Is uranium going to boom and bust?

There is no doubt that commodities move in cycles. These are well-established. We see it all the time and none more dramatic and violent than the lithium price. From Hero to Zero in a year. Truly astonishing. But there is a reason for this. It is a new material. Long-term price trends, supply, and demand have not settled down as yet. Not only that, but we have also gone from relatively unsophisticated investors like car companies frantically trying to tie down supply and ensure continuity and certainty, to new battery technology and chemistry affecting the near-term sentiment and possibly even the long-term viability of this nascent material. Did someone say Sodium Ion batteries?

With uranium, things are different. Uranium has been around for decades. The average age of the US Nuclear power plant is 42 years. Even Homer Simpson works in one!

The price of the underlying commodity is relatively slow-moving. Contracts are long term and there is a huge amount of politics (and emotion) wrapped around nuclear power, fuel and enrichment. And more importantly, there is no substitute. No cheaper version of it to take its place. No sodium or even recycling.

Where lithium is a capricious teenager, uranium is a dowdy middle-aged metal. Lack of investment due to sustained low prices has led to a market dominated by a few large players. Few new mines have come on stream. More importantly, the dominant suppliers are from places that are a little inconvenient. Russia (decommissioned nuclear warheads for many years), Kazakhstan with the world biggest in Kazatomprom, here in Australia, BHP is the fourth biggest producer at Olympic Dam.

Recent political events have thrown uranium into focus. COP28 had an unprecedented 22 countries sign on the dotted line to expand their use of nuclear power to triple the size by 2050. Preferably like Germany, with its power policy, outsourcing the actual location of the nuclear power plants. France has been convenient, in this respect and gets 70% of its power nuclear. Sells a lot to Germany which closed its nuclear industry.

Currently there is a hope that Small Modular Reactors (SMRs) become the solution to baseload power combined with renewables. An inconvenient issue is that the poster child for this, Nuscale, had to abandon its proposed power plant in the US, because it was just going to be too expensive. SMR remains a new untested technology in the West.

China, though, is building new capability. Over the past decade, China has added 37 nuclear reactors, for a total of 55, according to the International Atomic Energy Agency, a UN body. During that same period America, which leads the world with 93 reactors, added two. Most of the new reactors are being built in Asia or India.

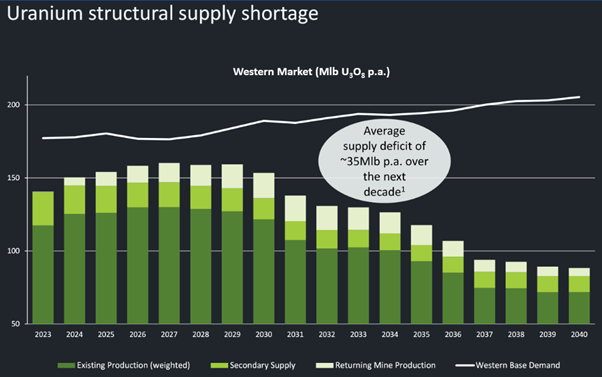

Supply is a huge issue. The US has a dependence on Russia for its enriched uranium and very small production capacity. For obvious reasons, the US would really like to get away from Russian dependency. It has plans but these things take time. It is especially dependent on Russia for enriched product. One potential winner here could be Silex (SLX) with its 3rd Generation Enrichment technology which has been in development for 30 years. Things do move slowly!

Here in Australia, we have a number of listed uranium wannabes, most are restarting previously shuttered mines like Paladin (PDN) or searching for treasure in Namibia and other African nations. BHP hardly mentions uranium in its press releases. More focus on potash. Politics with nuclear power is everywhere. That is part of the reason it is a slow-moving commodity. Secrets, long-term contracts, and the ability of nuclear fuel to be dual-purpose are sub-optimal. Making bombs is slightly frowned upon.

Uranium is not the new lithium. From my chemistry days, I remember lithium has a propensity to burst into flames and be very tricky to extinguish. In my school days, it was a dramatic lesson. Always good fun to see stuff go up in flames. Plenty of E-Bikes seem to be recreating those experiments too. The reaction of lithium seems a good metaphor for the underlying price. Uranium has no such problems and has to be enriched with centrifugal technology to become useful.

There are a number of ways to play uranium on the ASX. The highest profile and the go-to stock wise is Paladin (PDN). But Boss Energy (BOE), with its soon-to-be-producing Honeymoon project, is equally as attractive. Plus, it has a good geographical spread. Its recent acquisition of Alta Mesa in Texas has helped and gives it a foothold in the US. Pretty important with Biden’s IRA plans.

There have been some rumblings on Namibia trying to get a bigger slice of the resource pie. A slight risk for some.

Other stocks to consider would be a Canadian goliath in Nexgen Energy (NXG)

Deep Yellow (DYL) is another Namibian hopeful having a resurgence.

For the more conservative investors who are after exposure to the metal, together with the biggest producers, there is a good ETF URNM.

Holdings in the ETF

Source: Betashares

In the last few weeks production warnings have come out of Kazatomprom, due to a shortage of sulfuric acid, which is used to leach the uranium from the rock. It is called In Situ Leaching. ISL. Warnings too from Cameco on issues in Africa

In short, demand is strong on climate change aspirations, a political will to remove some of the country risks in supply, and production is suffering both in Canada and Kazakhstan, and new production is taking its time.

Source: American Nuclear Society

PDN’s Langer Heinrich project in Namibia seems to have been years in the planning and is only just on the cusp of production again. And in the big scheme of things, it will not touch the sides in terms of satisfying that demand.

The whole sector has run pretty hard in the last few months as the fast money has switched from playing lithium hopefuls to uranium explorers. It needs to consolidate, but it could be the pause that refreshes. We seem to have had some panic buying after the spot move above US$100 which is easing so investors can be slightly more discerning in their picks of the sector. A little bit of patience could see better prices achieved.

It seems after years in the wilderness, uranium is finally starting to seize the day. One local broker has a US$150 target for the spot price next year. So far, in the last year, uranium is up 116%. No lithium, but then do you really want that wild ride in this strategically sensitive metal? No boom and bust here. A long slow grind higher on fundamentals. Cyclical yes, but the cycle is only just starting to turn. Lithium has fallen 90% in a year. Uranium is up over 100% in a year. I know where I would be looking for gains. Lithium has yet to show signs of turning.

A free trial of the Marcus Today newsletter for nabtrade clients is available here.

All prices and analysis at 27 January 2024. This information has been prepared by Marcus Today Pty Limited. Marcus Today Pty Ltd ABN 57 110 971 689 is a Corporate Authorised Representative (no. 310093) of AdviceNet Pty Ltd ABN 35 122 720 512 (AFSL 308200).

The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.