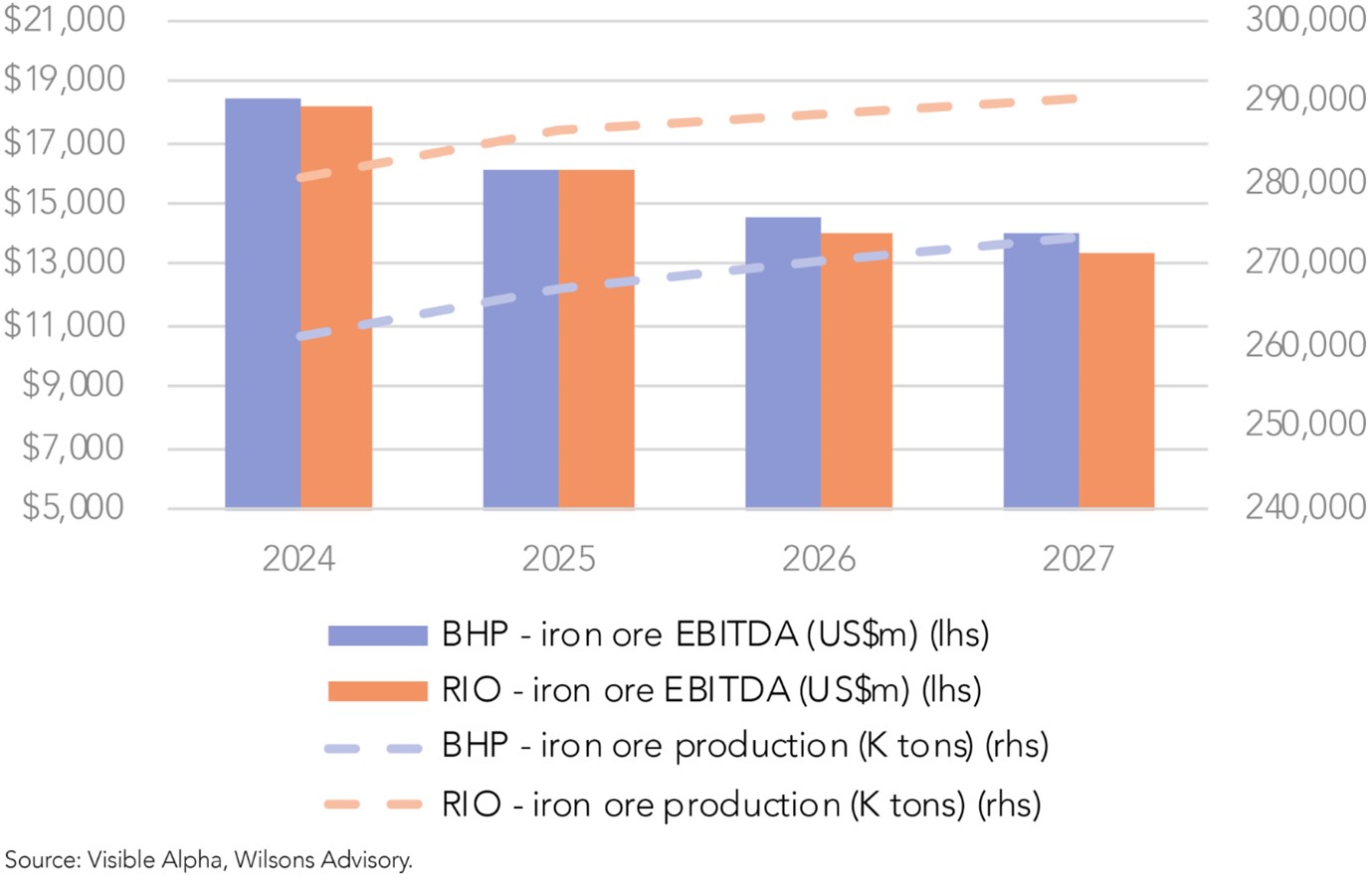

BHP still preferred over Rio Tinto

Our focus within the iron ore sector is on the largest, lowest cost producers: BHP and Rio Tinto (ASX: RIO).

In addition to its attractive relative valuation, BHP remains our preference over RIO for two key reasons.

1. Lowest cost and capital intensity

BHP is the lowest cost iron ore producer in Australia, with unit costs of US$18/tonne compared to RIO at US$23/tonne, and a medium-term target of US$<17/tonne compared to RIO's target of US$20/tonne.

