Three Property Trusts that can withstand rising inflation

I read an interesting piece recently on the Work From Holiday (WFH) trend.

Yes, it’s not enough to work from home during the pandemic. Some want to work anywhere, anytime … even if it’s at a holiday resort.

Some fancy overseas hotel chains now rent rooms from 10am to 6pm, hoping to attract work teams that want an occasional change of scenery – or individual travellers. The hotels see an opportunity to compete with co-working centres.

A fund manager I know is bullish on Airbnb shares because of this Work From Holiday trend. He believes the line between work and holidays is blurring. More people will rent longer holiday stays as they mix work and leisure (without taking annual leave).

I don’t know how much data supports this trend. It could be one of those catchy, anecdotal stories. What I do know is that more workers are resisting going back to the office for the full week. They want the flexibility of working when and where they want.

With some unions pushing for work-from-home to be included in awards, it’s clear that the pandemic will permanently change how we work, to some degree.

That’s bad for Australian Real Estate Investment Trusts (A-REITs) that own office towers and face long-term structural challenges as more people work from home and spend less time in CBDs.

A-REITs that own prime shopping malls should benefit from this trend in the long term. I’ve long argued that fortress malls are becoming mini-CBDs and enterprise centres. As extra people work from home in the suburbs, these malls will have a new purpose. I’m surprised more fortress malls aren’t building co-working centres for small business.

That said, the short-term outlook for retail A-REITs is tough. Readers of this column know I am bearish on the economy and share market. We have a tough year ahead. The focus now should be on capital preservation and defensive income.

Retail A-REITs will keep underperforming if the Reserve Bank persists with its insane rate rises. Our central bank is raising rates too far, too fast. If this continues, hundreds of thousands of Australians won’t be able to pay their mortgage this time next year.

Perhaps low unemployment will save our housing market. The key to keeping your house is keeping your job. Perhaps the huge savings built up during COVID-19 will provide some relief as rates rise, but home-loan data does not show that. About a third of home borrowers have no buffer (from getting ahead on their repayments).

I hope I’m wrong, but the odds of a recession in Australia next year are shortening by the day. That’s bad news for owners of retail property who will face waning demand for space or have to provide larger incentives to attract and keep tenants.

Industrial property has much better prospects. It wins from growth in e-commerce and the need for fulfilment centres, warehouses and other logistic centres. But key industrial property owners, such as Goodman Group (GMG) , are fully priced.

Property bulls will argue that A-REIT valuations reflect the problem for office and retail property. The S&P/ASX 200 A-REIT index has a year-to-date total return (including distributions) of minus 19.3%. By comparison, the S&P/ASX 200 is down 8.8%.

Surely, such horrible underperformance is a buy signal? A-REITs have underperformed the market for the past five years. Some look cheap, on paper.

My concern is the uncertainty of rate rises. For over a year, I have argued in this column that higher inflation was not “transitory” or just a short-term response to supply-chain bottlenecks during COVID-19. I wrote that the biggest investment risk this decade would be loss of purchasing power as inflation rose.

Central banks have belatedly changed their tune on inflation. Big-four bank economists are lifting their projections for peak interest rates in this cycle. The risks to rates are on the upside. In that environment, it’s hard to find a near-term catalyst to re-rate the A-REIT sector.

Of course, there are exceptions in every sector. If you want to buy A-REITs now, focus on those with defensive property assets and tenants who can better withstand rising inflation. Or A-REITs that have a sufficiently attractive valuation.

Here are three A-REITs that fit that bill.

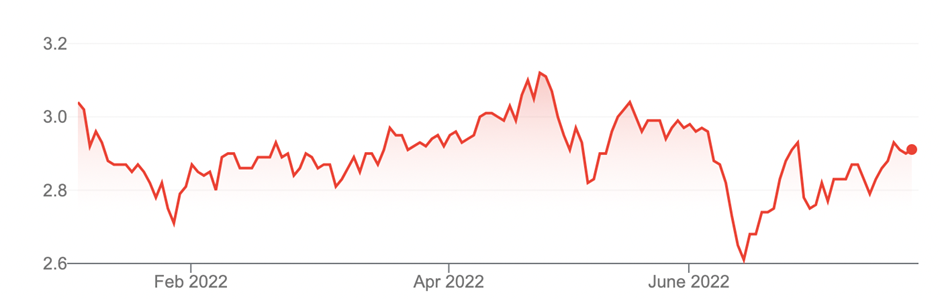

1. Shopping Centres Australasia Property Group (SCP)

SCP owns a portfolio of neighbourhood and sub-regional shopping centres. Often, the centre includes an anchor supermarket, liquor store, chemist and a handful of other speciality outlets. The centre is about mundane grocery shopping, not a retail “experience”.

