Two essential investments for tough times

A veteran stockbroker once chided me for “being too bearish at the bottom”. This was the time to encourage investors to buy, not frighten them away, he exhorted.

In theory, the broker was right. Having the courage to buy companies trading at bottom-quartile valuations – and the nerve to hold them – is the essence of great investing.

In practice, the broker was wrong. The market kept falling, then spent years grinding sideways and frustrating investors. It took ages for the market to bottom out.

The broker forgot the two great rules of share market investing. One, preserve capital. Two, never forget rule one. An ability to minimise losses in bear markets – and keep capital intact to fight another day – distinguishes great investors from the rest.

Right now, I can highlight dozens of quality companies that are at least 20% off their 52-week high and stand out at the current price. What I can’t do is identify a near-term catalyst to re-rate those stocks. The risks are slanted to the downside.

Banks look more interesting after price falls this year. As I have written before in this Report, banks are one of my preferred sectors as inflation rises. ANZ’s $4.9 billion takeover bid this week for Suncorp Bank shows that ANZ, too, sees value.

When rates rise, banks initially benefit from an expanding net interest margin (the difference between interest received and paid). But I’m concerned that the Reserve Bank is lifting rates too far, too fast and risking a sharp downturn in house prices. Rapid rate rises will also stymie lending growth, which is bad for banks.

The big commodity producers are my other preferred sector in an inflationary environment. I like the long-term outlook for commodity producers due to supply constraints. However, as the risks of a global recession rise, so does the risk of short-term demand destruction for commodities. China’s economic slowdown is worrisome.

So, what should investors do?

The starting point is having realistic expectations. Make no mistake: the worst is yet to come. More rate rises are a certainty as inflation remains stubbornly high, perhaps higher than the market expects, judging by the latest US inflation figures.

If consumers are hurting now, wait until the official cash rate heads above 2% (from 1.35% now) and a US recession and slowing Chinese growth trigger a global recession. Or when house prices fall by double-digit rates, making consumers feel less wealthy.

Some investors forget how far markets can fall or how long they can stay down. The current predicament could take years to work through, if history is a guide.

Not for a minute do I expect a quick market recovery (a V-shaped pattern). Yes, there will be periods when it feels like storm clouds are clearing: better-than-expected US earnings results this week is an example.

But I still think we’re at the end of phase one of this bear market: falling valuations due to rising interest rates. Phase two – a wave of earnings downgrades – is yet to happen, although we will know more about the outlook when companies report in August.

Phase three is emergency capital raisings from speculative companies – and investor capitulation, which is still a way off.

As I have written previously, the focus now should be on capital preservation and defensive yield. In recent months, I’ve highlighted several sectors and stocks that suit volatile markets: global healthcare and consumer staples, for example.

Investors who want to buy should favour companies that provide the essentials and have some pricing power, meaning they can lift prices as their costs rise. Ask yourself: what are the essentials people can’t do without in tough times?

Food and petrol (to an extent) are obvious choices. As readers know, I like fast-food stocks and some alcohol retailers that benefit as people trade down to cheaper food and liquor. Essential healthcare products and services are another example.

Here are two other sectors consumers can’t live without:

1. Insurance

Hands up if you pay premiums each month for your house and its contents, cars and health. Perhaps you have income, trauma and life insurance, or a policy for your pets. Keep your hand up if you intend to drop any insurance as household budgets groan.

Some forms of insurance are about as defensive as it gets. Yes, I might look for a better deal when the economy slows and I need to cut costs. But dropping house, contents or car insurance – or my family’s health cover – is not a consideration.

Insurance Australia Group (IAG) is my preference among large-cap insurers. In mid- and small-caps, I favour NIB Holdings (NHF) and AUB Group respectively.

Like other general insurers, IAG will benefit from rising investment income as interest rates rise (insurers invest a lot of their capital in fixed interest). As house costs and used-car prices rise, IAG could also benefit from higher policies and premiums.

The downside is the increase in natural disasters, such as flooding in New South Wales, although insurers manage this through their reinsurance programs (which come at a cost). At $4.34 a share, the market has priced this short-term earnings risk into IAG.

Rising rates should provide a decent tailwind to IAG’s FY23 earnings over the next few years. A few extra percentage points of return on IAG’s investment pool will make a big difference to its earnings over the next few years.

On Morningstar’s number, IAG has a forecast Price Earnings (PE) multiple of 14 times in FY23 and a yield of 5.3% (or 6.9% after franking).

