Three reporting season stars to consider for your portfolio

As the dust settles on the FY22 reporting season, investors are sifting through the good, the bad and the ugly. Here are three results that I think were eye-catchers for the right reasons.

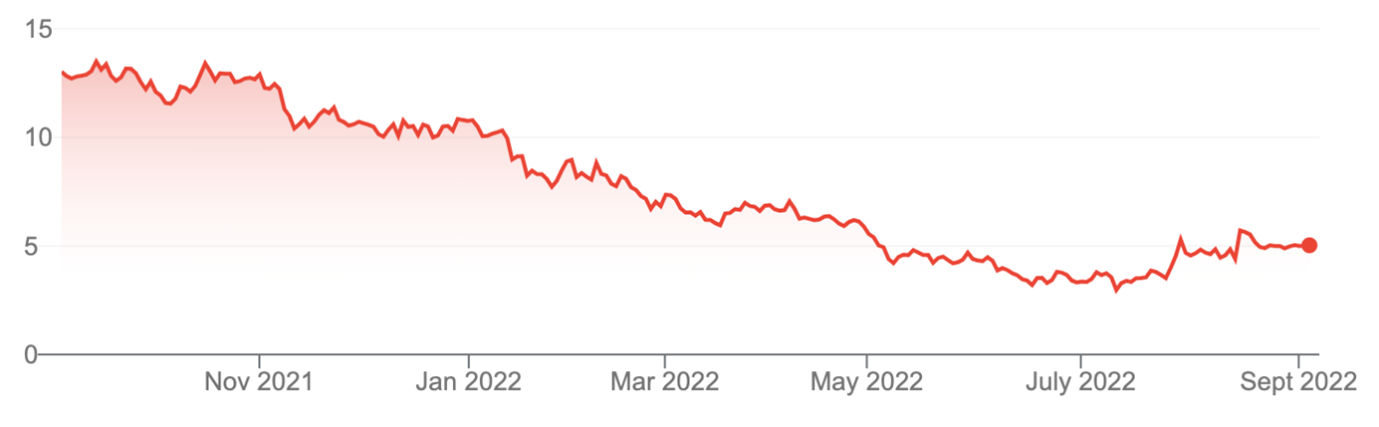

Temple & Webster (TPW, $5.02)

Market capitalisation: $607 million

12-month total return: –62.6%

Three-year total return: 47.8% a year

Estimated FY23 dividend yield: no dividend expected

Analysts’ consensus target price: $5.80 (Stock Doctor/Thomson Reuters, 11 analysts)

Online furniture and homewares retailer Temple & Webster (TPW) has struggled over the past year, as heady growth stock valuations have been wound back, supply-chain worries have concerned investors generally, and market perception of a rebound in physical retail has grown. But the full-year FY22 result impressed, as revenue surged 31%, to $426.3 million, and the EBITDA (earnings before interest, tax, depreciation and amortisation) margin came in at 3.8%, at the high end of the guidance range of 2-4%.

EBITDA and net profit were down on last year, but the market looked past those numbers to see some attractive things happening at TPW.

Active customer numbers rose by 21% to 940,000, while revenue per active customer increased 6%, the eighth consecutive quarter of growth. 55% of orders now come from repeat customers, outweighing first-time customers; repeat orders cost significantly less to acquire. The company said that month-to-month trading suggests a “return to double-digit growth during FY23” once it is no longer comparing figures against lockdown-affected periods.

In May, TPW launched ‘The Build’, an online site specifically for renovation projects, intending to become a major player in the $26 billion home improvement market, leveraging off the same model as the broader business: 27% of Temple & Webster’s 240,000-plus products come from its private label, sourced directly from more than 100 factories, while 73% of the range comes from “drop shipping,” in which TPW does not hold the inventory, but accepts orders and sources instantly from thousands of factories around the world. Temple & Webster says the furniture and homewares market is “large, stable and continues to shift online,” while the DIY renovation and home improvements market offers a new pathway of growth. All up, despite the profit fall, the FY22 result looked very good in terms of setting the company up for growth.

Temple & Webster Group Limited (TPW)

Source: ASX

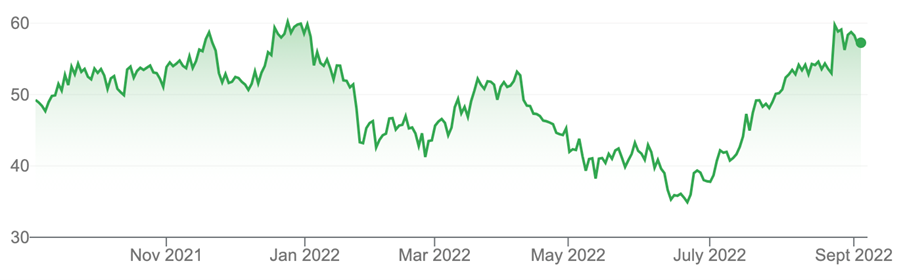

WiseTech (WTC, $57.06)

Market capitalisation: $18.6 billion

12-month total return: 16.8%

Three-year total return: 15.9% a year

Estimated FY23 dividend yield: 0.25%, fully franked (grossed-up, 0.4 per cent)

Analysts’ consensus target price: $59.00 (Stock Doctor/Thomson Reuters, 12 analysts)

Cloud-based logistics software company WiseTech Global (WTC) had a great result, with revenue up 25% to $632.2 million, statutory net profit up 80% to $194.6 million – at the higher end of the company’s guidance range – and underlying net profit up 72%, to $181.8 million. Free cash flow surged 71%, to $237.3 million, and the final dividend was increased by two-thirds. Revenue from the flagship CargoWise platform grew 37%, at the top end of the 30-40% guidance range. The gross profit margin increased by two percentage points, to 87%.

