Is CBA the most overpriced bank in the world?

James Gruber, Assistant Editor | Firstlinks and Morningstar.com.au

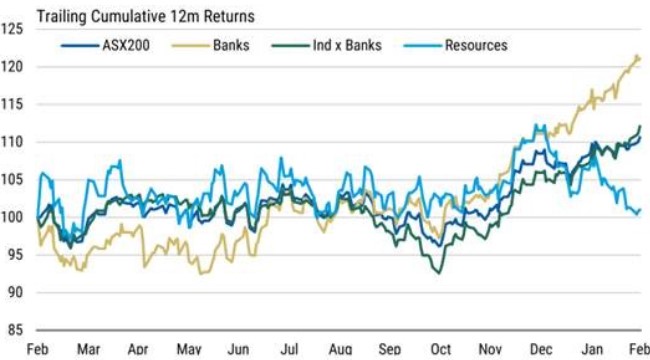

Australian banks have had a great run of late, compared to both the ASX 200 and other major sectors.

Source: Morgan Stanley, courtesy of Clime Asset Management

Commonwealth Bank (CBA) has stood out. It was largely flat for seven months into October last year, before exploding higher in recent months. Over the past 12 months, its share price has climbed 23% versus the ASX 200’s 8%.

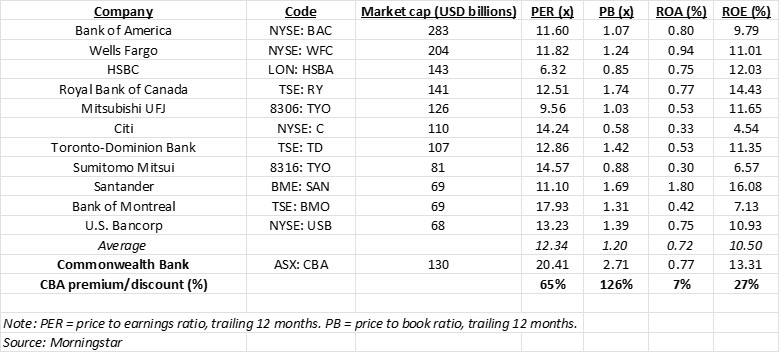

Source: Morningstar

What’s behind the move? It’s largely on expectations of an economic ‘soft landing’, rates cuts, and a resilient consumer. Throughout most of last year, investors were concerned about the fixed mortgage rate cliff, how rising rates would impact consumers and their spending, and whether the economy could hold up given these headwinds. Markets seem to be suggesting that those worries were overblown and that the economic picture is more positive for 2024.

Welcome to the most expensive major bank in the developed world

I thought it’d be a useful exercise to compare our largest bank, CBA, to other global retail banking peers to see how it stacks up on valuations and returns. Here’s a summary of the key numbers.

Major global retail bank valuations and returns

CBA is now the 12th largest bank in the world. In the table above, I’ve excluded investment banks such as JP Morgan and Morgan Stanley, which have large market capitalisations versus CBA. I’ve also excluded state-owned Chinese banks, which have low valuations from poor transparency and all of them dealing with property loans going bad due to the country’s deflating housing market. And I haven’t included some of the Indian banks as they still operate in a developing market where growth and returns are plentiful, and valuations reflect that.

The companies left on the list are those principally in developed markets - including Europe, Japan, Canada, and the US – and operating retail banking franchises.

What does the table tell us? CBA is arguably the most expensive retail bank in the developed world. The price-to-book (PB) ratio is the principal valuation metric used for banks, and CBA’s current PB ratio of 2.71x is at a 126% premium to the global peer average. No other developed market retail bank comes close to CBA on this metric, with the Royal Bank of Canada valued the next highest at 1.74x PB.

On a price-to-earnings ratio (PER) basis, the valuation gap is less extreme though still notable. CBA’s PER of 20.4x is at a 65% premium to global peers. Again, no other peer comes close to CBA, with the next highest being the Bank of Montreal at 17.93x PER.