Moreover, RIO is in a heavy investment phase with significantly more capex planned to replace asset depletion. As a result, BHP is poised to deliver higher iron ore profits / free cash flows than RIO over the next decade.

Figure 9: BHP is expected to generate more iron ore profits from less production

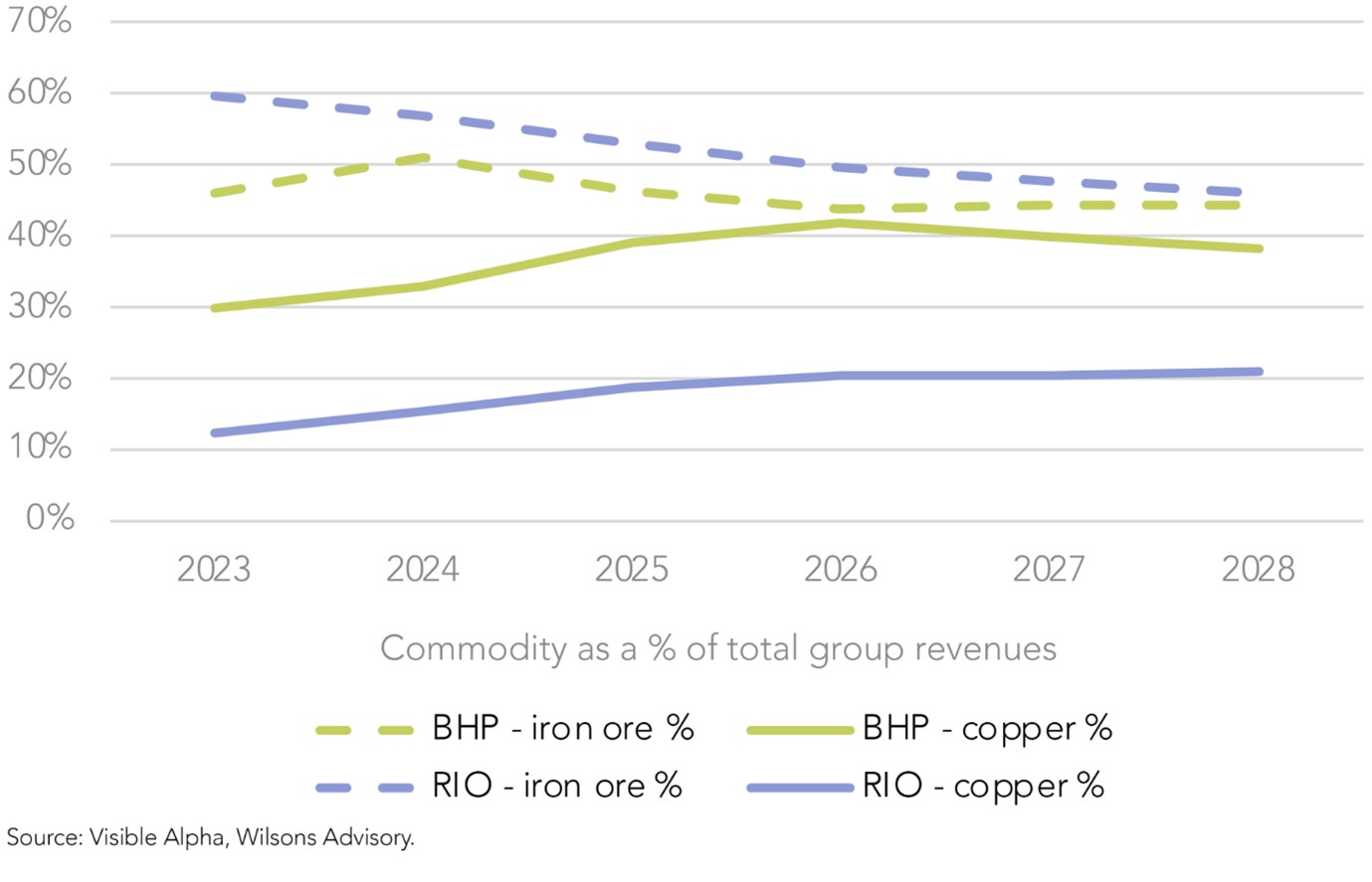

2. Most diversified asset base, superior copper exposure

BHP is more diversified than RIO, with significantly more exposure to copper. This is a key appeal of BHP given the positive structural supply/demand outlook of the metal driven by the energy transition.

