Super changes for the new year

Welcome to a new financial year! As always, that means further changes to the superannuation system. Here are five important changes that came into effect on 1 July.

1. Employers will now contribute 10.5% to super

The rate of employer contributions to super (the so called ‘super guarantee levy’) is increasing from 10.0% to 10.5%. If you earn $100,000, your employer will now contribute $10,500 rather than $10,000 to your super fund.

Super is payable on salary and wages, including bonuses, but not overtime. Technically, it is not payable on amounts in excess of a salary of $240,880 ($60,220 per quarter) although many employers choose to pay it.

There is no change to the concessional contributions cap of $27,500. Concessional contributions are the employer’s 10.5% plus any amount you choose to salary sacrifice plus any amount you contribute and claim a tax deduction for. If you are at risk of going over the cap of $27,500, talk to your employer – there is no upside in being over the cap.

Another change that will impact some employers and casual staff is the abolition of the rule that exempted employers from paying super if the employee’s gross wage was less than $450 in any month. All casual staff are now entitled to super.

2. 67 to 74 year olds can make big ‘one off’ contributions to super

A big change to the super rules this year is the abolition of the ‘work test’ for those aged 67 to 74 years. Anyone in this age bracket can now access the concessional contributions cap of $27,500 and the non-concessional contributions cap of $110,000.

Personal (non-concessional) contributions of up to $110,000 are allowed provided your total superannuation balance is less than $1.7m at the start of the year, irrespective of work status. Importantly, those aged 67 to 74 years can now access the ‘bring-forward’ rule, which allows them to make 3 years’ worth of non-concessional contributions in one hit. Potentially, an individual could get $330,000 into super in one hit and a couple $660,000.

There is one important caveat to accessing the ‘bring-forward’ rule, your total superannuation balance. If it is between $1.48m and $1.59m, the maximum amount you can contribute is $220,000. If it is between $1.59m and $1.7m, the maximum amount is $110,000 and if over $1.7m, no contribution is allowed.

Salary sacrifice contributions are allowed irrespective of work status. Those aged 67 to 74 years who are seeking to claim a tax deduction for a personal super contribution will still need to satisfy the ‘work test’.

3. Downsizer contribution age threshold reduces to 60

“Downsizers“ who are aged 60 or older can make a special contribution of up to $300,000 into their super, with the age threshold reducing from 65 years to 60 years. Downsizer contributions are not subject to the contribution caps, and can be make irrespective of your total superannuation balance.

To qualify, you need to have owned your home for 10 or more years prior to the sale. You need to make the contribution within 90 days of receiving the proceeds of the sale, and you can’t previously have made a downsizer contribution. Couples can potentially make a contribution of $300,000 each.

If you are in the pension phase of super, downsizer contributions will count against the transfer balance cap of $1.7m.

4. First home super saver limits are being increased

A “no brainer” savings scheme for those looking to buy their first home, the limit on how much you can access from super to help fund the purchase of a home is being increased from $30,000 to $50,000.

The amount you contribute to super to count as part of this scheme is capped at $15,000 pa. Contributions take the form of pre-tax salary sacrifice (concessional contributions) or post-tax personal contributions (non-concessional). Your employer’s 10.5% doesn’t count.

The first home super saver scheme delivers a high, secure return for aspiring homebuyers, much higher than if investing in a term deposit. For more information, visit the ATO's website.

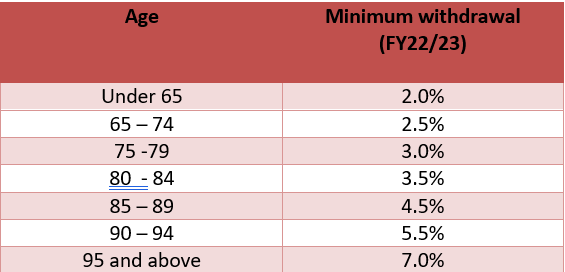

5. Reduced minimum pension payments

The Government has extended for another year a measure introduced during the Covid-19 pandemic that halves the minimum amount retirees must take as a super pension.

The minimum pension payment is age based, and calculated on the balance of your super assets in the pension phase at the start of the financial year (1 July). The factors to apply in 22/23 are shown below:

For example, if you were aged 66 on 1 July 2022 and had an account balance of $1,000,000, your minimum payment is 2.5% of $1,000,000 or $25,000. You can take your pension at any time and in any amount(s), but your aggregate drawdown over the year must exceed the minimum amount. If you commence a pension mid-year, the minimum amount is pro-rated according to the number of days remaining until the end of the financial year.

Paul Rickard is co-founder of the Switzer Report. All prices and analysis at 30 June 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.