What’s the one Australian tech stock that I’d recommend?

I have been a huge fan of cloud accounting software provider Xero (XRO). Technically a New Zealand company, Xero is right up there in the top tier of Australian technology companies, demonstrating consistent high growth, innovation and market leadership. In terms of the key SaaS (software as a service) metrics, it is world-class with a low cost of acquisition in terms of payback time, low churn, high LTV (lifetime value) of customers and high LTV/CAC (lifetime value to cost of acquisition) ratio. Moreover, Xero’s customers love it. It has left MYOB, Quicken and other providers of accounting software to small-and-medium businesses in its wake.

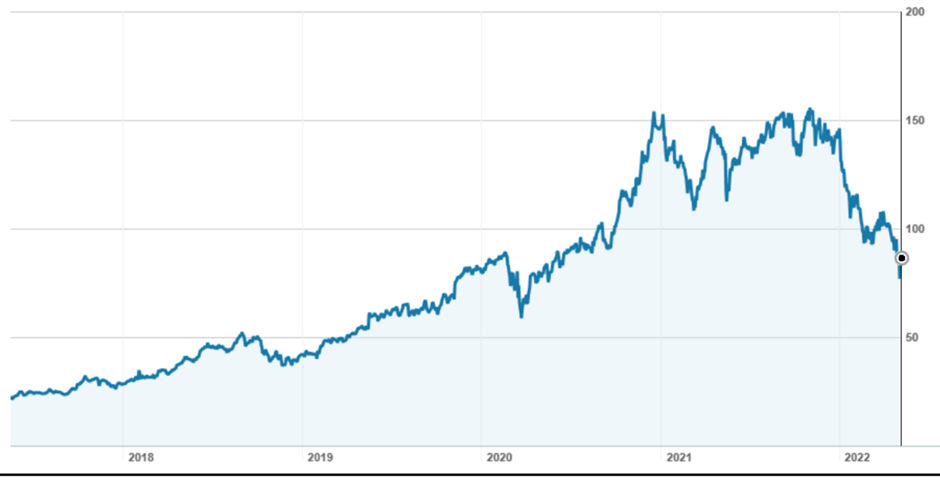

So it has been hard watching Xero get smashed this year as high growth technology stocks have been sold off. Starting the year at $141.44, it fell to a low of $75.80 last Thursday following the release of its full-year profit result, before recovering to $84.16 on Friday. Year to date, it has lost 40.4%.

Against the top US tech players, it looks like a big fall – Apple is down 17.2%, Alphabet 19.9% and Microsoft 22.4%. But compared to some others, it is not out of kilter. Atlassian, for example, is down 50.5%, Metta (Facebook) 41.0%, and Block 47.9%. Locally, WiseTech Global is off 30% this year.

Xero (XRO) 5 year stock price chart to 5/22

Source: nabtrade

So can the Xero share price recover?

Let’s start by looking at the annual profit result, and then see what the brokers have to say.

Xero’s 2022 financial results

Xero grew operating revenue by 29% to NZ$1,097 million. On a constant currency basis, this was up 30%. Excluding revenue from businesses acquired during the year, the growth rate was a high 24%.

Operating expenses grew by 39% to NZ$921 million, as Xero invested for growth and integrated newly acquired businesses. This meant that EBITDA only increased by 11%, from NZ$191.2 million to NZ$212.7 million.

Free cashflow fell from NZ$56.9 million to just NZ$2.3 million, with net cash on hand decreasing by NZ$205.4 million to NZ$51.2 million as at 31 March.

Although the result was a small “beat” on both revenue and earnings, the market didn’t like the expense profile and the continued cash burn in pursuit of growth. Looking ahead, Xero said that it expected total operating expenses (including acquisition integration costs) as a percentage of operating revenue to be towards the lower end of a range of 80-85%. This will be down marginally on the 84% achieved in FY22, but up from the 78.2% in FY21.

Xero said: “it will continue to focus on growing its global small business platform and maintain a preference for re-investing cash generated, subject to investment criteria and market conditions, to drive long term shareholder value”.

The “growth” metrics were, however, impressive:

- In Australia, subscribers are up 21% to 1.34 million; in the UK, subscribers are up 18% to 850,000 and in the US, subscribers are up 19% to 340,000. Globally, subscribers increased by 530,000 to 3.27 million, a growth rate of 19%;

- Churn fell from 1.01% to 0.90% per month;

- Average revenue per user (per month) rose from NZ$29.30 to NZ$31.36; and

- LTV/CAC (lifetime value to cost of acquisition) increased from 6.4x to 6.9x. In Australasia, this ratio is 14.9x, whereas, for the international businesses, it is 3.1x (but improving).

What do the brokers say?

While positive on Xero overall, the major brokers’ ratings reflect the challenges of valuing technology stocks in the current environment. Morgan Stanley is at one extreme with a target price of $148 and an ‘overweight’ recommendation. On the other hand, despite finding the result “strong”, UBS lowered its target price from $80 to $70 and maintained its ‘sell’ rating.

On consensus, the target price (according to FNArena) is $110.50, approx. 31% above its closing price on Friday. Individual target prices and recommendations are shown in the table below.

Source: nabtrade

So, is it a buy?

If I had to name one Australian technology stock for investors to own, it would be Xero. So after a 40% fall, it has to be interesting. There is nothing in the company’s financial result last week that makes me less interested in owning it.

But as we have seen before when the market goes negative on a sector or company, it can be pretty punishing and overshoots (both on the upside and downside). If the lead out of the US on technology stocks continues to be negative, Xero won’t be able to stay out of the wash and its price will come under pressure.

That all said, my sense is that 12 months from now, Xero will look like good buying in the mid-eighties.

Paul Rickard is co-founder of the Switzer Report. All prices and analysis at 16 May 2022. This information was produced by Switzer Financial Group Pty Ltd (ABN 24 112 294 649), which is an Australian Financial Services Licensee (Licence No. 286 531This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. This article does not reflect the views of WealthHub Securities Limited.