Read Dr Copper’s Healthy Prognosis

Figure 10: BHP has significant leverage to copper

Mineral Resources (MIN) – Transitioning into a low-cost producer

The company offers diversified exposure to iron ore (~57% of FY25e revenues), as well as lithium (~24% of FY25e revenues) and mining services (~19% of FY25e revenues excluding intersegment).

Key appeals of MIN include its commodity diversification, as well as its high-quality mining services segment which generates ‘annuity-like’, contracted earnings from tier 1 miners.

With respect to iron ore specifically, we are attracted to MIN for two key reasons:

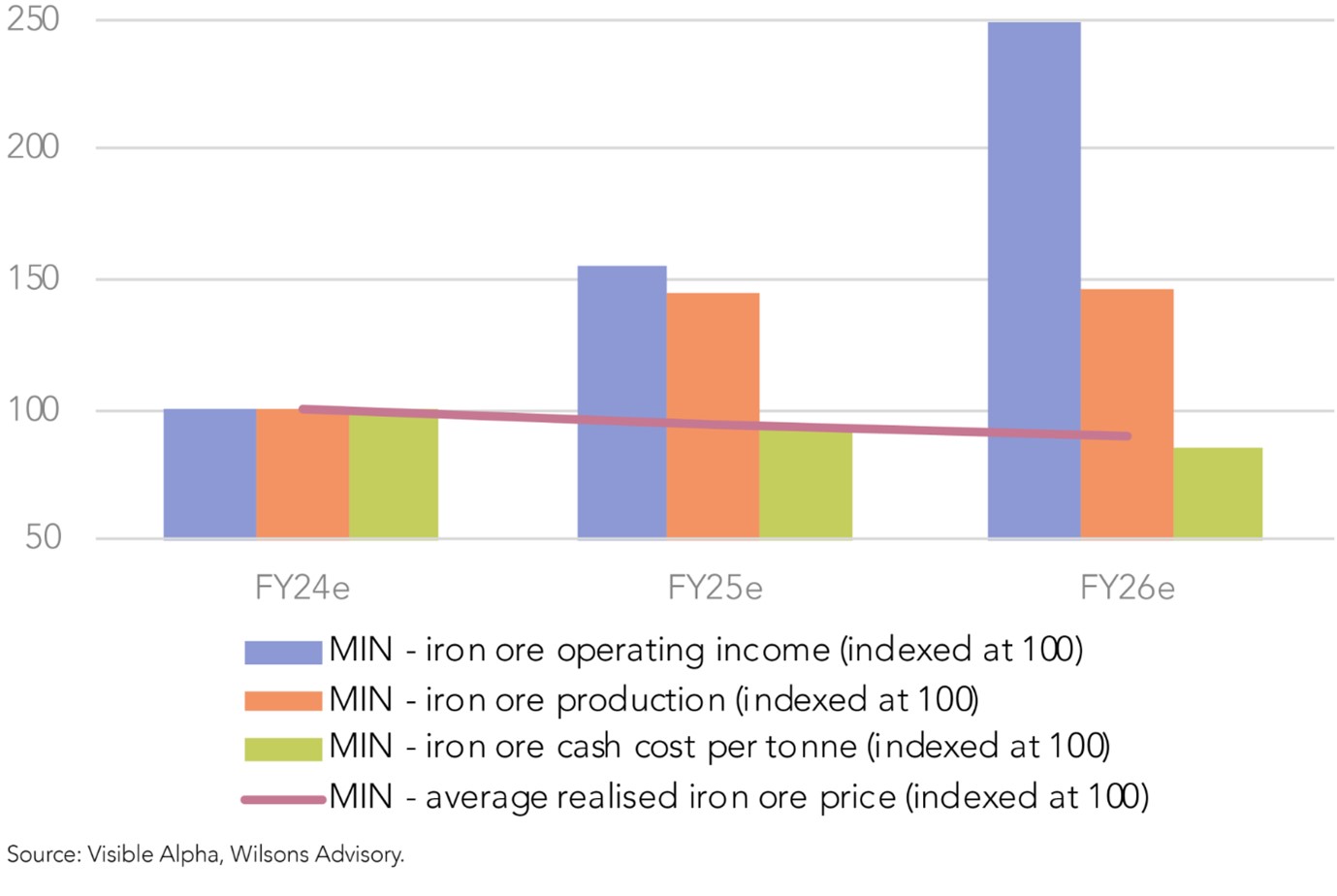

1. Strong production growth

After significant investment into Onslow Iron, the project achieved its first ore shipment last month. This project will be the key driver of MIN’s iron ore production growth and hence earnings growth over the medium-term.

