Five stocks under 50 cents to consider for your portfolio

It’s time again for “five under 50” – five stocks under (or near) the 50-cent level. At this level, there is not always profitability to go on – but there are always interesting stories, and here are five of them.

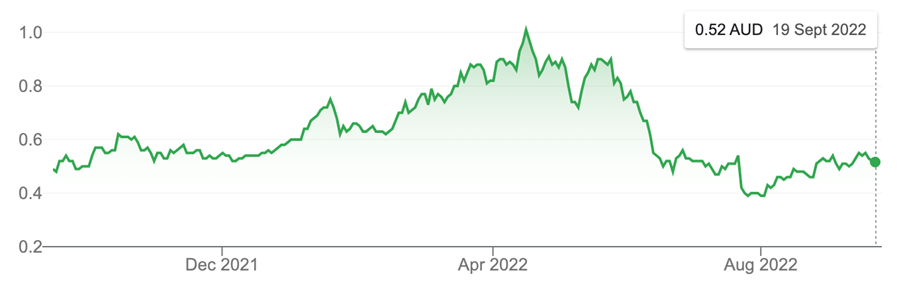

Jervois Global (JRV, 52 cents)

Market capitalisation: $209 million

12-month total return: 51.1%

3-year total return: 25.4% a year

Estimated FY23 dividend yield: n/a

Analysts’ consensus price target: n/a

OK, battery metals company Jervois Global (JRV) is not under 50 cents – but if you can buy it under that level, do so. In fact, buy it anyway. The company is nicely exposed to the booming demand for cobalt and nickel materials to serve both the battery and chemicals markets, and to provide a secure, reliable supply to customers in the face of geopolitical and other risks.

Jervois is building a fully-integrated cobalt value chain and is on track to become the only cobalt miner in the United States. In 2021, it bought the Freeport Cobalt business for a final purchase price of US$185 million, to create Jervois Finland; at a stroke, this made Jervois one of the largest western world suppliers of refined and advanced manufactured cobalt products (specialty cobalt powders and chemicals). The business has long-standing customer relationships across Europe, the United States and Japan.

In the same year, Jervois Global bought the São Miguel Paulista (SMP) nickel and cobalt refinery in Brazil, which JRV is restarting in stages over this year and next. These assets complemented the Idaho Cobalt Operations (ICO), which Jervois Global bought in 2019. Located in the eponymous US state, ICO is a high-grade ICO deposit that was partially complete when JRV acquired it. ICO also has gold and copper reserves, with the gold to be a by-product of the cobalt concentrate to be produced at ICO.

The ICO project is scheduled for commissioning this month, with the first ore going through the mill in October and full-rate processing expected by February next year. The official opening ceremony is scheduled for October 7. ICO will be the only domestic US mine supply of cobalt.

When everything is up and running, JRV will potentially be on track to become the second-largest producer of refined cobalt outside China. The SMP operation will be dedicated to cobalt concentrates from ICO. The first cobalt production at SMP from ICO concentrates is expected during the second quarter of 2023.

In June, Jervois Global updated the market that the costs to bring ICO into production will be about 7.5% higher than expected, at about US$107.5 million (A$155.7 million). It said the increased costs come from poor weather conditions, contractor shortages and the overall inflationary environment in the US.

Overall, Jervois’ strategy is to become a leading nickel and cobalt company and become the second-largest producer of refined cobalt outside China. The company is also developing Nico Young, a nickel-cobalt deposit in New South Wales, but the focus is on developing a fully-integrated cobalt value chain. Superannuation megafund AustralianSuper is on board as an investor.

JRV is a very promising situation, given that demand for cobalt will only increase with the rising use of electric vehicles (EVs) and renewable energy, the drive to Net Zero; and the fact that the world needs sources outside China and Africa. More than 70% of the global production of cobalt takes place in the Democratic Republic of the Congo (DRC) and according to UNICEF, about 20% of that cobalt comes from “artisanal” mines – meaning unofficial and often illegal mining, by hand – where about 40,000 children work in extremely dangerous conditions. Cobalt users urgently require more sustainable and ethical sources.

