Four reporting season shockers

Although the August reporting season was considered a mostly positive one, there were (as always) stocks that disappointed the market.

Here are four of the most notable disappointments – with two stocks where that situation can work in your favour.

Appen (APX, $3.82)

Market capitalisation: $472 million

12-month total return: –61.6%

3-year total return: –46.9% a year

Expected FY22 (December) dividend yield: 0.4%, 50% franked (grossed-up, 0.5%)

Analysts’ consensus price target: $4.16 (Stock Doctor, Thomson Reuters, 11 analysts), $3.57 (FNArena, three analysts)

Appen (APX) is an Australian global technology leader: its speciality is the development of high-quality, human-annotated datasets for machine learning and artificial intelligence (AI). Appen creates the data that goes into the machine learning models of many of the biggest tech companies in the world.

As a calendar-year balance-date company, Appen brought out half-year results in the reporting season just completed, and the market was not impressed. Appen ditched its dividend after tumbling to a half-year loss – it posted a net loss of US$9.4 million, down from an interim profit of US$6.7 million a year ago – and warned the market that its annual revenue would likely be below levels of previous years.

Revenue was down 7%, at US$182.9 million, and more importantly, that figure was well below analysts’ consensus estimates. Appen blamed a downturn in the digital advertising market, which resulted in a slowdown in spending by some of its customers on large global programs. Growth in the order book has slowed, and that worries some analysts. There are even “sell” ratings on the stock – Ord Minnett and Citi have made that call.

Appen said that FY22 revenue was “not expected to be at prior-year levels due to slowdown of global customers,” and that it expected FY22 EBITDA (earnings before interest, tax, depreciation and amortisation) and the FY22 EBITDA margin to be “materially lower than FY21 mainly due to lower revenues, as well as investment in product, technology and transformation”. Appen also said trading hadn’t improved in July and August – the company is a fallen tech star, and the turnaround doesn’t look to be in sight yet, as the market waits warily for full-year results. Longer-term, the company’s expertise in AI and machine learning will be a big positive for owners of APX, but I don’t think you could confidently buy the stock yet.

Appen Limited (APX)

Source: nabtrade

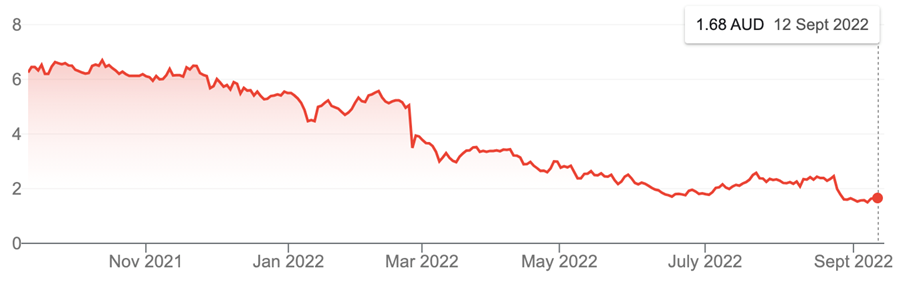

City Chic Collective (CCX, $1.655)

Market capitalisation: $396 million

12-month total return: –73.6%

3-year total return: –8.8% a year

Expected FY23 dividend yield: no dividend expected

Analysts’ consensus price target: $2.60 (Stock Doctor, Thomson Reuters, 11 analysts), $2.52 (FN Arena, five analysts)

“Plus-sized” clothing retailer City Chic (CCX) was considered a poor result for full-year FY22, despite revenue growing by 39%, to $369.2 million, and net profit improving from $21.6 million to $22.3 million. The inventory balance nearly tripled from $67 million to $196 million – apparently to mitigate the impact of supply chain issues in FY23 – and this flowed into a shock to operating cash flow, which reversed from $15.2 million in FY21 to minus $51.9 million in FY22.

While the market appears to be worried that City Chic has been very aggressive in lifting inventory levels – and this could result in future impairments if the company can’t sell the inventory as it expects – the company justified the decision by pointing to the risk of supply chain issues continuing in FY 2023, making inventory procurement difficult. City Chic expects inventory levels to “normalise” in FY23.

