Can Woodside's share price keep increasing, or is Santos a better bet for investors?

The energy sector is the standout performer on the Australian stock market this year – a total return of 35.7% to the end of May compared to the market’s small loss of 1.3%. It is of course mainly thanks to the Ukraine war and the recovery from Covid, and the inability (or unwillingness) of OPEC+ to materially lift production in response.

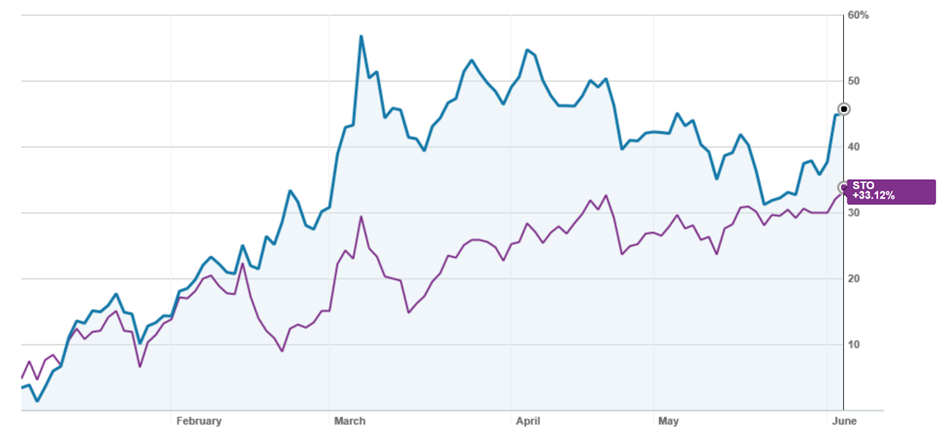

Big winners have been sector leaders Woodside Energy (WDS) and Santos (STO) – the former is up by 51.7% this year (with dividends included), while Santos has returned 35.0%.

Woodside (blue) and Santos (purple) in 2022

Source: nabtrade

Last week, a major “price capping hurdle” was lifted for Woodside when broker JP Morgan auctioned and cleared a line of 38 million Woodside shares at $29.15. These were shares that were being sold on behalf of ineligible and small shareholders who didn’t participate in the BHP/Woodside oil asset merger and distribution in kind of new Woodside shares, and removed a major overhang from the market.

That overhang hasn’t quite gone because Woodside’s ordinary shares have almost doubled with an extra 915 million new shares being issued to BHP shareholders. Some of these shareholders will decide for various reasons, including ESG concerns, that they don’t want to own Woodside shares. On the other side of the ledger, Woodside’s elevation to a ‘top 10’ independent global energy company might create new demand from international investors.

The question many investors have is “can Woodside’s share price keep going up”? In the short term, this clearly depends on the oil price, as the spot LNG price largely tracks the former. Also, Woodside has become more directly dependent on the oil price following the integration of the BHP assets – which include a 50% ownership of the Bass Straight JV with Esso and oil production in the Gulf of Mexico.

In the medium term, while the oil price will still be a major factor in the share price, the management team’s skills in project execution, production, cost management and marketing will also be critical. As will be the ability to deliver the synergy savings of US$400m that were forecast when the two businesses were put together.

I am not going to forecast the oil price and will leave that to the experts (If there are any). But I do note that the price seems to be inching higher (with very few pullbacks) and the conviction of the OPEC+ group to lift supply doesn’t appear overwhelming. The graph below suggests the upside trend is still in place.

Oil Price (WTI) in USD - 2022

Source: CNBC.com

So where to for Woodside, or is Santos a better bet? Let’s start with the experts – the broker analysts.

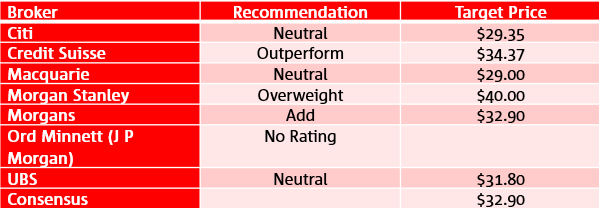

The brokers are generally positive on Woodside, but see it as close to fully valued (given their assumptions on oil and LNG prices). The table below sets out the recommendations and target prices of the major brokers. The consensus target price is $32.90.

Broker Recommendations and Target Prices – Woodside (WDS)

Source: FN Arena, 6/6/22

Morgan Stanley has the highest target price. According to the broker: “Woodside Energy’s acquisition of BHP’s petroleum division is transformational and there is potential for a multi-year re-rate. The company is considered one of the best global plays on gas. Even if the Russian/Ukraine conflict de-escalates, Europe will need to diversify its energy needs, which will keep energy prices elevated and underpin further demand growth for LNG”.

Woodside’s potential to pay out a super-sized dividend has not gone unnoticed. For the CY22 year (Woodside operates on a calendar year basis), the brokers forecast on consensus a full year dividend of A$3.30 per share (based on current AUD/USD exchange rate of 0.7200). This puts Woodside on a prospective yield of 10.4%, plus franking credits.

In CY23, the yield is forecast to fall to 8.1%.

On a multiple of earnings, the brokers have Woodside trading on the undemanding multiples of 7.2x forecast CY22 earnings and 9.4x forecast CY23 earnings.

The brokers see more upside for Santos. The consensus target price is $9.72, 15.7% higher than the last ASX price of $8.40. All bar one of the major brokers has a ‘buy’ recommendation, as detailed in the table below.

Broker Recommendations and Target Prices - Santos (STO)

Source: FN Arena, 6/6/22

Macquarie prefers Santos to Woodside in the large caps, while Credit Suisse considers Santos to “provide a strong exposure to uncontracted LNG upside vs global peers” (Much of the LNG that Santos and Woodside produce is sold on long term contracts at prices well below the current spot price).

On multiples, Santos (which also operates on a calendar year basis) is trading at 7.0x forecast CY22 earnings and 8.8x forecast CY23 earnings.

The dividend is forecast at around A$0.32 per share (about 70% franked), putting it on a prospective yield of 3.8% for CY22 and 3.6% for CY23. Santos’s recently updated its capital management framework, and is currently conducting an on-market share buyback of US$250m. To quote the MD & CEO Kevin Gallagher: “We are now in a position to target higher shareholder returns through our new capital management framework and are pleased to announce an initial on-market share buyback of up to US$250m because we believe the current share price undervalues the company”.

Bottom line

Given their very undemanding multiples, both companies have upside potential. I don’t think now is the right time to be going “short” the energy sector. The broker forecasts are inherently conservative when it comes to oil and gas prices.

With much of the “overhang” in Woodside shares lifted, I am more comfortable in holding Woodside. Certainly, dividend seekers aren’t going to be selling. But Woodside does have some major challenges – delivery of the Scarborough offshore gas project and realization of the annualised US$400m synergy benefits.

Santos, while not offering the same income return for investors, has a very disciplined strategy and the integration of the Oil Search business has resulted in diversified portfolio of long-life, low cost oil and gas assets. It is actively investing in carbon capture and storage projects, which it hopes to turn into a major revenue stream. Santos is potentially higher risk, but I am with the major brokers and see more upside potential.

All prices and analysis at 06 June 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.