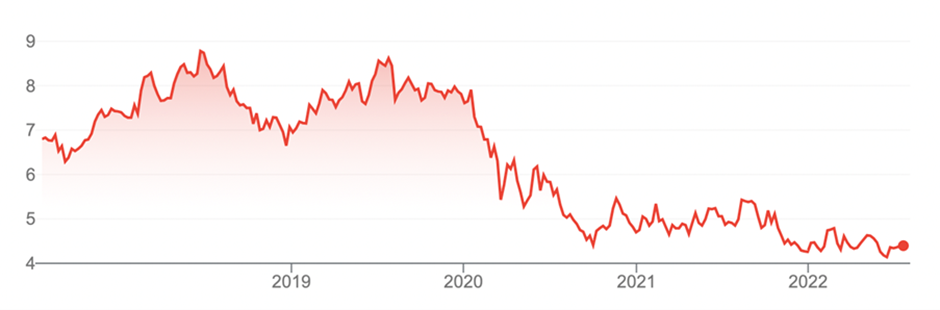

IAG has underperformed the market over the past five years. From $8.62 in mid-2019, the insurer has almost halved, bouncing along the bottom for the past two years.

But every stock has its price. This year, IAG has faced inflationary pressures (which have lifted the value of some insured assets such as used cars), a short-term hit from falls in investment markets, and natural disasters.

As rates rise and insurance premiums increase, IAG could finally get a break in the weather. At $4.34, the market can only see gloom for IAG.

Chart 1: Insurance Australia Group (IAG)

Source: ASX

2. Infrastructure

A recurring theme in this market is to buy companies that provide essential products or services and have some pricing power. Regulated core infrastructure assets – think gas, electricity and water utilities – are highly defensive and have inflation-linked revenues.

Lately, I’ve done much research on infrastructure stocks. The more I look at that sector, the more I believe it should be a permanent allocation in portfolios, possibly 5-10% of asset allocation, depending on the investor’s timeframe and goals.

Superannuation and pension funds can’t get enough of infrastructure – mostly the unlisted kind. Some big funds allocate well north of 10% of their fund to this alternative asset class. The result is most Australians already have significant exposure to infrastructure through their superannuation.

Those who want infrastructure exposure in their non-super portfolio should consider global infrastructure managed funds. ASX offers limited choice in infrastructure stocks after a spate of takeovers. The best listed infrastructure opportunities are overseas.

Argo Global Listed Infrastructure (ALI) is an interesting tool for infrastructure exposure. The Listed Investment Company (LIC) uses Cohen & Steers, a prominent US-based alternative-assets manager, to run the infrastructure portfolio. The fund is mostly invested in high-quality listed infrastructure assets overseas.

ALI’s underlying fund has outperformed its benchmark over one, three and five years to end-May 2021. Since listing, ALI has provided solid rather than spectacular returns, as one should expect from a diversified global infrastructure fund.

As a LIC, ALI is well placed to pay consistent dividends and use its company structure to generate franking credits for Australian retail investors. The company structure of global LICs – and what that means for dividends and franking credits – is often underappreciated in this market.

Investors who want defensive yield in a volatile market could do worse than favour listed infrastructure assets with regulated assets. Or use an LIC from one of this market’s most respected LIC managers and benefit from that structure’s dividend advantages.

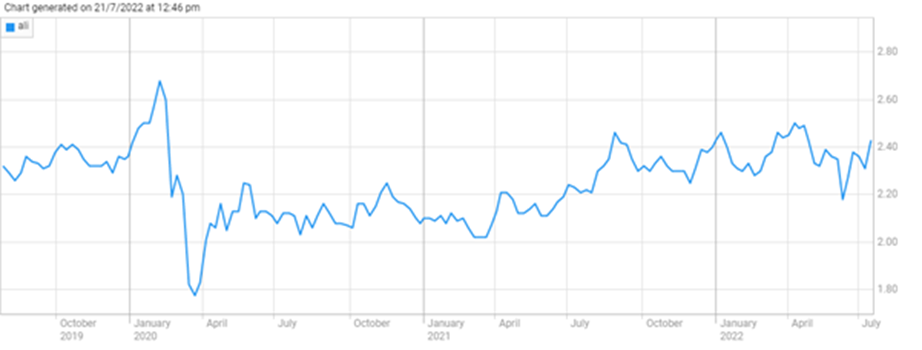

At $2.39, Argo is trading at a slight discount to its latest Net Tangible Assets ($2.45).

Chart 2: Argo Global Listed Infrastructure Ltd (ALI)

Source: ASX

Tony Featherstone is a former managing editor of BRW, Shares and Personal Investor magazines. All prices and analysis at 21 July 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.