9 ASX shares that might interest contrarians

Joseph Taylor | Morningstar

Finding an investment approach that fits your personality and situation can be hard. Until fairly recently, I spent most of my investing life trying to buy the cheapest shares possible and flip them when they appreciated.

I think this stemmed from my long-forgotten passion of betting on horse races. Instead of picking favourites, I would spend hours trying to find odds that I thought vastly underestimated the chances of an outsider. Taking a so-called contrarian approach and buying neglected shares was a natural fit. And in David Dreman’s Contrarian Investment Strategies, my 22 year old self found a guide on how to find them.

I recently stumbled across the book in Morningstar’s library and thought I’d re-read it. Seven years ago I did what most new investors do and blindly accepted everything. That wasn’t the case this time but I still think that a lot of his insights have value. I’ll share some of my favourites after giving you a quick overview of Dreman’s process.

As you can probably guess from the book title, Dreman’s strategy was to buy companies that were heavily out of favour. In practice, this meant buying stocks that traded cheapest on metrics like price-to-earnings, price to book, price to cash flow and dividend yield. He would then wait for the poor sentiment to ease. If a share rose back to the same valuation as the broader market, he would sell it and replace it with another cheap share.

Before we go any further, it’s important to note that this approach to investing might not fit your goals or personality. I no longer think it fits with mine. Aspects of it might also be outdated because measures like price-to-book value are less relevant for a lot of modern companies. Nevertheless, I enjoyed the book and think most investors can learn from it.

“Positive and negative surprises affect “best” and “worst” stocks in a diametrically opposite manner.”

Valuation levels are an expression of the market’s confidence in a company’s future earnings. Because of that, investment returns are heavily influenced by whether the company’s operating results exceed or fall below those expectations. If you invest in a company that is priced to perfection, even a small bump in the road can hit the shares hard. If a lot of bad news is already priced in, you might not even need good news to see good performance - just news that wasn’t as bad as the market was fearing.

“In a crisis, carefully analyse the reasons put forward to support lower stock prices – more often than not they will disappear under scrutiny.”

I think this insight is useful for ‘quality buy-and-hold’ investors too. Shares in high quality companies rarely trade at a material discount to their intrinsic value. When they do, it is usually because they are facing some kind of issue. Figuring out whether this a short-term headwind or a terminal problem can help you decide whether the shares offer an attractive buying opportunity relative to your goals.

An example here are situations where investors are concerned about a new source of competition. I love finding situations like this and finding out whether our analysts see it as a credible or non-credible threat.

For example, shares in ResMed (ASX:RMD) weakened considerably on fears that new rapid weight loss drugs might reduce the number of people needing sleep apnea treatment. At the Morningstar Investment Conference, Schroder’s Martin Conlon discussed how his team assessed the threat with the help of a medical expert and realised those concerns may have been overblown.

“Look beyond obvious similarities between a current investment situation and one that appears equivalent in the past. Consider other important factors that may result in a markedly different outcome.”

In many ways, the incredible share price performance of Philip Morris (NYS:PM) since 2000 has been a win for contrarians – the shares defied widespread expectations that a decline in the number of smokers would hurt profits and shareholder returns. And how.

I often see coal miners being referred to as ‘the next Philip Morris’. They are in a declining industry that may not decline as quickly as many people think. There are potential barriers to entry because getting permits and funding for a new coal mine in today’s climate would be tough. But what about the commodity nature of coal versus the brand loyalty of Marlboro smokers? What about nicotine addiction and the pricing power it brings? What about the completely different levels of capital intensity, profitability and cyclicality?

I’m not saying that coal miners can’t be a great contrarian investment. I’m just saying that the two situations are clearly different. Even if they have some similarities.

“Buy solid companies currently out of market favour, as measured by their low price to earnings, price to cash flow or price to book value ratios, or by high yields.”

As we saw earlier, buying a stock with sky-high expectations can be a recipe for disaster. Doing the opposite – and being very picky about which companies were “solid” – helped Warren Buffett become one of the richest men on Earth. His purchases of American Express (NYS:AXP) after the salad oil scandal and Coke (NYS:KO) during a period of bad management are classic examples. He bought very solid companies at a time when they were hated. But if he would have followed the next rule, those investments wouldn’t be so famous.

“Sell a stock when its P/E ratio approaches that of the overall market, regardless of how favourable prospects appear. Replace it with another contrarian stock.”

I understand why Dreman would take this approach to selling for this system. He is advocating a systematic and largely quantitative approach. He is not looking at stocks in great qualitative detail. Doing so, as he suggests in the book, could simply lead you to the same super pessimistic view on these stocks as the market. He is just trying to buy and flip the cheapest stocks again and again.

Personally, I have moved away from trying to flip stocks. Doing this for 20-30 stocks takes a lot of time that I’d rather focus on my career. I also find it hard to hold the kind of shares this strategy leads you towards. And if you can’t hold something long enough to see out your strategy, you shouldn’t buy it at all.

I talked about this in my article ‘How I set myself up for investing failure’.

Which ASX 200 shares might interest Dreman today?

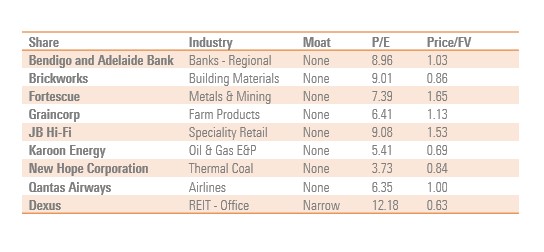

In a nutshell, Dreman recommends buying 20-30 large-cap stocks across several industries, targeting the cheapest share in each. He defines cheap by low P/E, low price to book, low price to cash flow or high dividend yield.

To find potential candidates in the ASX 200 and keep things simple, I chose P/E and looked for stocks with a P/E ratio below the market’s current ratio of 16. I also filtered for interest coverage ratios of over 3x for the non-banks.

From there, I picked the cheapest stock by P/E from a few different industries. Here is the sample I came up with, based on Morningstar data.

Of the nine sample stocks, only one has a moat according to our analysts. When you’re at this end of the price spectrum, that is perhaps to be expected. I was more surprised (at first, anyway) by how expensive the sample was relative to our estimates of fair value.

Three of the nine traded comfortably above our analyst’s estimate of fair value. Two were essentially in line and only two traded more than 20% below our fair value estimate. On average the group trades at a price to fair value of 1.04. According to our analysts, this isn’t an especially cheap group of stocks. You can see 11 ASX stocks our analysts do feel offer good value here.

The disparity can probably be explained by Morningstar’s investment philosophy and research methodology.

Most of the companies here don’t really fit with Morningstar’s vision of a highly valuable business – we prefer to see durable competitive advantages. Nor do we think that a P/E ratio or dividend yield alone can capture how cheap a share price is. Investing is about looking forward hence our analysts’ focus on forecasting future cash flows.

This puts Dreman’s stock selection approach at odds with ours. He thought that forecasting a company’s future results was impossible. Even so, I think some of Dreman’s rules make a lot of sense for investors following any investment approach – especially his warning to be careful about what expectations are baked in at the price you are paying.

The biggest lesson I took from this experience was the value of re-reading books. Not only will you find new insights you missed the first time. You’ll be able to read more critically and see how you’ve developed as an investor over time.

Joseph Taylor is an Associate Investment Specialist, Morningstar Australia.

Access this research and more at Morningstar. For a free four-week trial, click here.

All prices and analysis at 26 May 2024. This document was originally published on Morningstar.com on 26 May 2024 and has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892. The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.