The time for bonds has come

John Barrasso and Adrian Janschek | First Sentier Investors

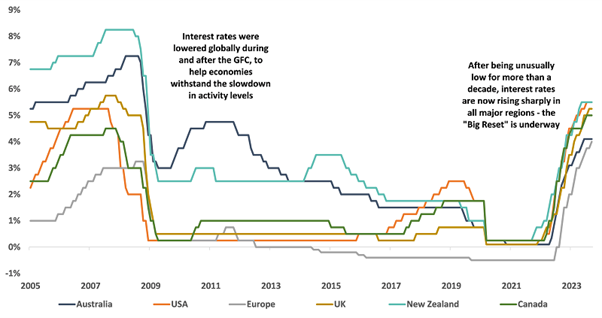

Markets worldwide spent much of 2008-2021 adjusting to unprecedented central bank support. This period began with policymakers’ response to the Global Financial Crisis (GFC) and finished at the end of the COVID pandemic. Much of this period saw cash rates in key regions at, or below, zero. Central bank balance sheets became bloated mostly with government bonds as authorities bought assets to support financial markets.

Figure 1: Developed market overnight rates

Source: Bloomberg. Data shown 1 January 2005 to 30 September 2023

In 2021, two major changes marked an inflection point for the 'Big Reset' to begin.

1 – Inflation exploded globally

- COVID lockdowns significantly disrupted manufacturing and supply chains across the globe, increasing both product prices and delivery costs. Commodity prices also began to skyrocket as the conflict in Ukraine unfolded.

- The scale of the global pandemic support delivered by governments and central banks was unprecedented and, in hindsight, arguably excessive. Consumers looked to deploy excess savings once the pandemic eased, resulting in an increase in global demand.

- These factors have seen inflation soar and the Consumer Price Index is now meaningfully above central bank targets in all key regions. Policymakers have responded by raising cash rates, hoping to dampen discretionary spending and bring inflation under control.

2 – The 'elephants' left the room

- With the global economy in full recovery and cash rates moving higher, central banks began to unwind their balance sheets, selling securities they had acquired in the preceding years. Central banks, previously the largest buyers of government bonds, became sellers.

- Government finances around the world were required to fund huge deficits from higher spending during the COVID pandemic. Markets have been flooded with higher bond issuance as governments look to repair their financial positions.

Historically, transitions away from aggressive central bank policies created volatility in financial markets, owing to uncertainty around the pivot from one interest rate regime to another. We believe that a soft landing is the most likely outcome over the next six to nine months whereby policymakers are able to engineer a slowdown in economic growth and inflation, without tipping economies into recession, and further changes in central bank policy will be gradual following a recent pause in the tightening cycle.

Where to from here? We share our thoughts on inflation, the pending actions of central banks regarding cash rates and, in turn, the possible implications for long-term bond yields.

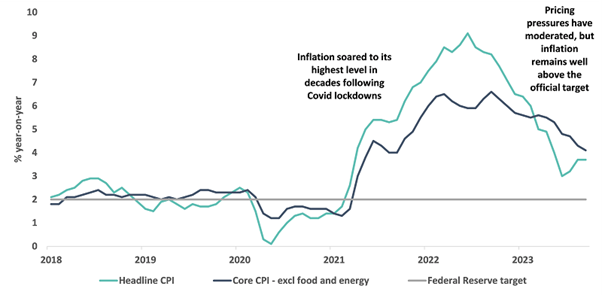

Inflation

With some of the large increases in prices in late 2022 and early 2023 rolling off the calculations, referred to as the ‘base effect’, we believe annual inflation will continue to moderate well into 2024. The most recent data, including 3-month and 6-month annualised run rates, are converging back towards central bank target rates. In some cases, most notably in the United States (US), readings such as the Multivariate Core Trend[1] and the Underlying Inflation Gauge[2] have nearly recovered to pre-COVID levels.