Looking at valuation alone doesn’t tell the full story, though. We need to look at the returns of CBA to see whether the premium valuation accorded it is justified.

Return on equity (ROE) is the most common metric used to evaluate a bank’s returns. CBA’s ROE of 13.3% is 27% better than the global peer average. There are two banks with higher ROEs, namely Santander (16.1%) and Royal Bank of Canada (14.4%).

Return on assets is likely a better indicator as it measures how effective a company is at using their assets to create value, but minus the leverage which can boost ROE figures. On this score, CBA’s ROA of 0.77% is closer to the middle of the pack, at a mere 7% above the global peer average. Santander and Wells Fargo stand out on this metric.

All up, the table suggests that CBA’s returns are above the average of other major retail banks, but its valuation is way above comparable peers.

How does CBA stack up against other local banks?

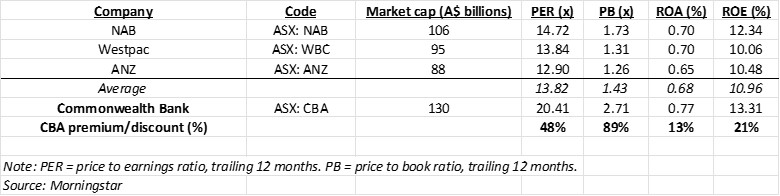

A global snapshot is useful, though a local one is necessary too. Here is the same table, though just for the major Australian retail banks (I’ve left out Macquarie Bank as it’s an investment bank).

Major Australian retail bank valuations and returns

Again, CBA’s premium valuations are striking. On a PB ratio basis, CBA’s PB of 2.71x is at an 89% premium to the average of the other three majors. And on a PER basis, CBA’s PER of 20.4x is 48% higher than the average 13.82x of the other banks. When it comes to valuations, no other Australian bank comes close to CBA.

As for returns, CBA’s ROE and ROA are 21% and 13% respectively superior to the average of the remaining three banks.

While the disparity between valuations and returns for CBA against Australian peers is less stark than against international banks, it’s still significant.

Is CBA’s premium valuation justified?

While numbers such as these are helpful, it’s good to delve deeper into the reasons why CBA may or may not deserve a better valuation than other retail banks.

Let’s look at the strengths of the bank:

1. It operates in a bank oligopoly. The structure of the banking industry in Australia is the biggest strength for all the major banks, including CBA. The ‘four pillars’ policy prevents any of the four major banks from taking over each other, which eliminates the prospect of competitors merging to gain scale and competitive advantages. It effectively backstops the domination of the big four banks and limits competition, which improves returns on equity.

The banking market most like Australia is probably Canada. The large retail banks there have also enjoyed decades of high returns on capital and rewarding share performance.

Contrast this with the US, which has more than 4,000 commercial banks (versus 62 locally owned ones in Australia). Bank competition is much stiffer in America, and the retail bank returns are generally lower.

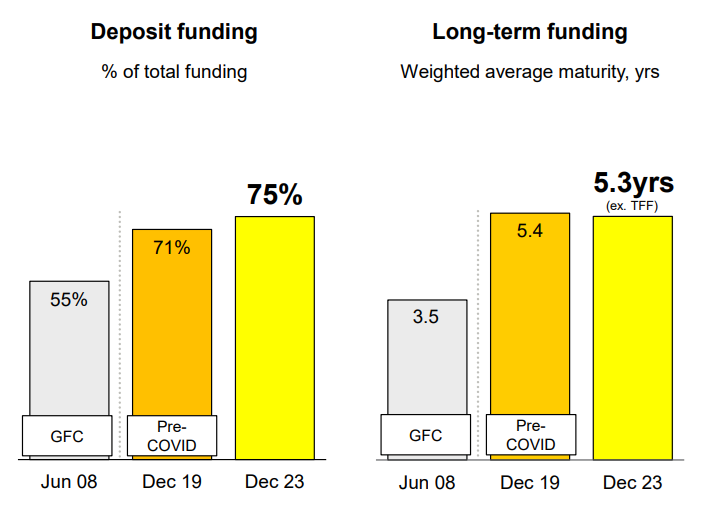

2. CBA is the deposit king. CBA has 16 million banking customers and 10.9 million transaction accounts, giving it the largest deposit funding pool of any Australian bank. It allows CBA to have access to cheap and sticky funding for its business. Close to 75% of total funding comes from deposits, with the rest from securitization, hybrids, and wholesale funding.