Jervois Global Limited (JRV)

Source: nabtrade

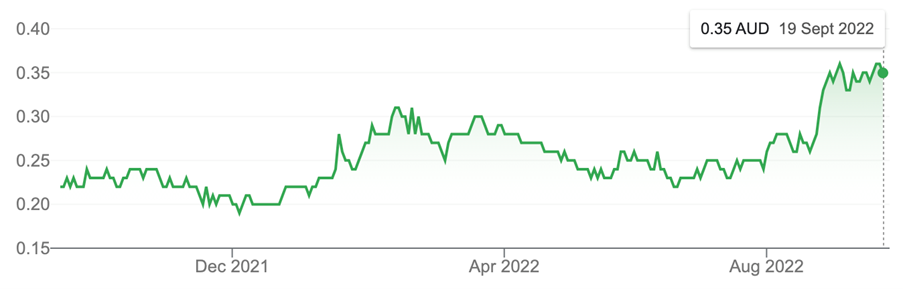

Austin Engineering (ANG, 36 cents)

Market capitalisation: $209 million

12-month total return: 51.1%

3-year total return: 25.4% a year

Estimated FY23 dividend yield: n/a

Analysts’ consensus price target: n/a

Perth-based Austin Engineering (ANG) is a major supplier to the world mining industry, producing customised “wear products” such as truck bodies and trays, digging “buckets,” water tanks, tyre handlers and ore chutes (which it makes under licence.) It has operations in Australia, Asia, North America and South America, and has a customer footprint that currently covers about 65% of the global truck tray market.

Last month, Austin bought Queensland-based mining equipment manufacturer, Mainetec, for an initial amount of $19.6 million, funded through cash reserves and debt. Mainetec designs and builds customised dipper buckets, and supplies the majority of dipper bucket systems in Australia; it also manufactures rope shovels and offers bucket repairs and spare parts. The acquisition will give Austin access to Mainetec’s Hulk range of high-performance mining buckets, which will increase the potential customer base in all of Austin’s markets. Austin will offer Mainetec’s high-value dipper buckets in its global markets, particularly North and South America, where there is high demand and a large dipper bucket market.

Austin expects Mainetec to have revenue of more than $40 million (on an annualised basis) for the 2022-23 financial year, with the acquisition expected to deliver significant synergies through the lower supply-chain costs Austin is able to provide, and optimised operating costs.

For FY22, Austin beat profit guidance for FY22, with net profit coming in at $20.6 million, above guidance of more than $18 million, and up more than five-fold on FY21. Total revenue rose 2.6%, to $203.3 million, while earnings before interest, tax, depreciation and amortisation (EBITDA), at $32.5 million, met recently upgraded forecasts, and was an increase of 155%.

Austin has operations in the US, Chile and Indonesia and says it’s been able to avoid pressures from rising steel costs. The company is well-diversified geographically, and by customer and commodity: at present, 74% of revenue comes from hard-rock mining, with 31% of revenue coming from iron ore, 30% from copper, 18% from metallurgical (steel-making) coal, 6% from gold, 5% from thermal (electricity) coal, 5% from oil and 5% from other commodities. The company says it “continues to see solid demand” despite economic headwinds: because most mines in the world transport ore from pit to process by truck, this drives (and underpins) demand for bodies and buckets.

Mainetec will provide a boost to ANG’s numbers. Excluding the Mainetec contribution, Austin has given guidance that full-year FY23 net profit is expected to be up 17% to about $24 million. The company’s order book stood at $135 million on 1 July 2022 – a $50 million rise from the same time in 2021, which ANG says indicates the potential for significant revenue growth.

Austin Engineering Limited (ANG)

Source: nabtrade

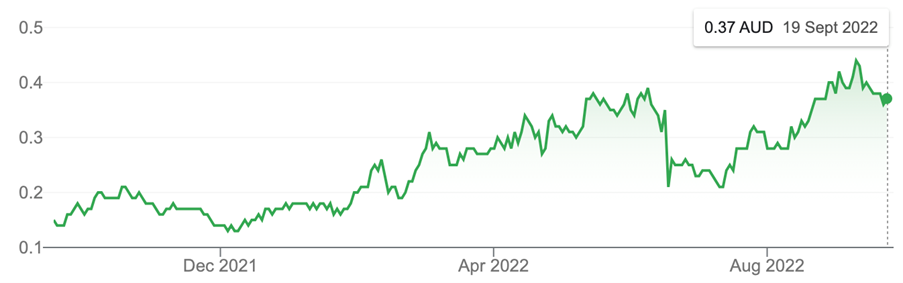

Orthocell (OCC, 40 cents)