Although it’s a retail A-REIT, SCP is more defensive. Woolworths and Coles pay more than 40% of its gross rent. By category, food, liquor and health account for over half the revenue from its tenants. These items are less discretionary.

In the short term, SCP could benefit from rising inflation and interest rates as people eat out less, and cook at home more, to save money. Longer term, population growth is good for owners of sub-regional shopping centres.

SCP is up 8% since June, but at $2.91,still looks reasonable value for long-term investors.

Chart 1: Shopping Centres Australasia Property Group (SCP)

Source: ASX

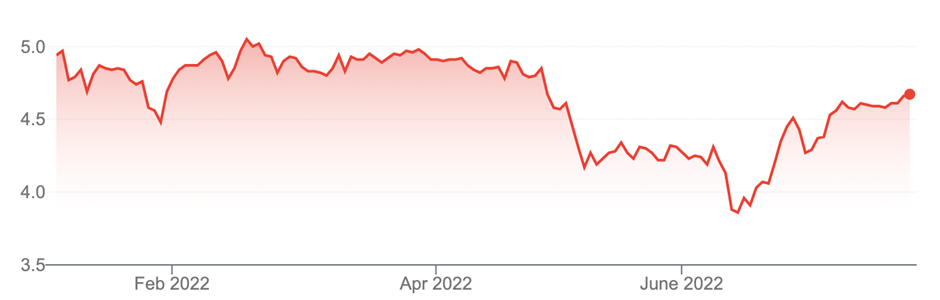

2. ARENA REIT (ARF)

For many years, ARENA has been among my favourite small-cap stocks. The A-REIT’s five-year annualised annual total return is 24%.

I like ARENA’s strategy to own childcare and healthcare properties, two defensive sectors. I prefer owners of childcare property rather than childcare operators, such as G8 Education, which can be volatile and hard to invest in.

With unemployment below 4%, ARENA will benefit as more people return to work (and demand for childcare property increases). Population growth and the long-term trend of higher female participation in the workforce bode well for ARENA.

ARENA is up from $4.30 to $4.72 since early July. It trades at a hefty premium to its Net Tangible Assets (NTA) because the market recognises the quality of its assets and performance.

Gains will be slower from here, but ARENA remains a solid long-term bet.

Chart 2: ARENA REIT (ARF)

Source: ASX

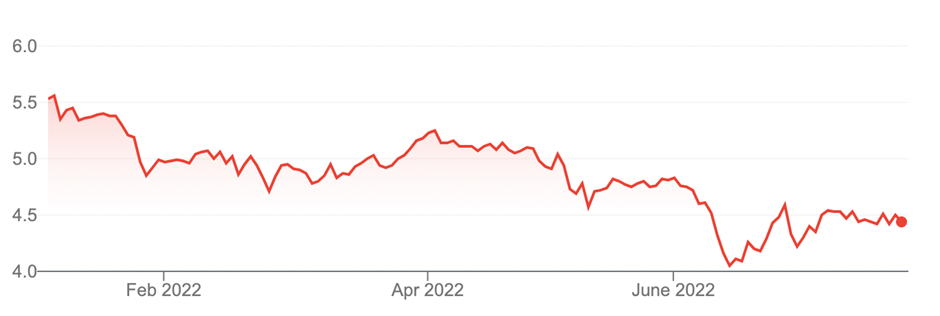

3. GPT Group (GPT)

My preference in A-REITs, for now, remains niche property trusts targeting defensive sectors. GPT Group, a large-cap diversified REIT, is the exception on valuation grounds.

GPT is this market’s oldest A-REIT and owns prime retail, office and logistics assets. About a third of its revenue comes from retail and a quarter from office assets. GPT also has a small funds-management operation.

GPT has fallen from a 52-week high of $5.59 to $4.50, in line with broader weakness in the A-REIT sector. Its current price is a 26% discount to GPT’s NTA ($6.09 at 31 December 2021). The size of that discount looks excessive.

The market appears to be pricing in a significant correction – or even a crash – in commercial and retail property values. Asset values will fall as rates rise, but the market’s view on GPT is too bearish at the current price.

At $4.50, GPT is expected to yield above 6.6% in FY23. It’s on a forecast Price Earnings (PE) multiple of 12 times FY23 earnings, on Morningstar numbers. Moreover, GPT has underperformed the market for the past few years.

Long-term investors should put GPT on their radar. Further price weakness would not surprise given sentiment towards the sector as rates rise – and amid fears that some AREITs might have to raise equity capital at depressed prices if falling property values trigger covenants in their debt agreements.

GPT has high-quality assets and its diversification appeals in this market. At the current price, GPT suits income investors who can ride out any short-term price volatility.

Chart 3: GPT Group (GPT)

Source: ASX

Tony Featherstone is an expert contributor to the Switzer Report. He is a former managing editor of BRW, Shares and Personal Investor magazines. All prices and analysis at 26 July 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.