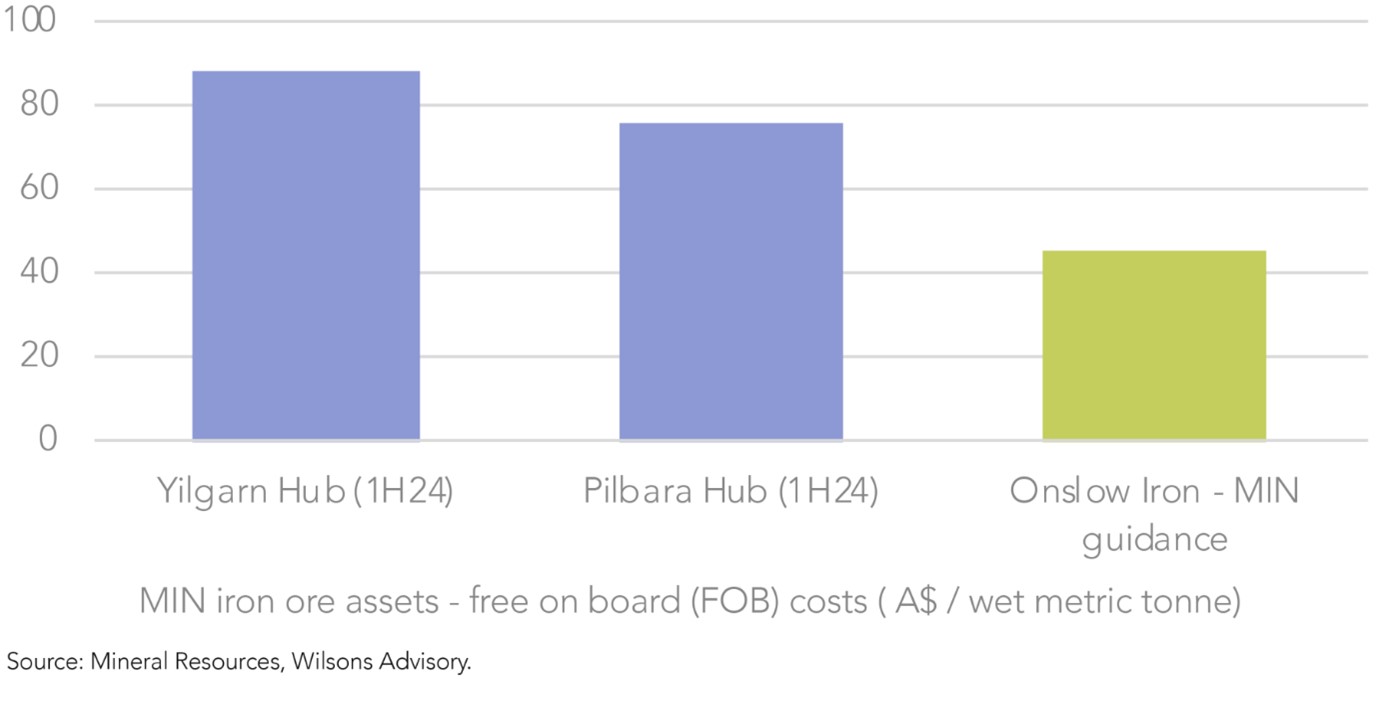

2. Lower cost, higher quality operations

At nameplate capacity, Onslow Iron will be significantly lower cost than MIN’s existing producing assets. The project will transition MIN into a more profitable iron ore producer with greater protection from the commodity cycle.

Figure 11: Onslow Iron will transition MIN into a low-cost, long-life iron ore producer

Figure 12: The ramp up of low-cost production at Onslow Iron will drive substantial earnings growth (even with lower iron ore prices)

Closing Thoughts on Iron Ore

While iron ore faces long-term headwinds from structural pressures on China’s housing market and the transition of China’s economy towards a consumption-centred model, the commodity remains a critical input into buildings, infrastructure, machinery, and the automotive/transportation sectors.

There is still merit to selectively investing in the sector given Australia’s iron ore majors are among the most profitable producers in the world and considering the attractive ‘bottom-up’ investment cases for BHP and MIN in particular.

Learn how the industry leaders are navigating today's market every morning at 6am. Access Livewire Markets Today.

All prices and analysis at 21 June 2024. This document was originally published in Livewire Markets on 21 June 2024. This information has been prepared by Wilsons Advisory and Stockbroking Limited (“Wilsons Advisory”)(ABN: 68 010 529 665)(AFSL: 238375) . The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.