Source: CBA

3. Home loan stranglehold. Most of CBA’s loans are home loans, which are considered the safest of loan types (more on that later). And it has a 25% share of the home loan market, well ahead of the second largest lender to this segment, Westpac.

4. Sound credit quality. The quality of loans is sound at this stage. Just 0.52% of home loans are in arrears, and CBA seems well provisioned for potential bad debts in future.

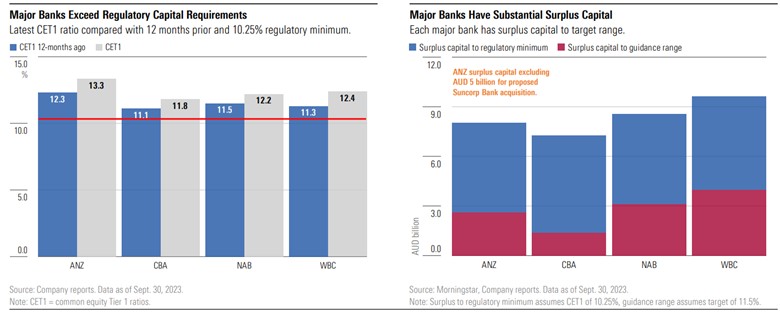

5. Sound capital position. CBA is well capitalized with a common equity tier 1, level 2, ratio of 11.8%, well above the regulatory minimum of 10.25%. APRA’s push for greater capital to be held by banks post-GFC leaves all of them, including CBA, in a strong position.

6. Technology lead? Fund managers and analysts often talk of CBA’s lead in technology over competitors, though my direct experience with the bank has me scratching my head on this one. It may be true, though I haven’t really seen it from my end.

CBA’s weaknesses

1. Unexciting growth prospects. Thanks to a spectacular housing boom, loan growth for the banks has been buoyant for much of the past four decades. It’s slowing now and is highly unlikely to get back to anything like the growth of the recent past. CBA housing loan growth was just 0.1% in the most recent quarter.

2. Loan competition. Recently, Macquarie Bank has ramped up competition in the home loan market. CBA has chosen to not match some of the aggressive pricing of Macquarie Bank and others. While it’s not intense competition as some make out it to be (intense for Australia, perhaps), it is a near-term headwind for CBA.

3. Deposit competition. With rising rates, competition for deposits has heated up. Yet, this issue shouldn’t be overstated, as deposits are traditionally sticky, as CBA has a stickier franchise than other any bank.

4. Exposure to stretched housing market. CBA is all in on housing, and it remains its biggest current strength, but also its largest risk. I’ve previously argued that housing in Australia is likely priced more expensively than any other asset in any part of the world – even more expensive than the Magnificent Seven tech stocks. Any downturn in housing would increase bad debts, profits, and balance sheet strength.

5. Commoditised products. This isn’t a CBA issue as it’s common to all retail banks. That is, banks offer commoditized products with little in the way of differentiation. Commoditisation means banks have minimal pricing power, which ultimately results in lower returns on equity.

Risk versus reward

Assessing whether to invest in a stock, or to stay invested in a stock, is about weighing up the potential reward against the potential risks. Given the tepid short- and long-term earnings outlook, the current pricing of CBA seems exorbitant both against local and global peers.

First published on the Firstlinks Newsletter. A free subscription for nabtrade clients is available here.

All prices and analysis at 21 March 2024. This information has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892 .

The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.