CargoWise has now grown its revenue by five times over the last six years, with recurring revenue growing at a compound annual rate of 31%. It has effectively become the global standard in freight-forwarding software. WiseTech has cut its sales and marketing costs from 13% of revenue in 2020 to 7% in 2022.

FY23 revenue guidance is for growth of 20-23%, to a range of $755–$780 million, powered by a 30-35% lift in CargoWise revenue. On an EBITDA basis, WiseTech has told the market to expect growth in the range of 21-30% in FY23, to a range of $385–$415 million.

This is based on a backdrop of slight improvement – slight, but still improvement – in world trade movement, despite geopolitical and inflationary pressures. WiseTech expects merchandise trade volume growth of 3% in 2022, down from the previous World Trade Organisation (WTO) forecast of 4.7%, and rising to 3.4% in 2023. The company says demand for goods continues to outpace pre-COVID-19 levels: it is running at 4.9% above the pre-COVID trendline. Although the global logistics industry remains under huge pressure, it appears that this is only making CargoWise more valuable to customers as a solution; almost 90% of revenue is coming from existing customers.

Braver investors have picked up a 64% rise in WTC from its June lows, and their buying was validated by the result. There is still a bit of value left, according to analysts.

WiseTech Global Limited (WTC)

Source: ASX

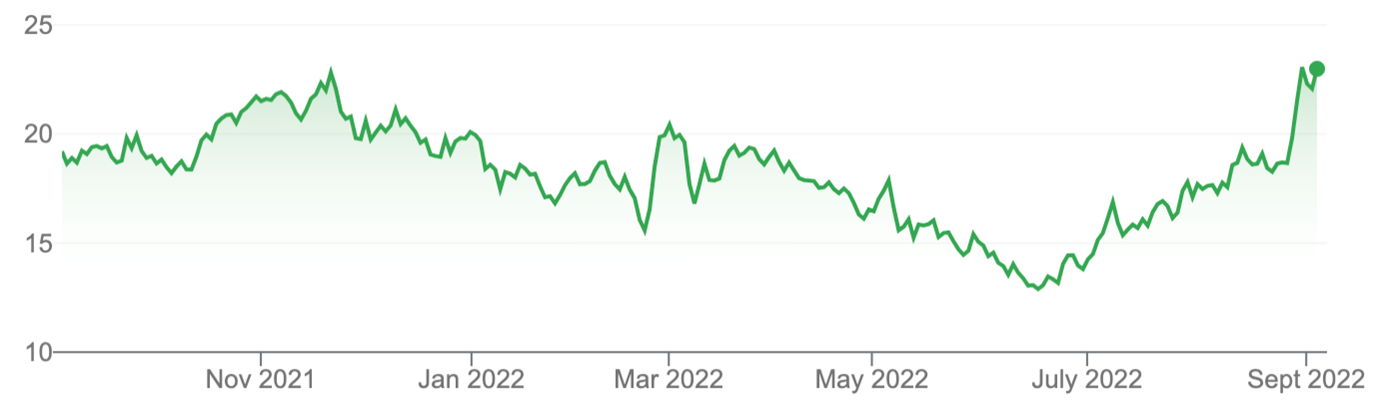

Lovisa (LOV, $22.08)

Market capitalisation: $2.4 billion

12-month total return: 16.9%

Three-year total return: 24.7% a year

Estimated FY23 dividend yield: 2.6%, 30% franked (grossed-up, 2.9 per cent)

Analysts’ consensus target price: $21.40 (Stock Doctor/Thomson Reuters, 12 analysts)

Fast-fashion jewellery store chain Lovisa (LOV) brought out an outstanding result, showing that despite the challenges the company has faced from COVID over the past two years, it is well on the way to achieving its goal of becoming a global brand. The global rollout strategy saw 85 new stores opened for the year, to a total of 629, led by 55 new stores in the US (up to 118) and 169 stores trading in Europe. The company entered two new markets during the year, in Poland and Canada, to make a total of 24 markets.

Revenue surged 59%, to $458.7 million, and net profit more than doubled, to $59.9 million. Online sales grew by 30%. The gross margin improved from 76.7% to 78.9%, and operating cash flow lifted 48% to almost $150 million. The FY22 total dividend almost doubled, to 74 cents a share, from 38 cents last year. The company ended the year with $24.2 million in net cash and no debt.

Lovisa has hit the ground running in the new financial year, with total sales in the first seven weeks of FY23 surging 66%: the company has opened 22 new stores so far (including its first two stores in Hong Kong and its first store in Namibia), and on a comparable-store basis, sales for the first seven weeks are up 21%. It’s a great story – but there is considerable disagreement among analysts as to where LV goes from here. After the result, Macquarie nominates a price target of $27.70 – but Morgan Stanley expects to see LOV at $18.00. Macquarie sees Lovisa as being well-positioned in the current environment, being exposed to low-price-point costume jewellery and younger buyers, a combination that should continue to perform well. I’m inclined to back that view of LOV over the pessimists.

Lovisa Holdings Limited (LOV)

Source: ASX

All prices and analysis at 5 September 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.