We are mindful of stickier elements of inflation, which might be harder to dislodge from the official data. These include rent or shelter costs and the prices of other services that have lagged the rise in goods prices globally, and which may remain elevated due to surprisingly robust economic growth rates, low unemployment levels, and strong wage growth. Central banks are not forecasting a return to target inflation rates until 2025 or 2026, suggesting they could continue to warn about the possibility of further interest rate hikes, and guide investors away from the possibility of premature policy easing.

Figure 2: US inflation

Source: Bloomberg. Data shown 1 January 2018 to 30 September 2023

Cash rates

Following the sharp rises over the past 18-24 months, overnight cash rates in many parts of the world are at or near their cycle highs, in our view. Most major central banks now regard the risks to economies as more balanced, and given our inflation view, we believe policymakers’ ‘higher for longer’ stance will be maintained. Some countries might be required to raise cash rates by another 0.25-0.50% in the next 12 months if delays in inflation returning to target exhaust central banks’ patience. At the very least, we feel policymakers will likely seek to guide markets forcefully away from expecting rate cuts until inflation is much closer to target levels or growth begins to falter.

Although this is our base case, our inflation and interest rate views are fluid. We are mindful of a potential re-acceleration of the global economy by mid-2024 driven by US economic strength, which in turn could require another round of rate hikes to counter this.

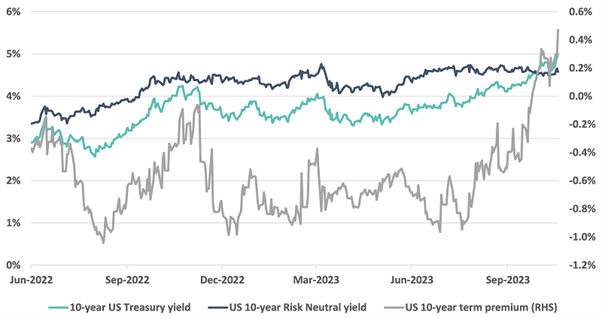

Long-term bond yields

Yields on longer-dated fixed income securities consist of two elements: expectations regarding the future path of cash rates and the term premium. Term premium, defined as the compensation that investors demand for interest rate risk in bonds, plays a critical role in understanding yield movements. The impacts from central banks unwinding their balance sheets, increased government bond issuance, geopolitical events and uncertainty around future inflation all suggest we could see further upward pressure on long-term yields i.e. the term premium and yield curve moving higher. The grey line in Figure 3 shows how much of an effect the recent increase in term premium has had on bond yields, over and above the market’s expectations of higher interest rates.

Figure 3: US 10-year term premium

Source: Bloomberg. Data shown 1 June 2022 to 19 October 2023

What signs are we looking for to suggest the “Big Reset” could be complete?

- First, we expect the Bank of Japan to strongly support and defend its recently announced 1.00% target for 10-year Japanese Government Bond (JGB) yields. The Bank of Japan changed its Yield Curve Control policy in July, doubling the cap on 10-year yields from 0.50% to 1.00%. This is a strong and underappreciated driver of global rates, given the Japanese yen has long been regarded as a funding currency, and since JGBs have anchored global rates. Japanese bonds have not participated in the global sell-off to the same extent as other sovereign bond markets due to stable Japanese monetary policy, which has seen official cash rates remain unchanged in Japan for more than seven years. While this yield adjustment is ongoing, we believe upward pressure on global yields could persist.

- Base effects continuing to slow inflation to a pace that may be slightly higher than central bank forecasts, but without any big upside (greater than +0.50% from target) surprises.

- Asset selection starts to favour US Treasury yields over equity earnings yields by greater than 0.50%. Currently, 2-year US Treasury yields are close to 5.20%[3], compared to an earnings yield of around 4.75%[4] on the S&P 500 Index.

- With the Effective Federal Funds rate[5] currently above 5.30%, we are looking for yields on 10-year Treasuries to approach that level and largely remove the negative carry still embedded in yields before we consider the market to have reached a more stable equilibrium.

- The risk/reward balance favours our forecast for a further increase in term premium and the possibility of further increases in cash rates.

