Is bad press a buying opportunity for Woolworths and Coles?

The value gap between Australia’s two largest supermarket operators has been dramatically closing over the space of a week, following their first-half fiscal 2024 results.

However, both defensive plays screen as overvalued. We think the market underestimates the risk of relatively low-growth, defensive yield stocks like Coles and Woolworths derating, given higher prevailing interest rates.

Source: Morningstar

Woolworths’ supermarket sales growth decelerated meaningfully to the low single digits in the initial weeks of the second half versus the previous corresponding period, or PCP, and its CEO Brad Banducci announced his impending retirement. However, Coles’ supermarkets are maintaining sales growth in the midsingle digits at the start of the second half.

We are reluctant to extrapolate the differential in sales growth of the two largest Australian supermarket chains over a relatively short time period—less than two months' trading. There are temporary factors for divergence in near-term sales momentum, including the timing of promotions and Coles’ Pokemon collectibles marketing campaign, which started Feb 7, 2024.

Further, we expect any prolonged underperformance in trading to trigger a competitive response from Woolworths, with more discounting potentially hurting the bottom lines of both players. From fiscal 2025, we expect Coles and Woolworths to maintain their respective market shares and increase their Australian grocery sales in line with industry growth of 4% per year.

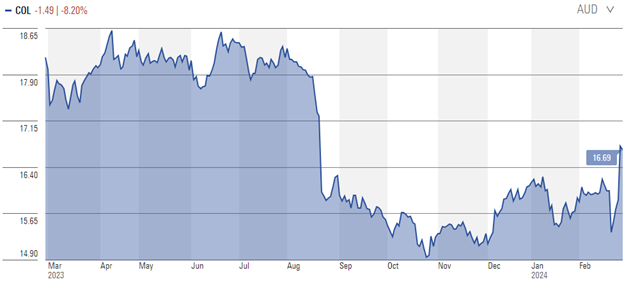

Coles’ first-half sales and earnings are tracking our fiscal 2024 estimates, and our forecast is virtually unchanged. We lift our fair value estimate for no-moat Coles by 3% to AUD 15 per share solely due to the time value of money.

Coles (ASX: COL)

Coles Group's businesses are defensive in nature, with its cash flow largely from consumer staples which are relatively stable across the economic cycle.

Coles also profits from negative working capital, allowing it to release capital as the business scales. The quality of these cash flows is high and with cash generation averaging over 100% in the five years to June 2028, we expect the dividend payout ratio to average over 80%. The shares are currently yielding 3.94%.

Coles' investment appeal as a defensive income stock is further underpinned by its strong balance sheet, manifested in investment-grade credit ratings from both Standard & Poor's and Moody's. Operating leases have an average lease expiry of around six years, providing the group with the flexibility to optimize its store network.

Coles operates the second-largest supermarket chain in Australia. The group gradually expanded its market share under Wesfarmers ownership, peaking in fiscal 2016. Since then, we estimate Coles lost some 2.3% in market share, chiefly to Woolworths.

However, over the past three years, the combined market share of the full-service supermarkets, Coles and Woolworths, has been steady at 65%. At the same time, Aldi gained .60% in market share, while the independent supermarkets and grocers were the losers and the IGA network's market share shrank by some .50%.

Coles supermarkets currently capture 28% of Australian food and grocery retailing, compared with market leader Woolworths at 36%, the IGA network at 12%, and Aldi at 9%. Costco operates membership-only warehouses and has a market share of under 2%. The U.S. giant commenced trading in Australia in 2009 and currently operates 14 warehouses.

E-commerce penetration of Australian food retailing remains low, at around 3%, with Coles and Woolworths as the dominant online players. We expect in-store sales to continue to dominate total industry sales for at least another decade, accounting for over 90% of revenue. However, we estimate incremental sales growth is increasingly sourced from online. Therefore, we anticipate optimizing e-commerce economics and convenience to be key focus areas of supermarkets.

Woolworths (ASX: WOW)

Woolworths is one of Australia's largest retailing groups, operating supermarkets and discount department stores. Its market capitalization is around $45 billion, with annual sales of over $60 billion.

Woolworths has a narrow economic moat characterized by an extensive supermarket store network, serviced by an efficient supply chain operation coupled with significant buying power. It operates in the very competitive supermarket and discount department store segments of the retail sector.

Intense competition has taken its toll on margins. Management has reset prices lower to drive foot traffic and increase basket sizes. Volume growth is vital for maximizing supply chain efficiencies.

To contextualize Woolworths' enormous scale advantage, its Australian food sales of over $40 billion represented about 15% of total Australian retail sales in fiscal 2022. The percentage increases substantially if sales are strictly comparable. For example, Woolworths has negligible exposure to cafes, restaurants, and takeaways, where sales totaled some $60 billion. We estimate that a more representative percentage on a strictly comparable basis would fall closer to 20%.

Key risks involve increased competition in the Australian retail landscape and reduced consumer spending. The change in ownership of Australia's largest retailer, Coles, in 2007, was the catalyst for increased price competition by both groups to win market share, while the entry of Amazon Australia could raise the competitive bar in the future.

The aggressive expansion of low-cost discounter Aldi has altered and further segmented the grocery sector and increased competitive pressure. A reduction in the rate of growth in consumer spending would affect revenue growth and could affect operating margins. Increased frugality and heightened deflationary pressures would crimp top-line sales growth, and relatively high fixed-cost leverage would affect margin.

However, Woolworths is well positioned to withstand cyclically weak consumer spending. Woolworths is a defensive stock, with food retailing generating most of group revenue and profit, a solid balance sheet, and a narrow moat surrounding its economic profits.

Johannes Faul CFA, is a director of equity research, Morningstar ANZ.

First published on the Firstlinks Newsletter. A free subscription for nabtrade clients is available here.

All prices and analysis at 28 February 2024. This information has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892.

The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.