Market capitalisation: $33 million

12-month total return: –17.5%

3-year total return: 0.9% a year

Estimated FY23 dividend yield: no dividend expected

Analysts’ consensus price target: n/a

Regenerative medicine company Orthocell (OCC) develops products for the repair of a variety of bone and soft tissue injuries, to regenerate mobility for patients. Orthocell’s platform technology has given rise to a portfolio of products that includes:

- CelGro, a collagen medical device that facilitates suture-less tissue repair and healing in a variety of dental and orthopaedic reconstructive applications;

- OrthoATI, the first injectable clinical-stage cellular therapy for the treatment of chronic tendon injuries, aimed at addressing a significant unmet clinical need for a safe, effective and non-surgical solution. The treatment is autologous, meaning uses each patient’s own tendon-derived cells to stimulate tendon regeneration and is delivered via a non-surgical ultrasound-guided injection. OrthoATI addresses a significant unmet clinical need in the healing of tendons that resist existing therapies. Orthocell is currently conducting two clinical trials with OrthoATI, the first is focused on the rotator cuff and the second on “tennis elbow” tendon defects.

- Striate, an application of CelGro approved for dental guided bone regeneration (GBR) applications, which is cleared for use in the US through the US Food & Drug Administration (FDA), 510(k) approval (for medical devices), Australia (Australian Register of Therapeutic Goods, ARTG) and Europe (CE Mark);

- Remplir, another application of CelGro, which is a collagen nerve wrap used in the repair of peripheral nerve injuries; it provides compression-free protection to the nerve, generating an ideal micro-environment to help nerve healing. Remplir helps in re-joining severed or severely damaged peripheral nerves, to restore function and sensation. Remplir recently received approval in Australia (ARTG) for surgical use.

- SmartGraft, for tendon repair, is available in Australia under Special Access Scheme or participation in a clinical trial.

The company’s other major products are autologous (using a patient’s own cells) cell therapies that aim to regenerate damaged tendons and cartilage tissue. Orthocell says its portfolio of musculoskeletal regenerative medicine applications has a total addressable annual market of US$17 billion, driven by the rising rate of musculoskeletal disorders and demand for efficient and cost-effective treatments.

In June, Orthocell signed a global exclusive licence and manufacturing agreement for Striate with BioHorizons Implant Systems, a part of the Nasdaq-listed Henry Schein, Inc., which has already seen OCC receive $21.5 million, net of fees. BioHorizons will exclusively market and distribute the Striate devices globally; Orthocell will manufacture them at its Perth facility, after increasing its capacity tenfold.

But the deal was transformative beyond the financial considerations, validating the company’s wider intellectual property suite of collagen-based regenerative devices. Orthocell says the BioHorizons deal proves the platform’s potential and positions the company to commercialise its Remplir nerve repair product in the US – the BioHorizons deal is restricted to the dental field only and does not prohibit a nerve or tendon deal.

OCC has a portfolio of world-leading regenerative medicine products. It’s early days for revenue, and the company makes a loss, but this is a story that many investors experienced in the long lead times of biotech like a lot.

Orthocell Limited (OCC)

Source: nabtrade

AIC Mines (A1M, 50.5 cents)

Market capitalisation: $158 million

12-month total return: 106.1%

3-year total return: 8.8% a year

Estimated FY23 dividend yield: no dividend expected

Analysts’ consensus price target: 65 cents (Stock Doctor/Thomson Reuters, three analysts), 70 cents (FNArena, one analyst)

The former Intrepid Minerals bought the Eloise mine in North Queensland from FMR Investments for $27 million in November last year and became a producer. In its first eight months under AIC Mines’ ownership, the mine generated $50.2 million in operating mine cashflow and $16.9 million in net mine cashflow at a low all-in sustaining cost (AISC) of $4.33 a pound of copper sold. (AISC is a figure that incorporates not only the “cash cost” of production but all the costs that allow production to be sustained.) At Eloise, the company produces a high-quality copper-gold-silver concentrate.