If bond markets travel as expected and the “Big Reset” is close to completion, fixed income should appeal to investors. Specifically, an allocation to bonds currently offers a good opportunity to access attractive, credit risk-free income streams.

For local investors, for example, a 0.50% increase in the 10-year Australian Commonwealth Government Bond yield from today’s 4.73% would still generate a total return of 0.9% over a one-year holding period. Conversely, the yield falling 0.50% would result in an 8.6% return.

The skew is now much more in favour of investors than it was during the extended period of near-zero interest rates following the GFC, because higher rates mean higher income streams, cushioning any potential capital depreciation of bonds. In order to have a negative return over a one-year holding period, 10-year Australian Commonwealth Government Bond yields would need to rise 0.60%, on top of the 3.70% they have already risen over the past two years or so as the Reserve Bank of Australia has increased the official cash rate from 0.10% to the current 4.10%. Regardless of the future interest rate path and the potential for some variability in returns along the way, long-term investors will capture an annualised, risk-free return of nearly 5% over ten years if purchased bonds are held to maturity.

As a reminder, fixed income offers two main attributes to investors:

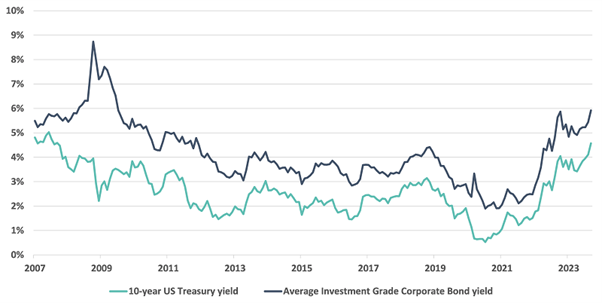

- Income – Low-risk 10-year government bonds in the US, Australia and New Zealand are typically offering yields between 4.50% and 5.50%. Highly rated corporate bonds are providing even more appealing income streams, typically between 5.75% and 6.50%. These are the most enticing levels for more than a decade. First Sentier Investors’ flagship Australian Fixed Income Fund, which consists primarily of State and Government bonds, is currently yielding around 5.20%[6].

Figure 4: Prospective yields from US Treasuries and Investment Grade Corporate Bonds

Source: Bloomberg. Data shown 1 January 2007 to 30 September 2023.

Investment Grade Corporate Bonds are represented by the Bloomberg Global Aggregate Corporate Index.

- Diversifier to equities – Post the cyclical “Big Reset” that appears to be nearly complete, we believe the correlation between fixed income and equities will reassert itself. We saw this during the banking crisis of March 2023, when bond prices increased (as yields fell by around 0.50%) and the S&P 500 Index fell around 5% during that two-week period. An allocation to fixed income should therefore provide useful diversification from risk assets, helping investors generate smoother, more stable overall returns from their investment portfolios over time.

With these considerations in mind, we consider the current risk/reward trade-off for holding bonds to be particularly favourable and could present investors with a good opportunity to increase exposure to fixed income assets.

[1] A model that measures inflation’s persistence across the core sectors of personal consumption expenditures price index (PCE).

[2] This captures sustained movements in inflation from information contained in a broad set of price, real activity, and financial data.

[3] Source: Bloomberg. Data as at 19 October 2023.

[4] Source: Bloomberg. Data as at 19 October 2023.

[5] A daily effective interest rate, calculated using the volume-weighted mean of overnight rates on trades arranged by major brokers. Data as at 19 October 2023.

[6] Source: First Sentier Investors. Data as at 19 October 2023.

John Barrasso and Adrian Janschek are Portfolio Managers in the Australian Fixed Income team at First Sentier Investors, a sponsor of Firstlinks. All prices and analysis at 22 November 2023. This document was originally published in Firstlinks, a publication from Morningstar Australasia (ABN: 95 090 665 544, AFSL 240892), on 22 November 2023. This information has been prepared by Acorn Capital Pty Ltd (ABN 89 114 194 311, AFSL 289017). The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.