The company says it is positioning itself to be a major player in the global “plus-size” market, which it says is worth US$180 billion ($265 billion). It says City Chic is the “only truly global plus-size-only business” – as at the FY22 result, 56.2% of revenue now comes from the Northern Hemisphere.

CCX shares have been hammered after the result – but this is a stock where you could buy the dip. CCX looks to be really good value at these levels.

City Chic Collective (CCX)

Source: nabtrade

Inghams (ING, $2.49)

Market capitalisation: $925 million

12-month total return: –36.7%

3-year total return: –3.9% a year

Expected FY23 dividend yield: 4.1%, fully franked (grossed-up, 5.9%)

Analysts’ consensus price target: $2.90 (Stock Doctor, Thomson Reuters, 9 analysts), $2.82 (FNArena, four analysts)

Inghams (ING), Australia’s biggest provider of poultry food products – and also a stockfeed producer – also disappointed the market with its FY22 result. Despite core poultry sales volume increasing by 4.2%, EBITDA fell 16.6% to $370.4 million, and net profit slumped 57.9%, to $35.1 million. The profit fall flowed into the final dividend, which was slashed by 94% to 0.5 cents a share, bringing the full-year dividend to 7 cents a share, down 58%.

Inghams said that global events and supply-chain disruptions are expected to continue to place upward pressure on the price of key inputs. Feed prices are expected to remain elevated due to tight global supply as a result of continued uncertainty surrounding production in Ukraine and related trade flows, poor growing conditions in North and South America and elevated transport costs.

Inghams said feed costs were “substantially” higher, and wheat and soybean meal prices were at their highest levels in ten years, partly due to the war in Ukraine. Analysts don’t appear to like the fact that the company will have to lift prices to cover its rising costs – which are not limited to feed, but also fuel and other supply-chain costs. Although no FY23 guidance was given, Inghams did say that it expects its profit margin to improve in the current year.

The company is probably on the road to recovery, but headwinds will continue into FY23, and most analysts downgraded their earnings forecasts. Analysts do see a bit of value in Inghams, and it is offering a solid projected fully franked dividend yield, but it is not as compelling a buy as CCX.

Inghams Group Limited (ING)

Source: nabtrade

CSL (CSL, $298.64)

Market capitalisation: $143.8 billion

12-month total return: –1.1%

3-year total return: 9% a year

Expected FY23 dividend yield: 1.2%, 5.4% franked (grossed-up, 1.2%)

Analysts’ consensus price target: $325.09 (Stock Doctor, Thomson Reuters, 17 analysts), $324.80 (FNArena, six analysts)

Australia’s biotech star CSL rarely disappoints, but it did in the recent reporting season, reporting a 6% drop in net profit, to US$2.2 billion, on a constant-currency basis, as sales of its core plasma therapies suffered from the continued subdued collection of plasma, the key ingredient of its treatments, on the back of COVID-19.

Total revenue was up 3% on a constant-currency basis, to US$10.7 billion, and CSL maintained its full-year dividend of US$2.22 a share.

For FY23, CSL gave guidance for net profit to increase between 7.6% and 11.8% on a constant-currency basis.

In the CSL Behring business, immunoglobulin and albumin sales were limited by COVID-constrained plasma collections in FY21, but CSL Behring managed to lift sales by 2%, to US$8.6 billion. The Seqirus business saw revenue rise by 13%, to US$1.96 billion.

All up, it was not a result that looked to be a disappointment – but it was a bit weaker than many analysts expected, especially from CSL Behring – although it came in toward the top end of management guidance. Also, CSL didn’t provide an outlook on expected plasma collections over the next 12 months, or on when the market can expect margins to return to pre-pandemic levels – and that also was seen as a disappointment. As the world’s largest collector of plasma and the second largest producer of vaccines – not to mention being the pride of the ASX – CSL is held to a very high standard by the local market!

So, while the Melbourne-based business was a bit on the soft side in terms of its annual result, it is still a tremendous global business – it’s just that it isn’t exactly cheap at the current price. The most optimistic analyst, at Citi, has a target price of $340 – I think go with that, and add some CSL to the portfolio if you don’t already have it.

CSL Limited (CSL)

Source: nabtrade

All prices and analysis at 12 September 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.