Located south-east of Cloncurry in North Queensland, Eloise is a high-grade underground mine with a 26-year operating history; at a reserve grade of 2.3% copper and 0.6 grams per tonne (g/t) of gold, it is one of the highest-grade copper mines currently operating in Australia. The resource contains 115,000 tonnes of copper and 100,100 ounces of gold; the reserve contains 36,000 tonnes of copper and 32,600 ounces of gold; and the current “life of mine” (LOM) plan extends to June 2030. In FY23, AIC Mines (A1M) is targeting production from Eloise of approximately 12,500 tonnes of copper and 6,000 ounces of gold in concentrate, at an AISC of approximately $4.50 a pound of copper.

AIC Mines is conducting exploration to lengthen the LOM at Eloise, but is also pursuing a takeover bid for Demetallica Limited (DRM), which listed on the ASX in May, the primary focus of which is the Jericho copper-gold resource, discovered in the Jericho prospect in 2017, adjacent to the Eloise mine. A1M’s pitch to Demetallica shareholders is that Combining Eloise and Jericho provides the quickest and most efficient means of developing, mining and processing Jericho.

Together, says AIC Mines, Eloise and Jericho would have combined resources of 245,000 tonnes of copper and 188,100 ounces of gold, increasing the mine life past ten years. Production through the Eloise plant could be increased by about 60%, to more than 20,000 tonnes of copper and 10,000 ounces of gold in concentrate. Also, the potential economies of scale would reduce the operation’s AISC.

A1M has other prospects – including its Marymia gold and copper project in Western Australia, at which it just kicked off a drilling program – but Eloise is the flagship. Even if the Demetallica bid does not succeed, Eloise has the capacity to produce at least 45,000 tonnes of copper and gold concentrate a year. It’s a great emerging copper story.

AIC Mines Limited (A1M)

Source: nabtrade

Bowen Coking Coal (BCB, 36 cents)

Market capitalisation: $557 million

12-month total return: 125%

3-year total return: 64.4% a year

Estimated FY23 dividend yield: no dividend expected

Analysts’ consensus price target: 53 cents (Stock Doctor/Thomson Reuters, two analysts), 55 cents (FN Arena, one analyst)

I accept that coal is not going to be everyone’s cup of tea, but Bowen Coking Coal (BCB) is a stand-out emerging story – and in the “good coal,” metallurgical (steel-making, or coking coal), which is essential in the production of steel.

In July, BCB became Queensland’s (and Australia’s) newest independent metallurgical coal producer, shipping its first delivery of approximately 35,000 tonnes of ultra-low volatile pulverised coal injection (ULVPCI) to a customer in Taiwan, from its Bluff Mine near Blackwater, which the company bought in December 2021, and where first coal was mined in April.

Last month, a second cargo of 40,000 tonnes of ULVPCI coal from Bluff was shipped from Gladstone, and BCB processed the first coal from its Broadmeadow East mine near Moranbah, which BCB bought from Peabody Energy in 2020, and began mining in July.

As the first producing pit of BCB’s expanded Burton Complex, which includes the Burton and Lenton pits, 20km to the north, Broadmeadow East coal will be processed through the Burton coal handling and preparation plant (CHPP) when its refurbishment is completed in early 2023. First coal from the Burton pit is targeted for late in the fourth quarter of 2022.

At Bluff, production is now expected to ramp up to a steady state ROM target of up to 100,000 tonnes a month, representing an annualized production rate of between 1 million–1.2 million tonnes a year, over four to six years, to supply the global steel industry.

The next of BCB’s projects to be developed is Isaac River, located 30 kilometres east of Moranbah in the central Bowen Basin, which contains a resource estimate of 8.7 million tonnes, and where BCB says studies have indicated a ROM production target of 400,000 to 600,000 tonnes a year over a four to five-year period.

By 2024, BCB is targeting production of more than 5 million tonnes a year. And – like it or not – the company has the market into which to sell, on the back of under-investment in metallurgical coal capacity and growing steel demand worldwide. The company has the option to add thermal (electricity) coal into its product mix if desired, but at this stage, it is a steelmaking-coal story – and a very compelling one.

Bowen Coking Coal Limited (BCB)

Source: nabtrade

All prices and analysis at 19 September 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.